China Weekly Wrap

a week that was 10 - 14 March 2025

Good Morning,

Welcome back to the China Weekly Wrap. A turbulent week across the world for all sorts of reason. We’re navigating the tariff headlines, the potential peace deal in Russia/Ukraine conflict, coupled with varying proposals for a grand bargain with the east and the west. At the same time we’re still processing the practical outcomes of the Two Sessions. This led to a somewhat reduced level of activity on the blog where the only real update was our piece on JD 0.00%↑ available to premium subscribers here. If you are interested in it, we encourage you to subscribe.

Be on the look out for our Portfolio Review piece tomorrow, where we will be touching on some of the ETF performances. Again, thats a paywalled feature, so if thats of interest do consider subscribing!

The Perspecticast is going on the road this coming week - we’re recording a special joint episode with an amazing recording partner - stay tuned for that, should be great fun!

After that we’ll finally complete pour China Internet overview - Meituan and Kuaishou are the only 2 pieces left to publish. Meituan will be the closer, so we’ll aim the get the Kuaishou out early and finalise Meituan for later in the week.

We also anticipate being in a position to make a big announcement on the structure of the services side of the blog this coming week, so do stay tuned for that as well, even if maybe that’s more exciting for us, behind the scenes, nevertheless It should give subscribes confidence that we’re palling on keeping going and developing the blog and the services.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

As of March 14, 2025 close of business, here’s a summary of the weekly, month-to-date (MTD), and year-to-date (YTD) performances of major Chinese and Hong Kong stock indices that we follow.

Notes:

Shanghai Composite Index (SHCOMP): Tracks all stocks (A and B shares) traded on the Shanghai Stock Exchange.

CSI 300 Index (SHSZ300): Represents the top 300 stocks traded on the Shanghai and Shenzhen Stock Exchanges.

China A50 Index (512150 CH): Comprises the top 50 A-share companies listed on the Shanghai and Shenzhen Stock Exchanges.

ChiNext Price Index (159954 CH): Focuses on innovative and high-growth enterprises listed on the Shenzhen Stock Exchange.

SSE STAR 50 Index (83151 HK): Represents the top 50 companies listed on the Shanghai Stock Exchange’s STAR Market, emphasising science and technology innovation.

Hang Seng Index (HSI): Measures the performance of the largest companies listed on the Hong Kong Stock Exchange.

Hang Seng China Enterprises Index (2828 HK): Includes major H-share companies listed in Hong Kong.

Currency Considerations:

Chinese Indices (SSEC, CSI300, China A50, CNT, STAR50): These indices are denominated in Chinese Yuan (CNY). To present their performance in USD terms, currency exchange rate fluctuations between the CNY and USD have been considered.

Hong Kong Indices (HSI, HSCEI): Denominated in Hong Kong Dollars (HKD). Their performance in USD terms reflects the HKD/USD exchange rate stability, as the HKD is pegged to the USD.

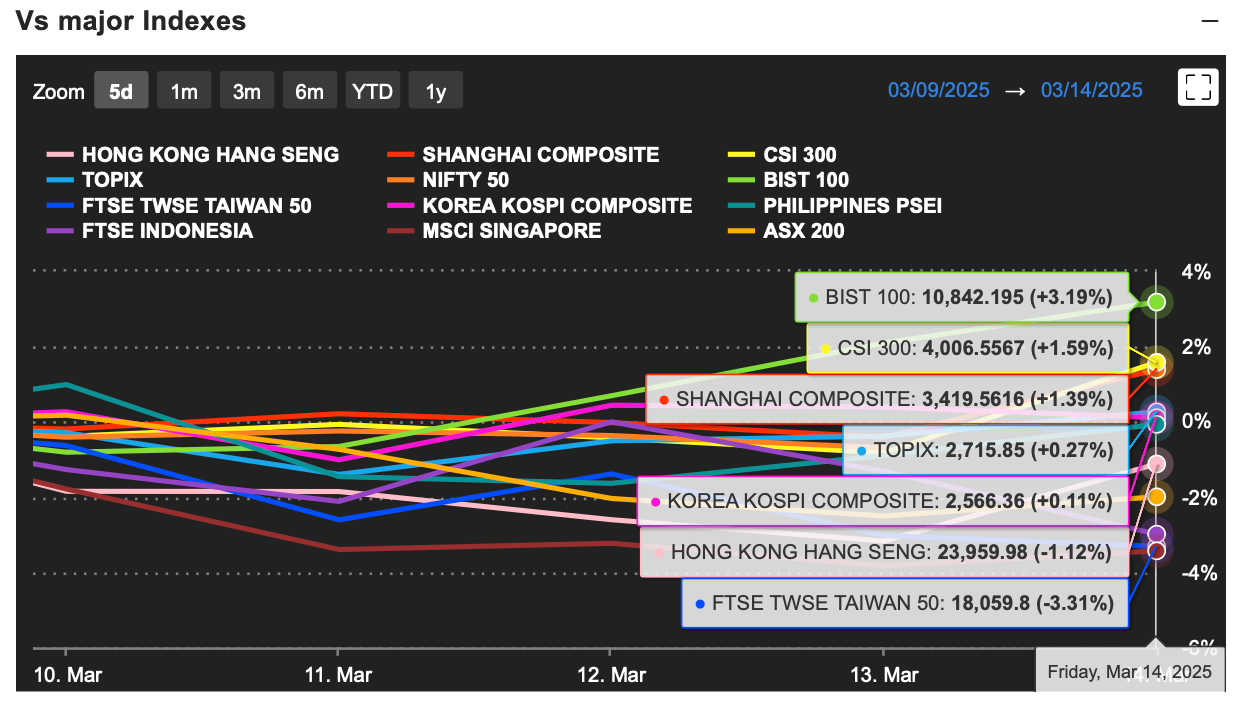

Weekly Relative Performance Observations:

Performance in Chinese Equities

HSCEI ETF (-0.33%)

Highlights: HSCEI ETF posted a slight decline for the week, underperforming some onshore indices.

Context: The Hong Kong market remained under pressure from weak investor sentiment and lingering concerns over China’s economic recovery.

Hang Seng Index (-1.12%)

Highlights: The HSI declined for the week, weighed down by tech and property sectors.

Context: Despite a positive single-day performance, broader weakness in Hong Kong-listed Chinese stocks and global risk sentiment dragged the index lower.

Shanghai Composite (+1.39%)

Highlights: The SHCOMP posted moderate gains, led by selective sector strength in financials and consumer stocks.

Context: Investor sentiment improved slightly as policymakers emphasized stability, but caution remained ahead of key economic data releases.

CSI 300 (+1.59%)

Highlights: The CSI 300 outperformed other major indices in China, with gains led by defensive sectors.

Context: The market responded to supportive policy expectations, but investors remained cautious amid global economic uncertainty.

ChiNext (+2.80%)

Highlights: The ChiNext index saw the strongest performance among Chinese indices, driven by tech and biotech rebounds.

Context: Renewed interest in growth stocks, coupled with expectations of government support for innovation and high-tech industries, fueled gains.

Regional Peers’ Performance

TOPIX (Japan) (+0.27%)

Highlights: Japanese equities posted slight gains, reflecting resilience in global macro conditions.

Context: Corporate reforms continued to support sentiment, but external economic risks limited stronger upside.

KOSPI (South Korea) (+0.11%)

Highlights: The KOSPI saw muted performance, weighed down by semiconductor sector concerns.

Context: Global uncertainty and chip sector headwinds offset positive sentiment from recent earnings.

NIFTY 50 (India) (+1.93%)

Highlights: The Indian market performed strongly, benefiting from domestic economic resilience.

Context: Solid macroeconomic data and strong foreign investor inflows supported gains.

Key Takeaways for Chinese Markets

• Resilience in Onshore Equities: The Shanghai Composite and CSI 300 outperformed Hong Kong-listed stocks, suggesting stronger domestic confidence.

• Tech and Growth Stocks Rebounding: ChiNext’s strong weekly gain highlights renewed interest in high-growth sectors, driven by expectations of policy support.

• Cautious Optimism Persists: Investors remain selective, awaiting clearer policy signals and macroeconomic data before taking broader positions.

In the news this week:

China’s National People’s Congress Concludes Amid Economic Uncertainty

Announced by: National People’s Congress (NPC)

Date: March 11, 2025

Details: The two sessions have fully concluded now. We have done a review of everything coming out of it here.

This Indicates: China is navigating economic challenges, including trade tensions and domestic economic slowdown, with a cautious approach to policy implementation, being ready to respond to US challenge.

China and Russia Urge U.S. to Lift Sanctions on Iran

Announced by: Governments of China and Russia

Date: March 14, 2025

Details: Russia and China are urging President Trump to lift sanctions on Iran, cease military threats, and rejoin the 2015 nuclear deal. This call follows talks in Beijing, responding to Trump’s letter to Iran’s Supreme Leader threatening military action unless Iran halts its nuclear program. Britain and France have hinted at reinstating UN sanctions, initially lifted under the 2015 agreement, due to Iran exceeding uranium enrichment limits after Trump’s 2018 withdrawal from the deal. Despite US sanctions, Russia and China have aided Iran, though its economy suffers. The summit underscores the rift between the Russia-China axis and the West.

This Indicates: China and Russia are aligning their foreign policies to counter U.S. actions regarding Iran, reflecting a strategic partnership aimed at challenging Western influence in global geopolitical matters.

China to Crack Down on Stock Market Misinformation Amid AI Concerns

Announced by: China Securities Regulatory Commission

Date: March 15, 2025

Details: China’s securities regulator will intensify actions against the spread of fake news in the stock market, which has been exacerbated by AI advancements, as reported by official media. The China Securities Regulatory Commission aims to collaborate with police and cyberspace regulators to address this issue robustly. Artificial intelligence is increasingly used to create and disseminate false information, misleading investors with promises of quick wealth. In response, the Commission plans to proactively debunk stock market rumors by providing clarifications and enhancing investor education to improve their ability to detect misinformation.

This Indicates: China is proactively addressing the challenges posed by AI-driven

China Criticises G7 Statements on Maritime Security

Announced by: Chinese Foreign Ministry

Date: March 15, 2025

Details: China vehemently criticized the Group of 7 (G7) nations for their joint statement condemning China’s actions in maritime regions, labeling the G7’s accusations as “filled with arrogance, prejudice, and malicious intentions.” The G7’s statement reproached China for its provocative actions in the South China Sea, including land reclamations and militarization of outposts, asserting that such activities disrupt regional stability. They also reaffirmed the importance of peace across the Taiwan Strait. In response, China rejected these claims, accusing the G7 of interfering in its internal affairs and vowed to make their opposition known to Canada, where the meeting was held.

This Indicates: Escalating diplomatic tensions between China and the West over maritime security issues, highlighting disputes over territorial claims and regional stability in the South China Sea and Taiwan Strait.

Data Released This Week:

Shanghai & Shenzhen Second-Hand Home Sales Surge

Announced by: Shenzhen Real Estate Intermediary Association, Yicai.com

Date: March 10, 2025

Event: February–March 2025 Second-Hand Home Sales Report

Details:

Shanghai: Second-hand home online transactions hit 1,432 units on March 8, surpassing 1,400 for the first time in 2025. This marks a continued uptrend following a record-high of 1,466 units on December 28, 2024. Demand is driven by inelastic homebuyer demand, signaling market stabilization despite previous slowdowns.

Shenzhen: 1,812 second-hand home transactions were recorded in the 10th week of 2025 (March 3–9), reflecting an 11.6% weekly increase. The market has seen five consecutive weeks of growth, with consumer confidence improving and more buyers entering the market.

This Indicates: The residential property market is rebounding, particularly in second-hand home sales, despite broader economic concerns. Increasing homebuyer activity suggests rising confidence and a potential stabilization in China’s real estate market, which has been under pressure from weak demand and regulatory constraints in previous months. Policymakers may ease further property restrictions if demand continues to recover, supporting home prices and stimulating the broader economy.

China New Yuan Loans – February 2025

Announced by: People’s Bank of China (PBOC)

Date: March 14, 2025

Event: February 2025 New Yuan Loans and Total Social Financing Data

Details:

New Yuan Loans: CNY 1,010 billion in February, significantly lower than January’s record CNY 5,130 billion and below the consensus estimate of CNY 1,275 billion. Year-over-year, the figure also fell from CNY 1,450 billion in February 2024.

Credit demand weakened following a front-loading of bank loans in January and a slower-than-expected economic recovery.

Total Social Financing (TSF): Fell to CNY 2,290 billion from CNY 7,060 billion in January, reflecting weaker overall credit and liquidity conditions.

This Indicates:

Policy Constraints: While authorities have been trying to stimulate credit growth, banks appear more cautious about lending, possibly due to rising defaults and weak business confidence.

Potential for More Stimulus: The sharp drop in credit issuance could prompt the PBOC to cut interest rates or ease lending conditions further in the coming months.

China Money Supply Data – February 2025

Announced by: People’s Bank of China (PBOC)

Date: March 14, 2025

Event: February 2025 Money Supply Statistics

Details:

M2 Money Supply:

Growth Rate: Increased by 7.0% year-on-year (YoY), aligning with market expectations.

Total Amount: Reached approximately ¥320.53 trillion as of February 28, 2025.

M1 Money Supply:

Growth Rate: Rose by 0.1% YoY, slightly below the anticipated 1.0% increase.

M0 Money Supply:

Growth Rate: Expanded by 9.7% YoY, indicating a substantial rise in the most liquid form of money.

This Indicates:

Stable Broad Money Growth: The M2 growth rate suggests a steady expansion in the overall money supply, reflecting ongoing monetary support for economic activities.

Sluggish Narrow Money Growth: The minimal increase in M1 points to cautious business sentiment, as M1 primarily comprises cash and demand deposits, which are closely linked to corporate transactions.

Robust Cash Circulation: The significant rise in M0 indicates increased cash in circulation, potentially due to seasonal factors or heightened consumer spending.

Complete Index Performance List:

General Trends

Chinese equity markets delivered mixed performances this week, with mainland indices posting moderate gains while Hong Kong markets struggled.

The Shanghai Composite Index (SSE) advanced +1.39% to 3,419.56, reflecting measured optimism amid policy expectations.

The CSI 300 (SSE-SZSE 300) gained +1.59% to 4,006.56, showing stability in large-cap A-shares, particularly in financials and industrials.

The ChiNext Index, a benchmark for growth-oriented stocks, saw a smaller weekly gain of +0.97%, indicating cautious rotation into high-growth sectors.

In Hong Kong, markets underperformed, with most indices ending the week in the red:

The Hang Seng Index (HSI) declined -1.12%, weighed down by weakness in property and consumer sectors.

The Hang Seng Tech Index (HS TECH) fell -2.59%, as investors remained wary of U.S.-China tensions affecting Chinese tech stocks.

The Hang Seng China Enterprises Index (HSCEI) dropped -0.40%, despite a late-week rebound.

Relative Outperformance

CSI 300 (+1.59%) – Large-cap A-shares showed resilience, supported by institutional buying.

Shanghai Composite (SSE) (+1.39%) – The index posted modest gains, aided by policy-driven sentiment.

Shenzhen 100 (+1.27%) – Growth names attracted selective buying, though enthusiasm remained muted.

SSE Commodity Equity Index (+3.81%) – The strongest performer, driven by energy and raw materials stocks.

Sector-Specific Dynamics

Technology & Innovation

The HS TECH Index fell -2.59%, as tech stocks struggled with regulatory and geopolitical uncertainties.

ChiNext (+0.97%) posted weaker gains than in previous weeks, indicating less aggressive risk-taking in growth stocks.

Financials & Real Estate

The HSI Financials Index declined -0.75%, reflecting pressure on banking and insurance stocks.

HSI Property (-1.16%) dropped amid weak confidence in China’s real estate market, despite improved second-hand home sales.

Industrials & Commodities

The SSE Commodity Equity Index surged +3.81%, as rising global commodity prices boosted Chinese resource stocks.

HSI Industrials (+2.85%) outperformed, suggesting continued investor interest in infrastructure and manufacturing sectors.

Large-Cap vs. Small-Cap Performance

Large-Cap Indices: The CSI 300 (+1.59%) and Shanghai Composite (+1.39%) held firm, indicating institutional support.

Small-Cap & Innovation-Focused Indices: The ChiNext (+0.97%) and Shenzhen 100 (+1.27%) posted modest gains, suggesting selective risk appetite in growth stocks.

Key Takeaways

Commodity Stocks Led Gains

The SSE Commodity Equity Index (+3.81%) was the strongest performer this week, benefiting from rising global demand for raw materials. This suggests that investors are positioning themselves for a potential rebound in global industrial activity, particularly in energy and metals.

Mainland Markets Showed Stability Amid Policy Expectations

While the Shanghai Composite (+1.39%) and CSI 300 (+1.59%) posted moderate gains, they reflected cautious optimism rather than broad-based enthusiasm. This aligns with expectations of further stimulus from Beijing, but without immediate catalysts, investors remained hesitant.

Hong Kong Markets Struggled, Weighed Down by Tech and Property Sectors

The HSI (-1.12%) and HS TECH (-2.59%) signaled continued selling pressure, particularly in technology and real estate. Investor sentiment remains fragile, with concerns about China’s economic slowdown, high debt levels in property firms, and regulatory risks for tech companies.

Selective Risk Appetite for Growth Stocks

The ChiNext (+0.97%) and Shenzhen 100 (+1.27%) saw only modest gains, suggesting that investors are still hesitant to aggressively rotate into high-growth, high-valuation stocks. This reflects uncertainty about earnings growth in China’s private sector, particularly for startups and innovation-driven firms.

Foreign Investment Remains Cautious

While Hong Kong stocks briefly rebounded, the weekly decline in key indices suggests that foreign capital is still taking a wait-and-see approach. This underscores broader concerns about U.S.-China relations, potential trade restrictions, and China’s economic policy direction.

Overall, while policy expectations helped stabilize mainland markets, Hong Kong’s underperformance suggests lingering investor skepticism. A more sustained market rally will likely require stronger economic data and clearer policy signals from Beijing.

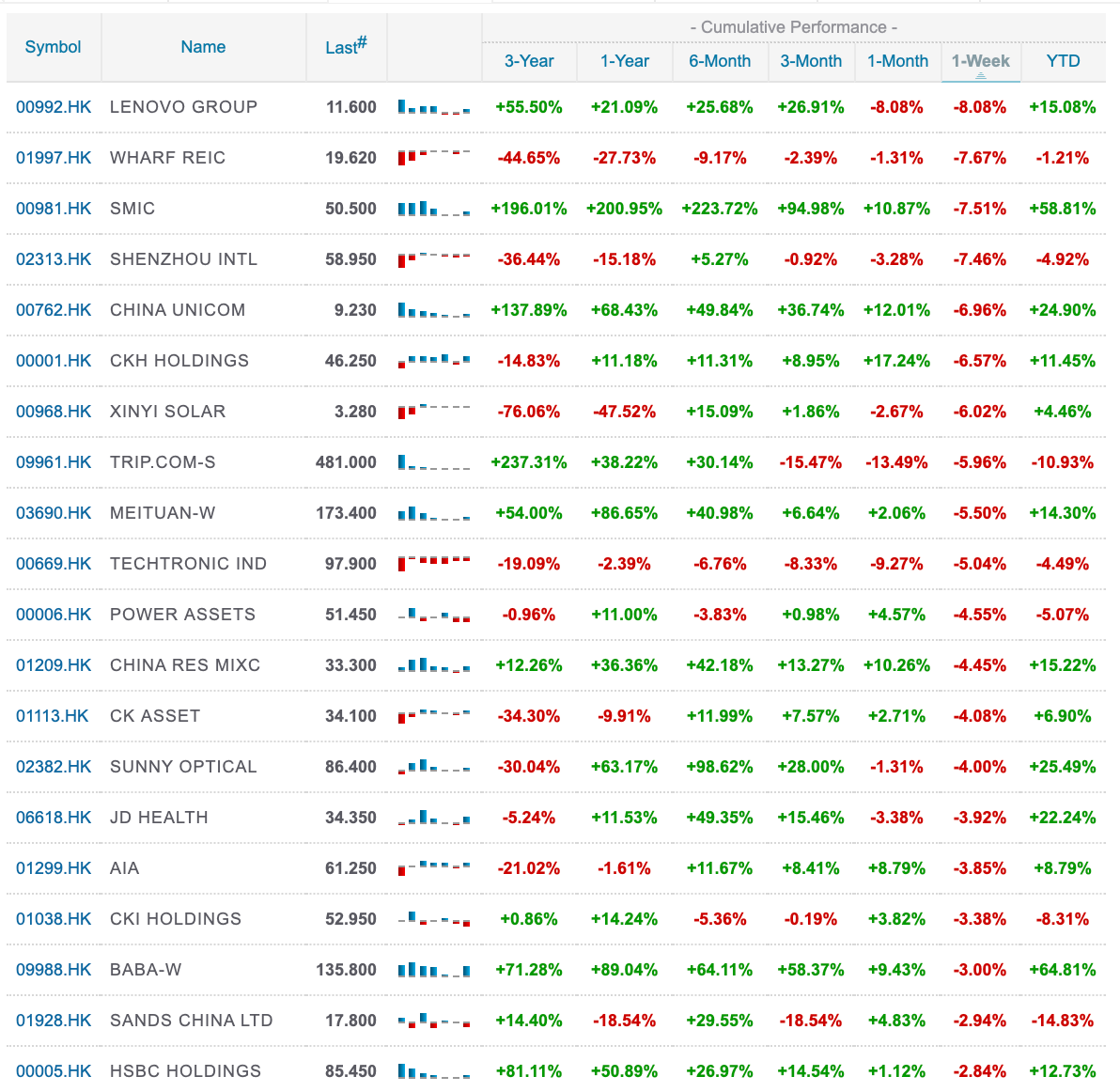

Top 20 Index Constituents:

Bottom 20 Index Constituents:

Corporate News and Results this week:

Li Auto Forecasts Decline in Q1 Revenue

Announced by: Li Auto

Date: March 14, 2025

Details: Li Auto reported a 20.4% year-over-year increase in vehicle deliveries and a 6.1% rise in revenue for Q4 2024, aligning with analyst expectations. However, the company projected a decline in Q1 2025 revenue, estimating sales between $3.2 billion and $3.4 billion, below the anticipated $4.9 billion. Profit margins decreased to 19.7%, reflecting intense market competition and reduced consumer spending in China.

This Indicates: The forecasted revenue decline underscores the challenges faced by Chinese electric vehicle manufacturers amid a competitive market and cautious consumer spending. The results are expected to improve in 2Q25 as the new fully electric Li i8 SUV makes its debut, followed by an expanded range of EVs and an updated Li6-9 family.

China’s Commerce Ministry Engages Walmart on Supplier Pricing

Announced by: China’s Ministry of Commerce

Date: March 11, 2025

Details: Officials from China’s Ministry of Commerce met with representatives from Walmart to address concerns about the retailer pressuring Chinese suppliers to reduce prices to offset U.S. tariffs. Reports indicated Walmart requested price cuts of up to 10% per tariff round, potentially forcing suppliers to absorb the full cost of U.S. tariffs.

This Indicates: The meeting highlights the complexities in global supply chains and the impact of trade tensions on corporate relationships and pricing strategies. Its not as easy as raising prices by 10% but nor is it as easy as squeezing your supplier by 10%.

China to Crack Down on Stock Market Misinformation

Announced by: China Securities Regulatory Commission

Date: March 15, 2025

Details: The China Securities Regulatory Commission announced plans to intensify actions against the spread of fake news in the stock market, exacerbated by advancements in artificial intelligence. The commission aims to collaborate with police and cyberspace regulators to address the issue robustly, as AI technologies have been increasingly used to create and disseminate false information, misleading investors.

This Indicates: The initiative underscores the regulatory body’s commitment to maintaining market integrity and protecting investors from misinformation in an increasingly digital landscape.

China Expresses Unhappiness Over BlackRock’s Panama Ports Deal

Announced by: Chinese State-Owned Newspaper

Date: March 15, 2025

Details: China expressed dissatisfaction with CK Hutchison Holdings’ agreement to sell a majority stake in Panama ports to a consortium led by BlackRock. A Chinese state-owned newspaper criticized the deal, suggesting it could politicize the Panama Canal and hinder China’s trade. Consequently, shares in CK Hutchison fell by 6.7%.

This Indicates: The criticism reflects China’s sensitivity to foreign control over strategic trade routes and its potential impact on Chinese commerce.

Upcoming Earnings Announcements

March 17, 2025: Hygon Information Technology and WuXi AppTec are scheduled to release their earnings reports, providing insights into the tech and healthcare sectors.

March 18, 2025: Xiaomi and China Unicom will announce their earnings, shedding light on the technology and telecommunications industries.

March 19, 2025: Tencent is set to release its Q4 2024 report, with analysts focusing on gaming and cloud service margins.

Otherwise not a lot on the docket in terms of macro data, so we’ll focus on those earnings and on any noise around tariffs and trade deal proposals coming-out off the US.

Have a great week,

Leonid

Minor formatting request, could you move the regular disclaimer and index/currency reference tables to the end of these updates? I often listen to articles in the Substack app and it's difficult to skip over these precisely since you can only move in 30 second blocks. Thanks!