China Weekly Wrap

a week that was 22-27 December 2024

While the Western World took a week off (well nearly), China was up and running. We’ve had a fun trading week in the A-shares and Even HK had a 3 full sessions, even though Stock Connect was closed for 2 days. There were also a couple of big news items that we’ll get to. First thing’s first though - we’ve been busy on the substack and have finalised our 2025 outlook.

All the articles can be found here

We have also done a pension reform overview here - do please have a read if you haven’t already, it’s important.

We also recorded the first Perspecticast - do check it out here , like and subscribe, as it were.

Next Week is Energy Week 1, where we’ll work on the Oil outlook. It will be followed by China Majors review and finally the Chemicals space overview. I am also keen to cover gas, gasification of city supplies, LNG impact and LNG import players, but that is probably a goal for week 2 or 3. While i’m not sure how many posts all of this will take my goal is to cover this space in some detail.

As some of you know my background is in commodities, and more specifically Oil and Gas. I still consult for E&P companies on occasion. In fact those engagements over the years have led me to have a bit of personal experience of working with the Chinese Companies in the space. This included Majors, as well as now defunct but once high-flying private companies and big regional importers over the years, so I think I have a pretty good handle on them and will be happy to share that, to the degree its still relevant.

Perhaps more immporatnaly I am very eager to revisit the state of China’s domestic O&G space, with energy reforms ongoing. I am very keen to start writing, so much so I even squeezed these couple of paragraphs in here, it should be good. I am not sure how much will be paywalled, but I think everything beyond general market reviews, as I believe this to be quite valuable additive to premium subscribers. Put it this way, if I can’t find a good long in the Asian Energy space, I probably should take some time off and reflect.

Speaking of premium subscribers, Panda Portfolio review for them is coming out on Sunday as per usual now, and there’s been excitement there, both positive and negative. If you fancy joining in on the fun, by all means do.

A quick reminder that there’s a special offer in place until the end of Eastern Orthodox Christmas (7th January).

With all that out of the way, on to the Weekly Wrap.

As of December 28, 2024, here’s a summary of the weekly, month-to-date (MTD), and year-to-date (YTD) performances of major Chinese and Hong Kong stock indices that we follow.

Notes:

• Shanghai Composite Index (SHCOMP): Tracks all stocks (A and B shares) traded on the Shanghai Stock Exchange.

• CSI 300 Index (SHSZ300): Represents the top 300 stocks traded on the Shanghai and Shenzhen Stock Exchanges.

• China A50 Index (512150 CH): Comprises the top 50 A-share companies listed on the Shanghai and Shenzhen Stock Exchanges.

• ChiNext Price Index (159954 CH): Focuses on innovative and high-growth enterprises listed on the Shenzhen Stock Exchange.

• SSE STAR 50 Index (83151 HK): Represents the top 50 companies listed on the Shanghai Stock Exchange’s STAR Market, emphasising science and technology innovation.

• Hang Seng Index (HSI): Measures the performance of the largest companies listed on the Hong Kong Stock Exchange.

• Hang Seng China Enterprises Index (2828 HK): Includes major H-share companies listed in Hong Kong.

Currency Considerations:

• Chinese Indices (SSEC, CSI300, China A50, CNT, STAR50): These indices are denominated in Chinese Yuan (CNY). To present their performance in USD terms, currency exchange rate fluctuations between the CNY and USD have been considered.

• Hong Kong Indices (HSI, HSCEI): Denominated in Hong Kong Dollars (HKD). Their performance in USD terms reflects the HKD/USD exchange rate stability, as the HKD is pegged to the USD.

Weekly Relative Performance Observations:

Shanghai A Index Sees Modest Gains

The Shanghai A Index rose by +0.95%, reflecting investor optimism. This uptick aligns with recent analyses suggesting that the A-share market is attracting increased capital inflows, indicating growing investor confidence.

Shenzhen Index Experiences Decline

In contrast, the Shenzhen Index declined by -1.32%, underperforming other major Chinese indices. This downturn may be attributed to sector-specific challenges or profit-taking activities, particularly in technology and growth-oriented stocks that dominate the Shenzhen market.

Comparative Performance with Regional Markets

While the Shanghai A Index’s modest gain was comparable to India’s Nifty 50, which increased by +0.96%, it lagged behind the robust performances of Taiwan’s FTSE TWSE Taiwan 50 (+4.13%) and Japan’s Nikkei 225 (+4.03%). The stronger rallies in Taiwan and Japan could be due to localized economic policies or sectoral developments favoring their markets.

In the news this week:

As mentioned at the top, this was a busy news week in China. It focused on critical areas such as stock market reforms, accommodative monetary policies, and fiscal measures to stimulate economic growth. Upward GDP revisions highlight resilience in core sectors, while significant AI investments signal China’s determination to lead in tech innovation. These developments reflect Beijing’s dual approach to stabilise short-term challenges while building a foundation for long-term economic transformation.

Stock Market and Financial Reforms

Announced by: People’s Bank of China (PBOC) and China Securities Regulatory Commission (CSRC)

Date: December 27, 2024

Event: Policy Announcement

Details:

The PBOC and CSRC jointly announced significant reforms aimed at modernizing China’s stock markets to attract domestic and foreign investors. Key measures included:

• Corporate Governance: The CSRC introduced a mandate requiring newly listed companies to establish audit committees, replacing traditional supervisory boards. This aligns with global governance practices to improve internal controls and accountability.

• Market Development: The PBOC emphasized its role in advancing stock market reforms to improve transparency, efficiency, and liquidity. This includes encouraging higher-quality listings and creating a more predictable regulatory environment.

• Investor Confidence: The reforms are expected to address long-standing concerns about corporate governance and market volatility, critical to fostering confidence among institutional investors.

Monetary Policy Updates

Announced by: People’s Bank of China (PBOC)

Date: December 27, 2024

Event: Monetary Policy Statement

Details:

The PBOC reaffirmed its commitment to accommodative monetary policy to support economic recovery and address liquidity challenges. Key measures included:

• Liquidity Support: The PBOC aims to use tools like reserve requirement ratio (RRR) cuts and targeted lending to maintain ample liquidity in the financial system, especially for small and medium enterprises (SMEs) and infrastructure projects.

• Countercyclical Adjustments: Emphasis on countercyclical regulations to stabilize economic growth amid external uncertainties, such as global economic slowdowns and geopolitical risks.

• Focus on Stability: The central bank reiterated its goal to balance growth with financial stability, ensuring support for real estate, manufacturing, and emerging industries.

Economic Growth and GDP Revision

Announced by: National Bureau of Statistics (NBS)

Date: December 26, 2024

Event: GDP Data Revision

Details:

The NBS revised its 2023 GDP figures upward, reflecting stronger-than-expected performance in key sectors. Key highlights included:

• GDP Revision: The revised GDP for 2023 was increased by 3.4 trillion yuan, reaching 129.4 trillion yuan, a growth of 2.7% from earlier estimates. The revision reflects robust growth in manufacturing and services.

• Sectoral Strength: Strong performance in domestic consumption, bolstered by recovery in the retail and real estate sectors, played a major role in the revision.

• Economic Outlook: The World Bank raised its forecast for China’s 2024 GDP growth to 4.9%, highlighting improving economic fundamentals and progress in structural reforms.

Fiscal Measures to Boost Investment

Announced by: State Council and National Fiscal Work Conference

Date: December 25, 2024

Event: Fiscal Policy Announcement

Details:

China introduced new fiscal measures to support infrastructure development and stabilize local government finances. Key initiatives included:

• Special Bonds: Issuance of 3 trillion yuan in special treasury bonds for 2025 to fund infrastructure upgrades, recapitalize state-owned banks, and drive regional development.

• Policy Reforms: Adoption of zero-based budgeting and tax reforms to optimize resource allocation and improve fiscal efficiency.

• Local Government Support: Increased transfer payments to local governments to strengthen financial capacities, enabling them to focus on high-priority areas like transportation, urban renewal, and green energy projects.

Data Released This Week:

The big event on December 27th, 2024, was the release of revised 2023 economic data and insights by the National Bureau of Statistics (NBS)during a key year-end announcement. This event, which typically takes place annually, aims to update key economic indicators based on comprehensive reviews, new data sources, and refined methodologies. Summary here and a detailed review of key numbers to follow.

Key Highlights:

Revised GDP Data: The NBS updated China’s 2023 GDP to 129.4 trillion yuan, reflecting an upward revision of 3.4 trillion yuan (2.7%)from initial estimates. This revision was attributed to stronger-than-expected growth in the manufacturing and services sectors, alongside recovering domestic consumption.

Employment Insights: The NBS reported a total of 428.98 million people employed in secondary (industrial) and tertiary (service) sectors, marking an increase of 11.9% since 2018. This highlighted the country’s continued shift toward urbanization, industrialization, and a service-oriented economy.

Enterprise Growth: The number of legal entities in secondary and tertiary industries grew to 33.27 million, a 52.7% increase from 2018, reflecting robust private sector expansion and improved business environments.

This annual data revision is significant as it offers a more accurate reflection of the past year’s economic performance, shaping both domestic policy direction and global perceptions of China’s economy.

Employment Growth in Secondary and Tertiary Industries

Announced by: National Bureau of Statistics (NBS)

Date: December 25, 2024

Details:

The secondary (industrial) and tertiary (service) industries reported total employment of 428.98 million people at the end of 2023, marking an increase of 11.9% since 2018.

These sectors continue to dominate employment, driven by industrial upgrades, urbanization, and expansion of the service economy.

The top three employment contributors were:

Manufacturing: Bolstered by China’s industrial modernization efforts and the global demand for Chinese exports.

Wholesale and Retail Trade: A reflection of the growth in domestic consumption and e-commerce.

Construction: Supported by ongoing infrastructure projects and urban redevelopment.

Growth in Legal Entities in Key Industries

Announced by: National Bureau of Statistics (NBS)

Date: December 25, 2024

Details:

The total number of legal entities in secondary and tertiary industries reached 33.27 million, an increase of 52.7% from 2018.

This surge reflects the rapid rise of private enterprises in China, particularly in manufacturing, technology, and services, which have seen exponential growth as the private sector now accounts for over 60% of the country’s GDP and 80% of urban employment. Structural reforms, such as streamlined business registration processes and reduced bureaucratic barriers, have encouraged entrepreneurship and fostered innovation. The number of newly registered companies in China surpassed 27 million in 2023, highlighting this trend. Additionally, the shift from state-dominated industries to a more diversified, private-sector-led economy has been driven by policies promoting market competition and foreign investment, with private companies playing a crucial role in emerging fields like artificial intelligence, green technology, and advanced manufacturing.

Trade and Consumption Data

Announced by: Ministry of Commerce

Date: December 24, 2024

Details:

A fiscal stimulus package for trade-ins of consumer goods in 2024 resulted in 150 billion yuan in spending, generating over 1 trillion yuan in sales.

Key categories included home appliances (e.g., refrigerators, TVs), which have been targeted to support domestic manufacturing while increasing consumer spending.

These measures are part of broader efforts to drive domestic consumption, which is a critical pillar of China’s economic strategy to reduce reliance on exports.

Industrial Profits Decline Moderates

Announced by: National Bureau of Statistics (NBS)

Date: December 27, 2024

Event: Monthly Industrial Profit Data Release

Details:

The NBS released its latest industrial profit data, highlighting continued pressure on China’s manufacturing and industrial sectors. Key findings included:

• Monthly Decline Moderates: Profits for major industrial firms fell by 7.3% year-on-year in November, improving from the 10% decline recorded in October, suggesting a modest recovery in the sector.

• Cumulative Performance: For the first eleven months of 2024, industrial profits were down 4.7% year-on-year, a steeper decline compared to the 4.3% drop reported for January to October.

• Sectoral Weakness: The overall decline reflects headwinds such as weak domestic consumption, ongoing challenges in the housing market, and geopolitical uncertainties impacting trade and exports.

• Enterprise Coverage: The data includes industrial enterprises with annual revenues of at least 20 million yuan, providing insights into the performance of medium and large-scale manufacturing and industrial firms.

• Government Response: To counter these declines, the Chinese government is deploying fiscal measures, including the issuance of special treasury bonds, and enhancing liquidity to support the industrial sector and broader economy.

Complete Index Performance List:

for the week 22-27 Dec 2024

5 Observations:

Broader Market Resilience

The Shanghai Composite Index (SSE) and SSE A Index gains of +0.95% suggest that China’s broader equity market remains stable, supported by recent fiscal and monetary policy measures. This resilience likely reflects confidence in government initiatives, such as infrastructure investments and liquidity support, as well as optimism about economic recovery in 2025. The performance indicates that large-cap, stable companies are seen as safer bets in a somewhat volatile economic environment.

Shift Away from Growth and Innovation

The significant decline in the SSE SME Innovation Index (-2.90%) and the slight drop in the CHINEXT Index (-0.22%) highlight a cooling interest in high-growth and innovation-oriented sectors. Investors may be wary of these riskier segments, especially amid global economic uncertainties and slower-than-expected recovery in domestic consumption. This trend could also indicate profit-taking in sectors like tech and biotech, which have performed well previously, as investors rotate into more traditional and income-generating sectors.

Preference for Stability and Blue-Chip Stocks

Strong weekly gains in the SSE Mega-cap Index (+2.89%) and SSE 380 Index (+0.32%) show a clear preference for large and mid-cap stocks. These segments are often perceived as less volatile and better positioned to benefit from government-led recovery efforts. The focus on mega-caps aligns with investor sentiment favoring companies with stable earnings, robust fundamentals, and defensive characteristics in uncertain times.

Sectoral Rotation into Commodities and Dividends

The SSE Dividend Index (+1.60%) and SSE Commodity Equity Index (+0.23%) outperformed other specialized indices, reflecting a shift toward income-generating and commodity-linked stocks. This sector rotation suggests that investors are hedging against macroeconomic uncertainties by targeting reliable dividend payers and industries with ties to global demand for commodities, such as energy and metals. This aligns with China’s structural push toward resource efficiency and green energy investments.

Continued Struggles for Tech-Oriented Indices

The underperformance of the Shenzhen 100 (+0.75%) and CHINEXT (-0.22%) indices signals ongoing challenges for growth and tech-oriented firms. These sectors may be experiencing pressure from weaker funding conditions, global tech competition, and cautious investor sentiment toward high-valuation stocks. The recent industrial profit data, showing declines, may also contribute to concerns about tech-driven industrial performance.

Broader Implications:

Cautious Optimism: The overall market resilience suggests cautious optimism, driven by government policies. However, the performance divergence between blue-chip and growth stocks reflects selective risk-taking by investors.

Investor Rotation: The move toward dividend and commodity stocks signals a defensive stance, possibly in anticipation of global economic uncertainties in early 2025. This is in line with the SOE, Corp governance and Yield themes.

Tech Pressure: Challenges in growth and tech sectors may persist until there is clearer visibility on consumption recovery, funding conditions, and global tech competition. Again in-line with the view express in the outlook.

So far so good.

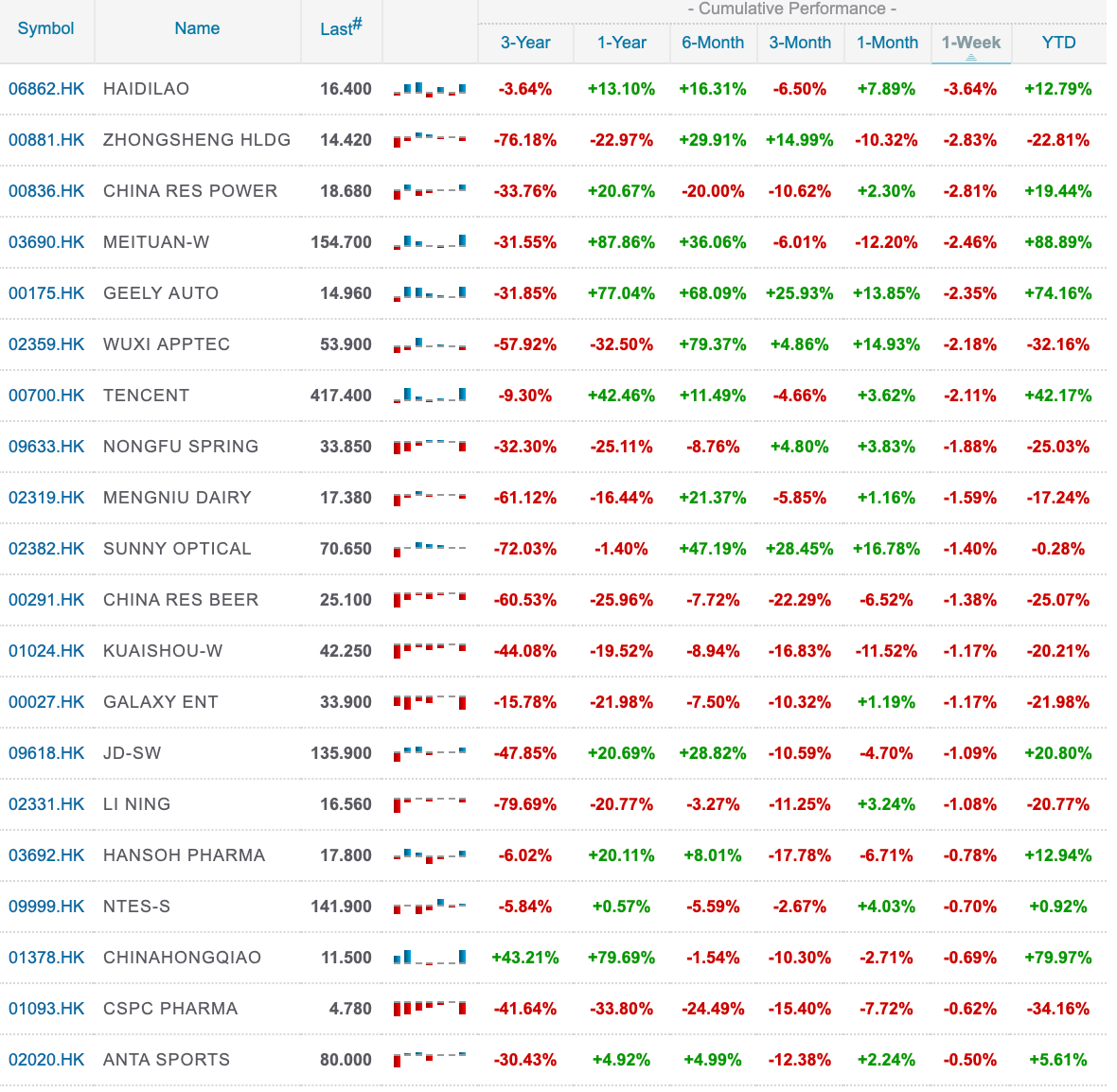

Top 20 Index Constituents:

Bottom 20 Index Constituents:

Corporate News this week:

Xiaomi Expands into AI Development

Date: December 26, 2024

Event: Strategic Expansion Announcement

Details:

Xiaomi revealed plans to build a large-scale GPU cluster to train AI models, signaling its ambition to strengthen its position in artificial intelligence and cloud computing. The cluster will reportedly feature thousands of GPU cards, showcasing Xiaomi’s commitment to competing with global tech giants in AI innovation.

This initiative aligns with Beijing’s push for self-reliance in technology, especially amid ongoing geopolitical tensions over semiconductor and AI export restrictions.

CATL Secures EV Battery Supply Agreements and Unveils Smart Chassis

Date: December 24, 2024

Event: Product Announcement

Details:

CATL announced a multi-year battery supply deal with two major European automakers, bolstering its position as the world’s largest EV battery supplier and reinforcing confidence in its global market leadership.

Additionally, CATL unveiled its latest intelligent chassis system, an integrated platform combining EV batteries, motors, and control units. This new product aims to streamline EV manufacturing for automakers by providing a “plug-and-play” solution.

The smart chassis is expected to reduce vehicle weight and improve energy efficiency, aligning with automakers’ goals for cost reduction and performance optimization in next-generation EVs.

Tesla Shanghai Plant Manager Joins Envision Group

Announced by: Tesla Shanghai & Envision Group

Date: December 24, 2024

Event: Leadership Transition

Details:

Song Gang, Tesla’s Shanghai Plant Manager, resigned to join Envision Group, a leading Chinese company in wind turbines, energy storage, and green hydrogen. This leadership change reflects Tesla’s ongoing adjustments in China as local competitors like BYD and NIO intensify competition in EV manufacturing. Envision’s recruitment of Song highlights its ambition to scale up renewable energy solutions globally.

BYD Expands Global Footprint

Date: December 23, 2024

Event: Factory Announcement

Details:

BYD announced plans to establish a new EV manufacturing plant in Indonesia, marking its latest effort to expand its global footprint. The plant will produce affordable electric cars for Southeast Asian markets, leveraging Indonesia’s resources for battery raw materials, such as nickel.

This expansion aligns with BYD’s strategy to dominate emerging markets while continuing its aggressive growth in Europe.

Alibaba Cloud Unveils New AI Tools

Date: December 22, 2024

Event: Product Launch

Details:

Alibaba Cloud launched a suite of AI-driven cloud tools, targeting industries like healthcare, e-commerce, and logistics.

The tools include AI-powered supply chain optimizers, chatbots, and advanced cloud storage solutions, further strengthening Alibaba’s cloud computing and AI ecosystem.

This comes as Alibaba faces intensified competition from Tencent Cloud and Huawei in China’s cloud market, with AI being a critical battleground.

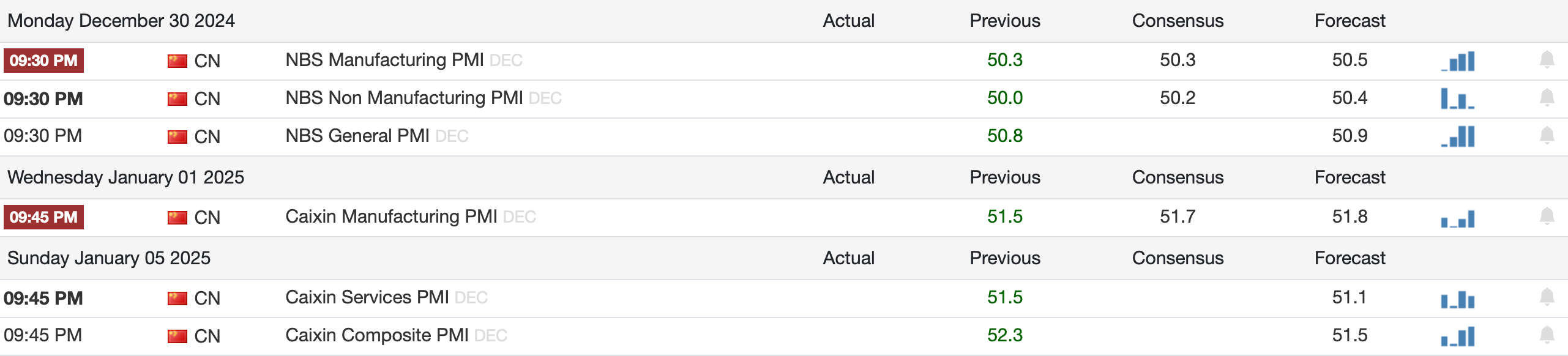

Not a very busy Econ Calendar next week:

Have a Great weekend and the week ahead!

Leonid