China Weekly Wrap: Export Surprise Edition

Week of 4-10 May 2026

Good Morning,

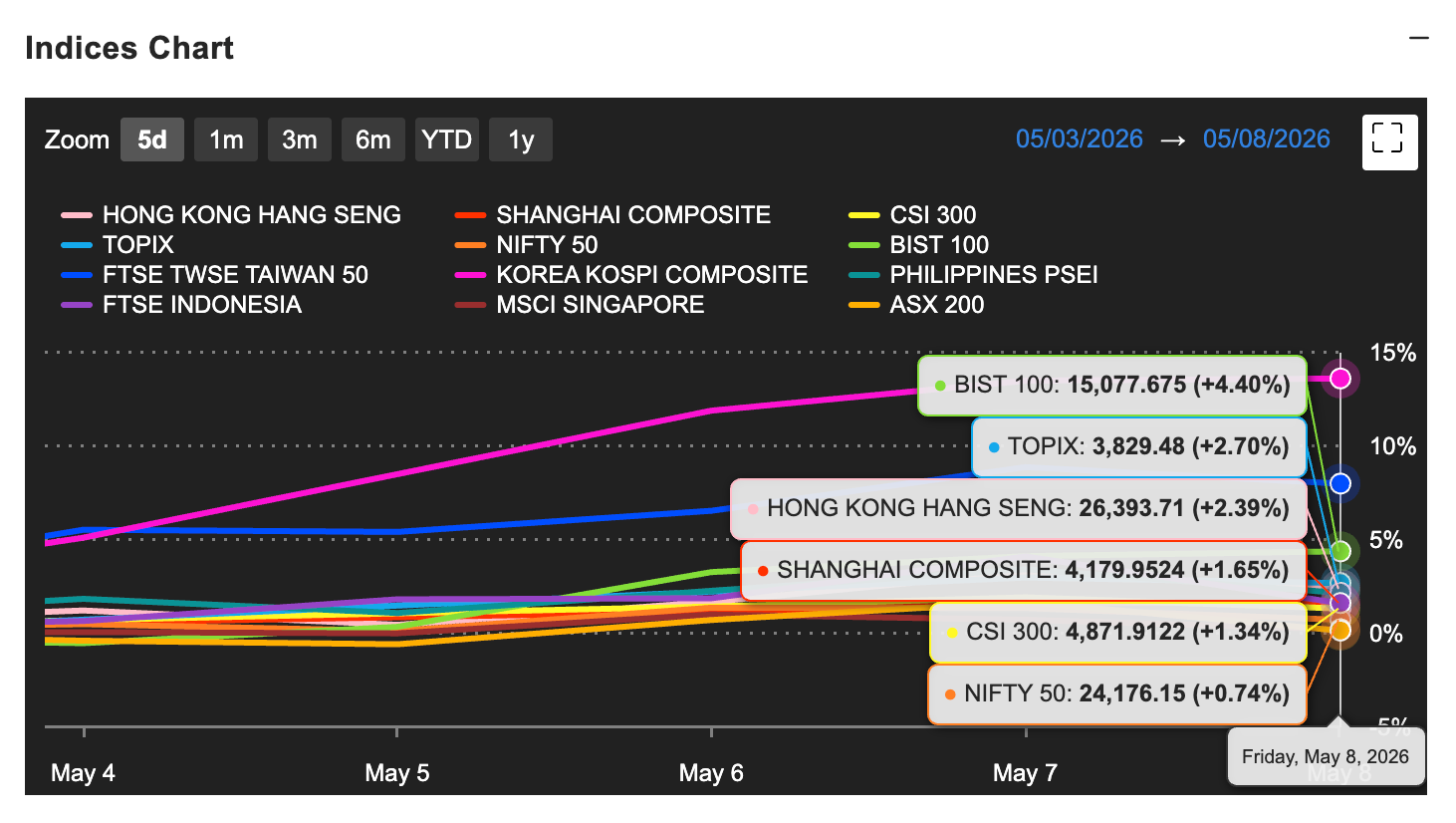

A week where the macro data did the talking, and the property tape did the answering. April exports printed +14.1% YoY against +7.9% consensus and +2.5% prior, the largest single positive surprise on the China data calendar in over a year, with imports +25.3%, the trade balance at $84.8bn, China’s RatingDog Composite PMI at 53.1, and Hong Kong’s Q1 GDP at +5.9% YoY versus a 3.5% forecast. Inside that backdrop, Hong Kong’s tape was led by HSI Property +7.56% and HSI Mainland Properties +13.36%, with China Overseas +19.88%, Longfor +14.09% and China Res Land +13.11% all printing the kind of single-name moves that suggest the Tier-1 property turnaround thesis got repriced from “stabilisation” to “turnaround” in five trading days. PetroChina -11.97% and CNOOC -10.01% funded the move, with Brent -6.6% on US-Iran ceasefire holding. Kuaishou +23.43% and Baidu +22.33% led the internet/AI software complex on the back of the Kunlunxin US$14.7bn HK IPO news, the DeepSeek-Huawei stack confirmation, and ongoing $45bn fundraise / V4.1-in-June chatter. China onshore +1.34% (CSI 300) and HSI +2.39% were the broad-index outcomes; the more interesting reads are at the sector level. MXAPJ +6.8% on the week, with Korea +16.9% and Taiwan +7.9% the regional leaders.

IMPORTANT NOTE: We are presently in the process of getting a license with a major regulator, and while that process is ongoing we are not able to publish the portfolio update and company notes. We’ll do a big reveal of the new plans as soon as we’re in a position to do thusly. We apologise for it taking time, but this is unfortunately a fact of life. With that we’re also putting the opinion part of this behind the wall.

NOTE: Panda+ is now closed to new joiners. We thank everyone for their interest and custom.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

📊 Weekly Relative Performance Observations

Week of 4 - 10 May 2026

📉 Broad Takeaway

A clean risk-on week. MXAPJ closed +6.8% on the week, with Korea +16.9%, Taiwan +7.9% and Hong Kong +3.4% leading, while Singapore +0.2%, Australia +0.3% and Thailand +0.5% lagged. EM Asia saw US$1.4bn of foreign inflows on net, with Taiwan attracting +US$5.5bn on the AI/memory bid and Korea posting -US$3.6bn of outflows even as the index ripped 17%, which tells you domestic and HF money were the marginal buyer there. Tech Hardware & Semis (+13.9%), Capital Goods (+5.5%) and AIGC Semiconductors (+13.2%) led at the sector level. Energy (-4.5%) lagged, alongside Consumer Staples (+0.3%), Health Care (+0.5%) and Utilities (+0.7%).

China participated, but participated quietly. CSI 300 +1.3% and MSCI China +3.2% in USD terms, both well behind the Korea/Taiwan move. Hong Kong outperformed onshore (HSI roughly tracking MSCI HK +3.4%). The shape underneath the headline: the chip and AI-infrastructure leg of the tape kept running on Cambricon’s continuing re-rating and DeepSeek-Huawei stack confirmation, but defensives, energy and the commodity-cyclicals all sold off on the Brent move. The export print landed Saturday morning so the cleaner read on the trade beat will be next week’s tape, but the run-up into the print was already telling: A-share trade-exposed names, freight, and onshore industrials all caught a bid through the week.

The macro backdrop deserves more space than usual. April exports +14.1% YoY versus 7.9% consensus and 2.5% prior; April imports +25.3% versus 15.2% consensus and 27.8% prior; trade balance $84.82bn versus $51.13bn last month and $79.1bn forecast. HK Q1 GDP +5.9% YoY versus 3.5% consensus, +2.9% QoQ versus 1.4% forecast. RatingDog Services PMI 52.6 (consensus 52.0), RatingDog Composite 53.1 (prior 51.5), saving the print after last week’s NBS Services 49.4. The data set is not perfectly clean: HK April S&P Global PMI fell to 48.6 from 49.3 (the local-tape weakness is real even as the macro headline is strong), and HK March retail sales +9.8% printed against a 17.5% prior base that flattered the comp. But the direction is unambiguous, and so is the policy posture: targeted, no bazooka required.

MXCN/CSI 300 split was +3.2%/+1.3% on the week, the inverse of last week. In factor terms: High Capex (+10.0%), GARP (+7.0%), Strong Earnings Revision (+7.0%) and Generative AI (+8.1%) led the AEJ basket; Defensives (+0.7%) and Secure Dividend Yield (+1.6%) lagged. China Offshore VIP basket +8.2%, China A VIP +4.2%. The 12m forward MXAPJ index target was raised to 990 from 920 by one major index strategist, alongside a Korea KOSPI target of 9,000 and 2026E earnings growth forecasts of +300% for Korea (memory) and +45% for Taiwan (AI hardware). The frame for China inside that picture is “OW Japan, Korea, China Offshore and China A; MW Taiwan, Singapore, Hong Kong, Malaysia, India; UW Australia, Thailand, Indonesia, Philippines.”