China Weekly Wrap (feat. BABA Results and America First Investment Policy)

a week that was 17 February - 21 February 2025

Good Afternoon,

Parts of the China market are still rallying, while others take a moment to catch their breath. The landscape is intriguing and makes market monitoring highly rewarding. When you add evolving macroeconomic trends and blend them with impressive, insightful corporate results, you get a compelling mix that’s a pleasure to analyse.

We’ll talk about the Alibaba results in the corporate news section, (and a few other ones too!), the America First Investment Policy in the News section (which is a phenomenal document in its own right), but before we do, I wanted to re-highlight the BABA 0.00%↑ note we wrote this week. ITs over 7k words long yet we really tried to keep every portion of it succinct. Its a pretty comprehensive overview of BABA’s business, so if you are at all interested in it, I encourage you to have a read:

Link to the pice is here: Link

We have also finally written an introduction to the substack, which was along time coming, but 100 entires in, it was time to pull the trigger. If tou are interested in it, you can find that piece here.

This coming week we’ll publish 2 research pieces: Baidu and TenCent. Baidu piece is almost done, but BABA taking so long bumped it down the schedule. Thankfully it’s much smaller footprint to deal with so we should be able to publish on Monday, and follow up with Tencent in the latter part of the week. We shall also endeavour to publish the 2 sessions preview also later on in the week to include the outcomes of the NPC SC meeting that is being held 24-25 of February.

On top pf that, but really as usual. this Sunday, we’re back with our weekly portfolio review, and the Panda companies have once again delivered impressive results both in absolute and relative terms. The focus will also be on BABA and a role it can play in the portfolio. This exclusive update is available only to premium subscribers, so join us to unlock key insights and join the conversation.

So a lot to look forward to on the deck for us, so do join us if you are interested. Also a reminder to check out our portfolio services if you have an asian portfolio (or a part of the portfolio) that you would like to be sure is set up appropriately for 2025.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

As of February 21, 2025 close of business, here’s a summary of the weekly, month-to-date (MTD), and year-to-date (YTD) performances of major Chinese and Hong Kong stock indices that we follow.

Notes:

Shanghai Composite Index (SHCOMP): Tracks all stocks (A and B shares) traded on the Shanghai Stock Exchange.

CSI 300 Index (SHSZ300): Represents the top 300 stocks traded on the Shanghai and Shenzhen Stock Exchanges.

China A50 Index (512150 CH): Comprises the top 50 A-share companies listed on the Shanghai and Shenzhen Stock Exchanges.

ChiNext Price Index (159954 CH): Focuses on innovative and high-growth enterprises listed on the Shenzhen Stock Exchange.

SSE STAR 50 Index (83151 HK): Represents the top 50 companies listed on the Shanghai Stock Exchange’s STAR Market, emphasising science and technology innovation.

Hang Seng Index (HSI): Measures the performance of the largest companies listed on the Hong Kong Stock Exchange.

Hang Seng China Enterprises Index (2828 HK): Includes major H-share companies listed in Hong Kong.

Currency Considerations:

Chinese Indices (SSEC, CSI300, China A50, CNT, STAR50): These indices are denominated in Chinese Yuan (CNY). To present their performance in USD terms, currency exchange rate fluctuations between the CNY and USD have been considered.

Hong Kong Indices (HSI, HSCEI): Denominated in Hong Kong Dollars (HKD). Their performance in USD terms reflects the HKD/USD exchange rate stability, as the HKD is pegged to the USD.

Weekly Relative Performance Observations:

From the perspective of a Chinese equities investor, this was another constructive week, characterized by rising optimism and selective buying in growth-oriented sectors. Most Chinese indices outperformed their regional counterparts, reflecting a combination of policy support signals and improving corporate earnings trends. Below is a detailed breakdown, incorporating some broader context to help frame the moves:

Strong Performance in Chinese Equities

MSCI China Index (+3.85%)

Highlights: Led regional peers, continuing a rebound that began earlier in the month. Renewed risk appetite for Chinese technology and consumer discretionary stocks underpinned gains.

Context: Investors appear more confident about near-term policy support—such as potential monetary easing and targeted stimulus measures—particularly in innovation and tech.

Shenzhen Index (+1.96%)

Highlights: Continued strength in technology and innovation-driven names. High-growth companies in semiconductors and AI-related segments attracted capital inflows.

Context: Domestic investors remain upbeat on the government’s push for technological self-reliance, which benefits Shenzhen-listed firms.

Shanghai A Shares (+1.69%)

Highlights: Posted moderate gains, with financials and select consumer stocks contributing.

Context: While sentiment is improving, investors are somewhat selective, favoring quality names that demonstrate strong balance sheets or policy alignment.

Hong Kong Hang Seng Index (+3.2% to +3.7% range)

Highlights: Offshore-listed Chinese stocks rallied, echoing mainland momentum. Financials, property, and tech outperformed, buoyed by improved investor sentiment.

Context: Valuations for many Hong Kong–listed Chinese companies remain relatively attractive, driving renewed inflows from global funds.

Regional Peers’ Performance

Japan’s Nikkei 225 (+0.82% to +1.09%) and TOPIX (+0.65% to +1.06%)

Highlights: Posted modest gains, with a more measured advance compared to China.

Context: Japanese equities have been consolidating after strong performance in prior weeks. Investor focus remains on corporate governance reforms and earnings season updates.

FTSE TWSE Taiwan 50 (+0.57%)

Highlights: Managed a small gain, trailing Chinese indices but remaining in positive territory.

Context: While the tech-heavy Taiwanese market often correlates with Chinese tech trends, it lagged slightly, reflecting cautious positioning ahead of semiconductor demand updates.

USD/CNH (-0.14% depreciation)

Highlights: Slight currency fluctuation did not significantly impact equity inflows, indicating foreign investors remain comfortable with current exchange rate trends.

Context: A relatively stable yuan can help sustain foreign buying interest, particularly if U.S. dollar strength remains contained.

Key Takeaways for Chinese Markets

Broad-Based Rally, Tech in Focus: Both onshore and offshore Chinese equities gained, but the outperformance was most pronounced in tech, consumer discretionary, and policy-supported sectors.

Hong Kong’s Upswing: The Hang Seng and related ETFs posted solid gains, reflecting renewed global investor interest in offshore Chinese listings, potentially spurred by attractive valuations.

Selective Onshore Rebound: While A-shares moved higher, certain sub-sectors—especially traditional industrials—underperformed. Investors appear to be rotating toward future-oriented growth plays.

Regional Divergence Continues: China stands out with a stronger rebound compared to Japan, Taiwan, and some other Asian peers. This divergence suggests global funds are warming again to Chinese equities after a period of caution.

Policy and Earnings Tailwinds: Anticipation of supportive government measures and better-than-expected corporate earnings in select sectors continue to fuel buying interest.

In the news this week:

President Xi to Chair Business Leaders Symposium

Announced by: Chinese Government

Date: 14 February 2025

Details: President Xi Jinping will host a high-profile symposium bringing together leading figures from major private enterprises—among them Alibaba’s Jack Ma, Tencent’s Pony Ma, Xiaomi’s Lei Jun, and Unitree Robotics executives. The meeting, slated for next week, aims to discuss macroeconomic policies, strategies to address industry-specific challenges, and possible government measures to support corporate expansion.

Such high-level engagements often signal Beijing’s intention to shore up private-sector confidence and clarify policy directions. The inclusion of prominent tech CEOs suggests that innovation and technology development will remain a core focus of future policy initiatives. We now expect potential policy announcements or incentives to stimulate private investment and boost domestic consumption. For a fuller take check out our podcast from earlier in the week.

China Unveils Action Plan to Stabilise Foreign Investment

Announced by: State Council of the People’s Republic of China

Date: 18 February 2025

Details: The State Council released a wide-ranging initiative to streamline foreign investment approvals, expand market access in sectors like telecom, healthcare, and education, and enhance IP protection. The plan also addresses bureaucratic hurdles, aiming to attract more global capital despite external uncertainties.

This Indicates Beijing’s intent to maintain China’s attractiveness as a premier investment destination. Foreign companies in high-value sectors, such as biopharma, stand to benefit from looser restrictions and potentially faster regulatory approvals. It could help offset investor concerns about geopolitical risks by demonstrating China’s commitment to an open market.

China to Expand Pilot Foreign Investment in Manufacturing Sector

Announced by: National Development and Reform Commission (NDRC)

Date: 19 February 2025

Details: The NDRC will broaden existing pilot programs designed to allow deeper foreign participation in high-tech and advanced manufacturing. Emphasis will be placed on robotics, semiconductors, and AI-driven applications, aligning with China’s ambition to lead in next-generation technologies.

This aims to spur industrial upgrading and foster innovation by attracting overseas capital and expertise.vCompanies with niche tech capabilities may find it easier to form joint ventures or wholly foreign-owned enterprises in pilot zones.

It also signals a potential relaxation of previous constraints in strategic manufacturing areas.

China’s Premier Li Qiang: Economic Policies to Focus on Improving Livelihoods

Announced by: State Media (Xinhua News Agency)

Date: 20 February 2025

Details: Premier Li Qiang reiterated the government’s commitment to boosting domestic consumption and upgrading social services in education, healthcare, tourism, and elderly care. Specific measures could include consumer vouchers, infrastructure spending, and tax incentives for targeted industries.

We are paying attention to this as this continues to highlight the pivot toward a more consumption-driven growth model. WE are keeping tabs as it may offer new investment opportunities in consumer-facing sectors and public services, and even at this point it certainly reinforces the notion that social stability and quality of life improvements remain top priorities for Beijing.

China to Improve Recycling System of New Energy and Auto Power Batteries

Announced by: Chinese Cabinet (State Council)

Date: 20 February 2025

Details:

The State Council approved measures to refine the recycling and disposal process for aging EV and renewable energy batteries. This includes setting standards for collection, transportation, and reuse of valuable materials.

This development reflects China’s growing emphasis on environmental sustainability and circular economy principles which could create opportunities for foreign and domestic firms specialising in battery recycling technology, including BYD and CATL.

China Commerce Minister: Calls for Dialogue with US, Criticises Unilateral Tariffs

Date: 17–18 February 2025

Details: Over two days of statements, the Chinese Commerce Minister underscored Beijing’s readiness to engage in constructive dialogue with the United States to ease ongoing trade tensions. While expressing willingness to negotiate, the Minister also criticized U.S. tariffs as undermining normal economic and trade cooperation, voicing “strong dissatisfaction” at what China views as protectionist measures. These dual messages highlight both Beijing’s openness to negotiation and its determination to defend its interests.

‘America First Investment Policy’ Released

Announced by: The White House

Date: 21 February 2025

Details: The U.S. administration formally introduced its “America First Investment Policy,” which encourages inbound investments from allies while restricting or blocking capital flows from “foreign adversaries,” most notably the PRC. It also promises expedited environmental reviews for large investments and tighter scrutiny of technology transfers.

The two final news points actually highlight the same issue. For decades, the United States and China have been locked in a symbiotic economic relationship defined by persistent imbalances: the U.S. consumes vast quantities of goods from China, while China recycles its trade surpluses into U.S. Treasuries. This dynamic allows American consumers to enjoy cheaper imports, while Chinese manufacturers expand on the strength of external demand—without a correspondingly large role for Chinese domestic consumption. Now, however, both countries appear to be reaching the limits of this arrangement.

The America First Investment Policy exemplifies this shift. By tightening scrutiny of foreign investments—particularly from China—in sensitive sectors and prioritizing self-sufficiency, Washington is laying the groundwork for a departure from the “import goods, export Treasuries” cycle. Although the policy is framed as a national security measure, it also addresses concerns about overreliance on global supply chains that funnel critical technologies and resources from China to the U.S.

Meanwhile, China’s Commerce Minister has issued a dual message: calling for dialogue to resolve trade tensions and criticizing U.S. tariffs as protectionist. This two-pronged approach underscores Beijing’s recognition that it needs a stable external environment, even as it shifts toward a more balanced economic model. Recent announcements to stabilize foreign investment, encourage domestic consumption, and upgrade industries reflect a broader effort to foster self-sufficiency in key sectors while gradually boosting the role of the Chinese consumer.

Such changes are necessary because the current imbalances are no longer sustainable. If the U.S. continues to rely heavily on imports without strengthening its own manufacturing base, its fiscal and trade deficits will keep growing. Conversely, if China remains dependent on export-led growth, it underutilizes its domestic market potential and stays vulnerable to external demand fluctuations. At the same time, rising geopolitical tensions are pushing both sides toward “decoupling,” where each seeks to localize production of strategically important goods.

In the long term, we should expect a gradual decrease in U.S.-China trade, particularly in strategic or politically sensitive sectors. The U.S. will likely onshore more manufacturing, while China invests in its own high-tech industries and fosters domestic consumption. For investors, Chinese financial assets could benefit from a policy tailwind as Beijing develops a consumer-driven economy. Neither country can overhaul decades of entrenched economic patterns overnight, but these recent policy moves—ranging from the U.S.’s “America First” framework to China’s efforts to attract foreign investment and encourage internal demand—are paving the way toward greater self-sufficiency on both sides.

Ultimately, the statements from China’s Commerce Minister and the “America First Investment Policy” reveal that both countries are acknowledging the limits of the old model. They are forging policies that reduce mutual dependency and prioritize domestic growth engines. While these shifts will not resolve imbalances immediately, they set the stage for a future in which the U.S. manufactures more at home and Chinese consumers play a more prominent role in global demand—fundamentally reshaping trade, investment, and growth patterns in the process.

Data Released This Week:

Industrial Production (YoY) – January 2025

Announced by: National Bureau of Statistics (NBS)

Date: 17 February 2025

Event: January 2025 Industrial Production (Year-over-Year)

Details:

Industrial production grew by 4.6% in January compared to the same period last year. This uptick reflects resilient manufacturing output, particularly in high-tech and machinery segments, despite global demand uncertainties. Government policy support and stable energy supply contributed to the sector’s steady performance.

Retail Sales (YoY) – January 2025

Announced by: National Bureau of Statistics (NBS)

Date: 18 February 2025

Event: January 2025 Retail Sales (Year-over-Year)

Details: Retail sales rose by 5.9% in January, suggesting improving consumer sentiment. Growth was driven by strong holiday spending on consumer electronics, clothing, and dining-out services. E-commerce platforms also saw notable gains, indicating continued momentum in online consumption channels.

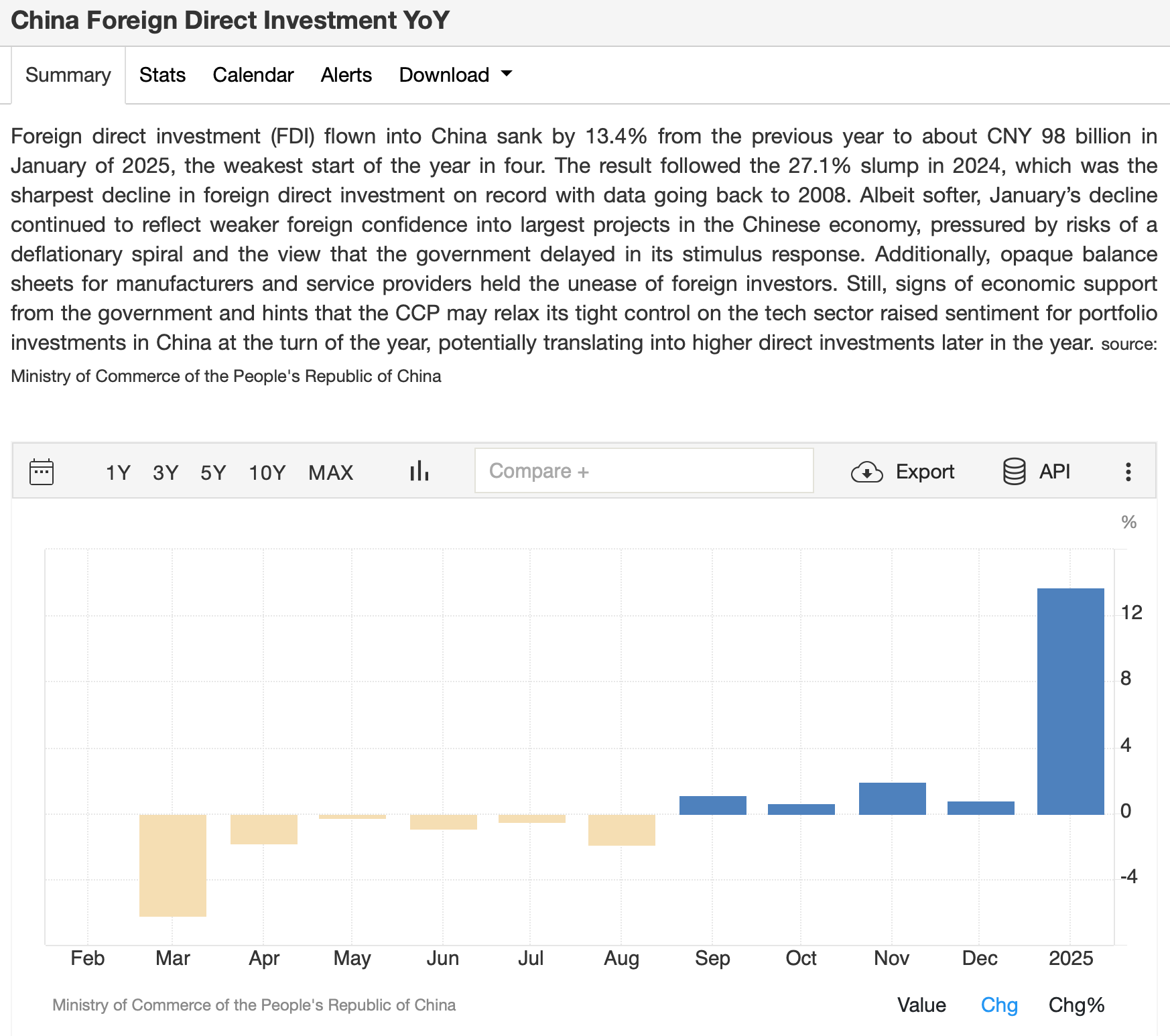

Foreign Direct Investment (FDI) – January 2025

Announced by: Ministry of Commerce (MOFCOM)

Date: 19 February 2025

Event: January 2025 FDI Data

Details: FDI inflows increased by 8.3% year-on-year, led by investments in advanced manufacturing, technology, and biopharmaceuticals. The recent “Action Plan to Stabilize Foreign Investment” was cited as a contributing factor, helping streamline approvals and boost investor confidence.

SSE and SZSE Exceed 2 Trillion Yuan Turnover

Announced by: Shanghai Stock Exchange (SSE) & Shenzhen Stock Exchange (SZSE)

Date: 21 February 2025

Event: Combined Turnover Surpasses 2 Trillion Yuan

Details: For the first time in two months, combined turnover on the SSE and SZSE surpassed 2 trillion yuan, rising by more than 400 billion yuan compared to the previous trading session. This reflects robust market activity fueled by optimism around policy support and solid corporate earnings. The uptick in volume underscores renewed investor confidence in Chinese equities, especially in technology and consumer sectors.

Complete Index Performance List:

General Trends

Chinese equity markets delivered moderate but broad-based gains this week, reflecting improving investor confidence and continued optimism around policy support. On the mainland, the Shanghai Composite Index (SSE) rose +0.85% to 3,379.11, buoyed by renewed interest in industrial and growth-oriented stocks. The SSE-SZSE 300 Index, which tracks large-cap A-shares, climbed +0.93% to 3,978.94, indicating steady demand for leading blue-chip companies.

Shenzhen’s tech-heavy boards fared even better. The CHINEXT Index jumped +2.74% to 2,827.71, fueled by strong performances in AI, biotech, and advanced manufacturing. The Shenzhen 100 Index gained +1.59% to 4,827.71, underpinned by robust buying in innovation-driven companies.

In Hong Kong, the Hang Seng Index (HSI) advanced +1.64% to 18,952.30, while the HS TECH Index added +2.63%, reflecting growing optimism toward China’s technology giants and a potential easing of previous regulatory headwinds. Overall, the week’s gains suggest that Chinese equities are finding a firmer footing, supported by stable macro data, ongoing policy measures, and a “risk-on” tilt among investors.

Relative Outperformance

CHINEXT Index (+2.74%): The CHINEXT, a benchmark for growth-oriented small and mid-cap companies, led mainland gains this week. Continued investor enthusiasm for tech, biotech, and AI-related plays drove the rally. The index also benefited from supportive government rhetoric on innovation and advanced industries.

SSE-SZSE 300 Index (+0.93%): Large-cap A-shares saw a solid advance, signaling that institutional investors remain constructive on key state-backed enterprises and financials. Although overshadowed by higher gains in smaller-cap segments, the SSE-SZSE 300’s performance underscores steady capital flows into blue-chip stocks.

HS TECH Index (+2.63%): Technology stocks in Hong Kong continued to rebound, reflecting improving sentiment toward major Chinese internet and tech firms. Expectations of policy support, alongside signs of stabilizing regulatory conditions, fueled buying in names exposed to AI, e-commerce, and fintech.

Shenzhen 100 Index (+1.59%): Shenzhen’s large-cap innovators maintained their upward momentum. Sectors such as new energy, semiconductors, and advanced manufacturing were among the key drivers, mirroring the government’s push toward high-tech self-reliance.

Sector-Specific Dynamics

Technology & Innovation: Growth and tech-heavy indices outperformed again, supported by China’s strategic focus on AI, advanced manufacturing, and biotech. Investor appetite was particularly strong in Shenzhen-listed firms, reflecting confidence in long-term government support.

Commodity and Industrial Equities: The SSE Commodity Equity Index slipped -0.40%, suggesting some profit-taking in resource-linked names. Nevertheless, industrials overall held up, bolstered by expectations of targeted fiscal measures aimed at sustaining manufacturing growth.

Financials & Real Estate: Financial stocks in Hong Kong saw moderate gains, helped by easing concerns over bad debts and improving loan growth in mainland markets. Real estate shares benefited from incremental policy measures aimed at stabilizing the property sector, though gains remained relatively modest compared to tech.

Large-Cap vs. Small-Cap Performance

Large-Cap Indices: The SSE-SZSE 300 (+0.93%) and SSE Mega Cap Index (not shown in the screenshot, but typically moves in line with other large-cap benchmarks) recorded steady gains, reflecting institutional confidence in market stalwarts.

Small-Cap & Innovation-Focused Indices: Indices like CHINEXT (+2.74%) and SSE SME Innovation (+1.58%) outperformed, underscoring the market’s appetite for higher-growth segments. Government incentives for SMEs and R&D-intensive industries continue to attract investors seeking above-average returns.

Additional Observations

Hong Kong’s Continued Recovery

The HSI’s +1.64% climb builds on prior weeks’ momentum, with tech and consumer plays driving much of the gains. Turnover remains healthy, indicating a sustained “risk-on” mood.

Elevated Trading Volumes

As noted in previous updates, the combined turnover on Shanghai and Shenzhen exceeded 2 trillion yuan for the first time in two months, a sign of robust market participation and growing investor conviction.

Divergence in Defensive Plays

While technology and growth stocks attracted capital, defensive sectors like utilities and high-dividend plays lagged, reflecting a shift toward riskier, higher-growth assets.

Key Takeaways

Improving Market Sentiment: Broad-based gains across Shanghai, Shenzhen, and Hong Kong point to renewed confidence in China’s economic outlook, bolstered by steady macro data and supportive policy signals.

Tech & Innovation in the Spotlight: Growth-oriented sectors, especially AI, semiconductors, and biotech, continue to see strong inflows, aligning with China’s strategic push for self-reliance and next-generation development.

Selective Strength in Commodities & Industrials: Commodity-linked stocks faced mild headwinds, while advanced manufacturing and industrials benefited from expectations of targeted stimulus and robust domestic demand.

Small-Cap & SME Outperformance: Indices tracking small and medium-sized enterprises outpaced their large-cap counterparts, highlighting investor preference for high-growth opportunities and policy-backed innovation.

Hong Kong’s Resilience: The HSI and HS TECH Index posted notable gains, confirming a continued rebound in offshore-listed Chinese equities as regulatory fears ease and global investors seek value in battered tech names.

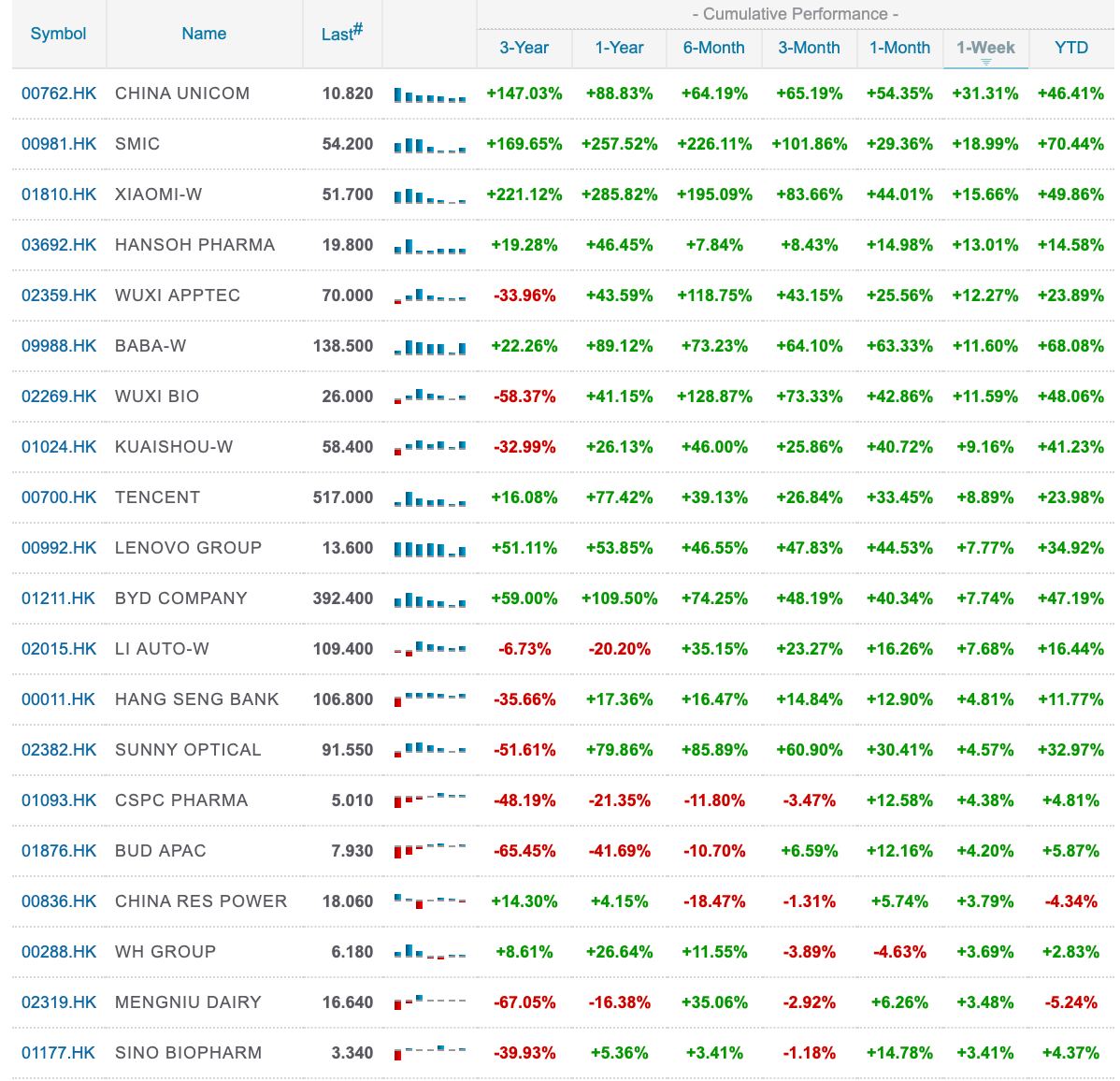

Top 20 Index Constituents:

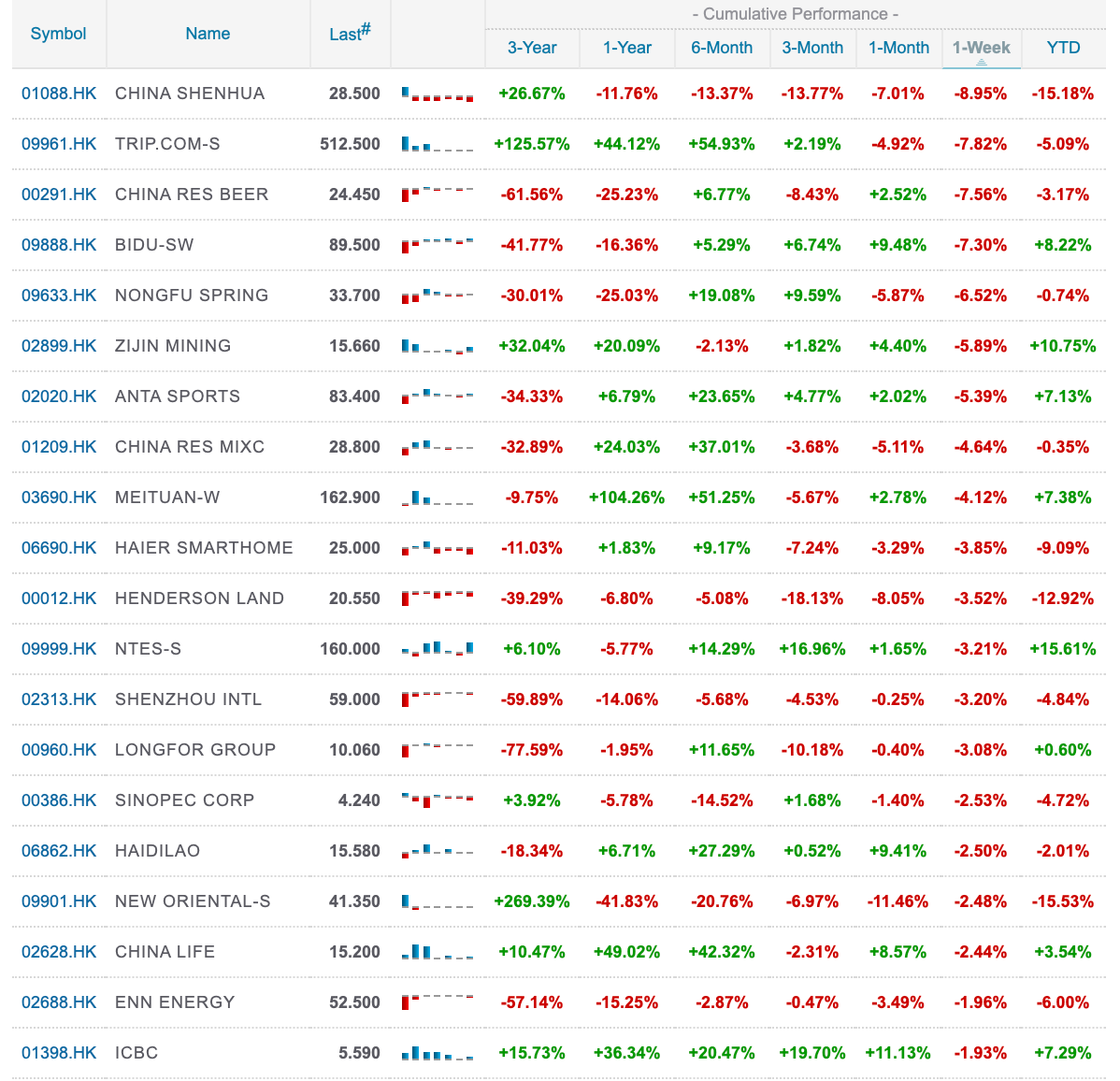

Bottom 20 Index Constituents:

Corporate News and Results this week:

(News first, results last with Alibaba is last on the list to allow for a longer discussion)

BYD EV Production Update

Announced by: BYD Company Limited

Date: 21 February 2025

Event: Monthly Electric Vehicle Production & Sales Data

Details: BYD reported that January EV sales rose 25% year-on-year, underlining robust domestic demand for new energy vehicles. The company also highlighted progress in battery supply partnerships, reinforcing its leadership position in the EV battery market.

Xiaomi New Product Launch

Announced by: Xiaomi Corporation

Date: 20 February 2025

Event: Launch of Flagship Smartphone and AIoT Devices

Details: Xiaomi unveiled its latest flagship smartphone featuring a custom AI chip, alongside new AIoT (Artificial Intelligence of Things) home products. The company emphasised global expansion plans and deeper AI integration across its hardware ecosystem.

Pinduoduo Q4 2024 Earnings

Announced by: Pinduoduo Inc.

Date: 21 February 2025

Event: Fourth Quarter 2024 Financial Results

Details: Pinduoduo posted a 14% year-on-year increase in revenue, driven by strong demand for agricultural produce and fast-moving consumer goods. Management signalled plans to expand its livestreaming features to enhance user engagement and better compete with other e-commerce platforms. Overall taken Positively by the market +5.8% for the week.

JD.com Q4 2024 Results

Announced by: JD.com Inc.

Date: 20 February 2025

Event: Fourth Quarter 2024 Earnings Release

Details: JD.com achieved 10% year-on-year revenue growth, buoyed by demand in consumer electronics and home appliances. The company underscored its investments in logistics, including drone and autonomous delivery expansion, and partnerships with local governments to boost rural e-commerce. Stock ended the week +2.5%, a little behind the Tech indices.

Tencent Q4 2024 Earnings

Announced by: Tencent Holdings

Date: 19 February 2025

Event: Fourth Quarter 2024 Financial Results

Details: Tencent posted an 8% year-on-year revenue increase, propelled by its gaming division and cloud services. The company also reported growth in fintech solutions (WeChat Pay, wealth management) and outlined expanded investments in metaverse-related technologies. Market took the results positively ending +8.9% on the week.

Kuaishou Q4 2024 Earnings

Announced by: Kuaishou Technology

Date: 19 February 2025

Event: Fourth Quarter 2024 Earnings Release

Details: Kuaishou reported a 15% year-on-year revenue increase, driven by strong live-streaming and social commerce growth. Monthly active users (MAUs) surpassed 600 million for the first time. The company plans to invest further in AI-driven content recommendations and new monetisation features. Another positive reaction as the stock was up 9.2% on the week.

Baidu Q4 2024 Earnings

Announced by: Baidu Inc.

Date: 17 February 2025

Event: Fourth Quarter 2024 Earnings Release

Details: Baidu reported a 9% year-on-year increase in total revenue, driven by its AI cloud services and a continued recovery in online advertising. The company highlighted strong traction in autonomous driving partnerships and AI-enabled enterprise solutions. Management reiterated its focus on generative AI research, hinting at upcoming product rollouts. The market was not impressed though, as between the Deep Seek integration and the absence at the Tech Leaders meeting, the stock was down 6%, despite positive sectoral tailwinds. We’ll be discussing Baidu in some detail this coming week.

Alibaba Q3 FY2025 Results

Announced by: Alibaba Group

Date: 18 February 2025

Event: Third Quarter FY2025 Financial Results (covering October–December 2024)

Details: Alibaba reported better-than-expected earnings for Q3 FY2025, showcasing solid revenue and profit growth across several core segments, while also demonstrating a continued focus on AI-driven strategies and streamlined operations.

Headline Figures

Adjusted EPS: ¥21.39 (vs. est. ¥19.12), up +13% YoY

Revenue: ¥280.15B (vs. est. ¥277.37B), up +8% YoY

Adjusted EBITDA: ¥62.05B (vs. est. ¥60.42B), up +4% YoY

Segment Highlights

Cloud Intelligence Group

Revenue: ¥31.74B, up +13% YoY (est. ¥30.68B)

Adj. EBITA: ¥3.14B, up +33% YoY

Taobao and Tmall Group

Revenue: ¥136.09B, up +5% YoY

Customer Management Revenue: ¥100.79B, up +9% YoY

Direct Sales & Others: ¥28.73B, down -9% YoY

Adj. EBITA: ¥61.08B, up +2% YoY

Alibaba International Digital Commerce Group

Revenue: ¥37.76B, up +32% YoY

International Commerce Retail: ¥31.55B, up +36% YoY

International Commerce Wholesale: ¥6.20B, up +18% YoY

Adj. EBITA: (¥4.95B) loss; widened by -57% YoY

Cainiao Smart Logistics

Revenue: ¥28.24B, down -1% YoY

Adj. EBITA: ¥235M, down -76% YoY

Local Services Group

Revenue: ¥16.99B, up +12% YoY

Adj. EBITA: (¥596M) loss; narrowed by +71% YoY

Digital Media & Entertainment Group

Revenue: ¥5.44B, up +8% YoY

Adj. EBITA: (¥309M) loss; narrowed by +40% YoY

All Others Segment

Revenue: ¥53.10B, up +13% YoY

Adj. EBITA: (¥3.16B) loss; stable YoY

Other Key Metrics

Net Income: ¥46.43B, up +333% YoY

Non-GAAP Net Income: ¥51.07B, up +6% YoY

Income from Operations: ¥41.21B, up +83% YoY

Operating Margin: 15% (vs. 9% YoY)

Free Cash Flow: ¥39.02B, down -31% YoY

Net Cash from Ops: ¥70.92B, up +10% YoY

Strategic & Shareholder Updates

Repurchased 15M ADSs (~¥1.3B) during the quarter, reducing total outstanding ADSs by 0.6%.

Completed a ~¥5B senior unsecured notes offering to extend debt maturities.

Disposed of Sun Art and Intime stakes for ~¥19.7B, streamlining non-core assets.

Management Commentary

CEO Eddie Wu: “This quarter’s results demonstrated substantial progress in our ‘user first, AI-driven’ strategies and the re-accelerated growth of our core businesses. Cloud revenue reignited with double-digit growth, driven by AI-related products achieving triple-digit growth for the sixth consecutive quarter.”

CFO Toby Xu: “We maintained financial discipline while investing in our core businesses, achieving positive EBITA growth in Taobao and Tmall Group. We also strengthened our balance sheet through asset sales and share buybacks, enhancing long-term shareholder value.”

After a challenging period marked by heightened regulatory scrutiny and strategic realignments, Alibaba appears to have turned a significant corner. Recent earnings results underscore the company’s renewed momentum, highlighted by better-than-expected revenue growth and a strategic pivot toward AI-powered services. Rather than merely recovering from external pressures, Alibaba is emerging as a global leader poised to capitalize on cutting-edge innovations and a reinvigorated product suite that resonates more strongly with its core markets.

One of the standout factors behind this resurgence is Alibaba’s focus on artificial intelligence. The Cloud Intelligence Group’s double-digit revenue growth and ambitious product rollouts in AI-related offerings illustrate the company’s commitment to remaining at the forefront of tech innovation. This aligns seamlessly with global market trends, as AI is increasingly seen as a key driver of future profitability in e-commerce, cloud computing, and digital services. Beyond AI, Alibaba’s traditional commerce segments are also showing improved traction, thanks to more targeted offerings, a clearer organizational structure, and continued efforts to streamline operations.

The market’s response has been notably positive, with Alibaba’s stock surging 15% this week alone. While such a rapid ascent may prompt some caution about near-term fluctuations, our analysis indicates that the company’s underlying fundamentals support a higher long-term valuation. In our view, the “new Alibaba” is less about managing crises and more about proactive growth—extending its global footprint, nurturing its cloud ecosystem, and investing heavily in future-focused technologies like AI and advanced logistics.

Of course, no tech giant operates on a perfectly linear growth trajectory, and Alibaba is no exception. Regulatory environments can shift, and competitive landscapes evolve. Yet, given the company’s track record of navigating challenges and adapting to market needs, we see ample reason for optimism. In short, our assessment of Alibaba as a business has markedly improved, driven by its capacity to innovate, its robust suite of services, and its renewed ambition to capture global market opportunities.

The market closed badly in the US, and there are various rumours circulating around the market about the size of the fiscal package. We are also going to start seeing what the NPC SC will be guiding for. We’ll discuss that at the end of next week. Not a ton of data next week otherwise, but brace for major moves.

HAve a great week ahead,

Leonid

Any specific theme behind the Star50’s outsized 8% move that you can see or was it more of a broad catchup with the other tech indices?