China Weekly Wrap (feat. Politburo meeting wrap)

a week that was 24 February - 28 February 2025

Good morning!

What a week. Mettle was tested quite severely this week in quite a few ways, but we’ve come out the other end more or less unscathed, and sufficiently energised to summarise the purely financial part of it. We’ll touch on the results that were published this week as well as some major pieces of political developments like the NPC SC meeting and the politburo session. Net-net though it's been a tough week given the severity of the moves in both directions across the asian region - first a rip up and then a big move down. We don’t believe that this move is symptomatic of a change in the market - quite the contrary, its an opportunity to test out our core thesis - the Chinese market will be moved by local developments a lot more than the changes in the US.

Sure it generates headlines but the direction ultimately comes from the confidence improvement of domestic investors, fuelled by a more aggressive policy stance of the CCP and a general economic improvement. We’ll have a lot more of that this coming week with the National Peoples Congress. A full preview will be up on the website early next week.

With that in mind we have continued to explore the China Internet space. WE have looked at

Do check those out if you haven’t yet. We found the exercise to be very interesting and ultimately rewarding as we readjust our preference scale in the space. This week we’re coving JD.com and PinDuoDuo - should be an exciting set of write ups. We’d know - we’re writing them!

Much like the work from the previous week, the reports will be behind the paywall. If you are interested in them do consider joining.

For our premium subscribers we will also be sending around the Panda Portfolio Review tomorrow detailing how we fared in this market, as well as any moves we’re priming for ahead of the NPC.

This is also the last call for the premium subscribers to request the Panda Perspectives pre-NPC economic outlook presentation. IF you are interested, do please respond to this email or drop us a DM saying so.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

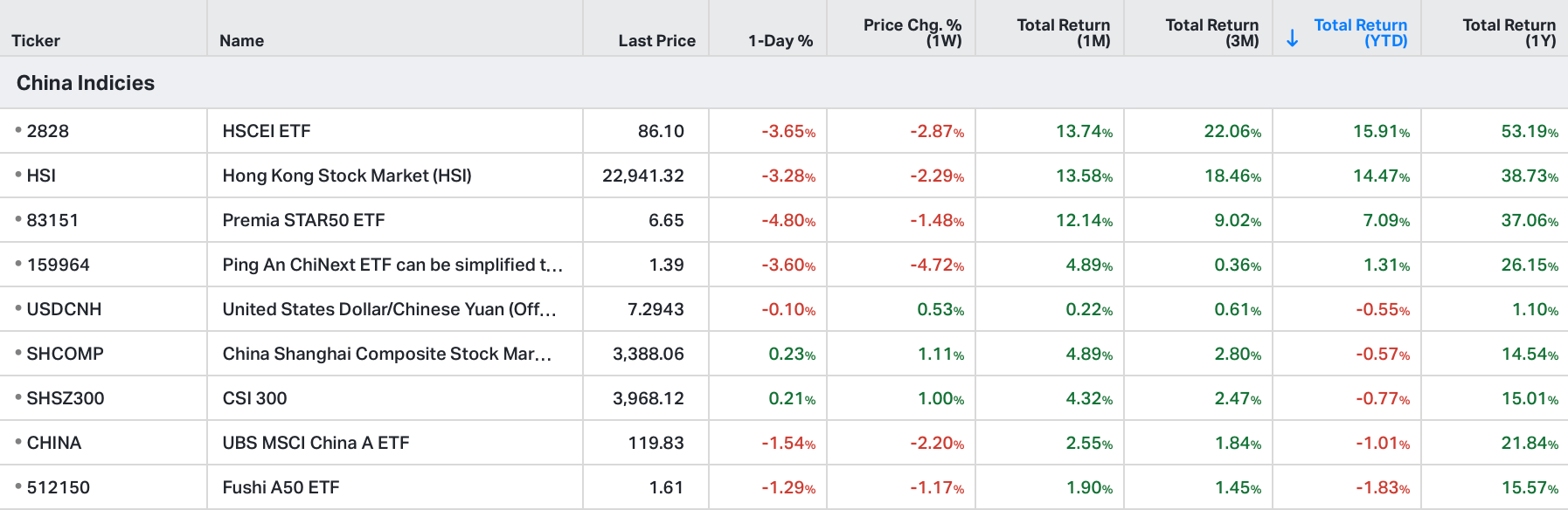

As of February 28, 2025 close of business, here’s a summary of the weekly, month-to-date (MTD), and year-to-date (YTD) performances of major Chinese and Hong Kong stock indices that we follow.

Notes:

Shanghai Composite Index (SHCOMP): Tracks all stocks (A and B shares) traded on the Shanghai Stock Exchange.

CSI 300 Index (SHSZ300): Represents the top 300 stocks traded on the Shanghai and Shenzhen Stock Exchanges.

China A50 Index (512150 CH): Comprises the top 50 A-share companies listed on the Shanghai and Shenzhen Stock Exchanges.

ChiNext Price Index (159954 CH): Focuses on innovative and high-growth enterprises listed on the Shenzhen Stock Exchange.

SSE STAR 50 Index (83151 HK): Represents the top 50 companies listed on the Shanghai Stock Exchange’s STAR Market, emphasising science and technology innovation.

Hang Seng Index (HSI): Measures the performance of the largest companies listed on the Hong Kong Stock Exchange.

Hang Seng China Enterprises Index (2828 HK): Includes major H-share companies listed in Hong Kong.

Currency Considerations:

Chinese Indices (SSEC, CSI300, China A50, CNT, STAR50): These indices are denominated in Chinese Yuan (CNY). To present their performance in USD terms, currency exchange rate fluctuations between the CNY and USD have been considered.

Hong Kong Indices (HSI, HSCEI): Denominated in Hong Kong Dollars (HKD). Their performance in USD terms reflects the HKD/USD exchange rate stability, as the HKD is pegged to the USD.

Weekly Relative Performance Observations:

Performance in Chinese Equities

1. SSE (Shanghai Composite) (-1.72%)

Highlights: The Shanghai Composite posted a weekly loss, with most sectors under pressure.

Context: Investor caution and lack of strong policy catalysts contributed to subdued sentiment. While valuations remain relatively attractive, near-term uncertainties limited buying enthusiasm.

2. SSE-SZSE 300 (-2.22%)

Highlights: Large-cap A-shares retreated, led by weakness in financials and industrials.

Context: Despite some resilience in defensive sectors, the broader market mood was weighed down by global risk-off trends and concerns about China’s growth trajectory.

3. SZSE Composite (-3.46%)

Highlights: Technology and consumer names were among the laggards, reversing part of their earlier gains.

Context: Profit-taking in high-valuation stocks contributed to the broader decline, reflecting investors’ sensitivity to tighter monetary conditions worldwide.

4. ChiNext (-4.87%)

Highlights: The growth-heavy board underperformed, as smaller-cap tech and biotech names saw significant selling.

Context: Valuation concerns and mixed earnings results in certain high-growth sectors weighed on ChiNext, which had previously benefited from optimism around innovation and policy support.

5. Shenzhen100 (-3.30%)

Highlights: Key technology and consumer companies listed in Shenzhen declined, mirroring the tech pullback seen elsewhere in the market.

Context: Domestic funds turned defensive, favoring more stable, policy-aligned names over higher-beta growth shares.

Regional Peers’ Performance

Japan (TOPIX: -1.99%, Nikkei 225: -1.68%)

Highlights: Japanese equities fell modestly, influenced by global risk aversion.

Context: Corporate governance reforms and decent earnings reports offered some support, but were not enough to offset broader selling pressure.

KOSPI (South Korea: -0.45%)

Highlights: The KOSPI outperformed most Chinese indices, though it still ended the week in negative territory.

Context: Ongoing concerns about semiconductor demand tempered gains, but selective buying in defensive names helped limit losses.

NIFTY 50 (India: -2.10%)

Highlights: Indian equities also declined, largely tracking global trends.

Context: Investors balanced domestic growth prospects against a cautious global backdrop, with foreign institutional flows turning more selective.

Key Takeaways for Chinese Markets

1. Broad-Based Declines

Major onshore indices finished lower, reflecting heightened caution and a pullback in risk appetite. Tech and growth-oriented sectors led the decline.

2. Growth Sectors Under Pressure

Previous optimism around technology, biotech, and other high-valuation segments gave way to profit-taking, as investors reevaluated near-term earnings prospects.

3. Policy Signals Awaited

Market participants remain watchful for additional government support measures to be announced during NPC. The lack of fresh policy catalysts this week contributed to the cautious tone.

In the news this week:

Xi Jinping Emphasizes Stable Growth and Tech Self-Reliance at Politburo Meeting

Announced by: President Xi Jinping (via Politburo Meeting Briefing)

Date: 28 February 2025

Details: Xi Jinping highlighted the importance of maintaining economic stability amid global uncertainties. He underscored the need for stronger technological self-reliance, calling for intensified support for strategic industries such as semiconductors, AI, and renewable energy. Xi also reiterated the government’s commitment to controlling systemic financial risks and promoting balanced regional development.

This Indicates: Beijing’s top leadership remains firmly focused on steering China toward a more innovation-driven economy while safeguarding financial stability. Xi’s remarks reinforce the notion that future policy measures—ranging from fiscal stimulus to tighter oversight of key sectors—will align with these national priorities.

This was all a par of the Politburo of the Communist Party of China convening to review and set the nation’s priorities for 2025, ahead of the upcoming “Two Sessions”—the annual meetings of the National People’s Congress (NPC) and the Chinese People’s Political Consultative Conference (CPPCC).

Key Focus Areas Highlighted:

• Economic Stability: The Politburo emphasized the importance of maintaining economic stability while pursuing technological advancement and development.

• Technological Innovation: There was a strong emphasis on fostering scientific and technological innovation to drive new productive forces, aligning with China’s goals for high-tech industrial self-reliance.

• Domestic Demand Expansion: Strategies to boost domestic consumption and improve investment efficiency were discussed, aiming to strengthen internal economic drivers.

• Market Stability: The leadership underscored the need to stabilize real estate and stock markets, improve living standards, and continue promoting high-level economic openness.

• Risk Mitigation: Efforts to prevent and resolve risks in key sectors and counter external shocks were highlighted to ensure sustained economic recovery.

The meeting primarily focused on reviewing the government work report, which Premier Li Qiang is expected to present at the NPC session beginning on March 5. This report will outline China’s economic targets and priorities for the final year of the 14th Five-Year Plan.

These discussions occur in the context of external challenges, including recent tariff threats from the United States. President Trump announced plans to impose a new 10% tariff on Chinese imports if issues like fentanyl trafficking are not addressed, adding to existing trade tensions.

China’s economy expanded by 5% last year, supported by strong exports and economic stimulus efforts introduced in late September. However, challenges persist, including weak consumer spending, a prolonged downturn in the property market, demographic shifts, and declining business confidence.

The upcoming “Two Sessions” will be closely watched for detailed policy directions addressing these challenges and implementing the priorities set by the Politburo. We’ll have a full preview up on Monday.

China’s Reserve Requirement Ratio System May Be Adjusted

Announced by: People’s Bank of China (PBOC), as reported by Securities Times

Date: 25 February 2025

Details: Analysts suggest the PBOC could relax the lower limit of bank reserves, effectively injecting more liquidity into the financial system. This potential move is part of broader efforts to support economic recovery and offset global headwinds.

This Indicates: A continued accommodative stance by China’s monetary authorities. By freeing up lending capacity, policymakers aim to stimulate growth amid uncertain external demand.

China Puts the Breaks on US Stock Listings for Homegrown Companies

Announced by: China Securities Regulatory Commission (CSRC)

Date: 27 February 2025

Details: The CSRC imposed tighter oversight on smaller Chinese companies seeking U.S. IPOs, citing national security and data protection concerns. As a result, the volume of U.S.-bound listings has declined, and the regulator plans stricter review measures for future overseas IPOs.

This Indicates: Beijing’s effort to retain closer control over data and financial disclosures. It also underscores China’s broader objective to deepen domestic capital markets while reducing reliance on foreign listings. As the capital base broadens, it need quality companies to be available for investment.

PBOC Monetary Policy Committee Member Wang Yiming on Real Estate “Deep Adjustment”

Announced by: People’s Bank of China (via MKTNews)

Date: 25 February 2025

Details: Wang Yiming highlighted that China’s real estate sector is undergoing a “deep adjustment,” leading to reduced market demand. Policymakers are exploring targeted measures to stabilise housing and avoid spillover effects on the broader economy.

This Indicates: The government’s concern over the property market’s drag on growth. Further policy support, possibly through relaxed credit or local government initiatives, may be on the horizon to prevent systemic risks.

China Plans USD 55 Billion Capital Injection into Major Banks

Announced by: Unnamed Government Sources

Date: 26 February 2025

Details: China is set to inject fresh capital into large state-owned banks to strengthen their lending capacity, part of a broader stimulus package aimed at stabilising key sectors, including real estate and manufacturing.

This Indicates: Beijing’s commitment to safeguarding financial stability and fuelling economic recovery. By bolstering major banks, policymakers seek to spur credit growth and address potential liquidity pressures in troubled industries.

Data Released This Week:

Official NBS Manufacturing PMI – February 2025

Announced by: National Bureau of Statistics (NBS)

Date: 28 February 2025

Event: February 2025 Official Manufacturing Purchasing Managers’ Index (PMI)

Details:

China’s official NBS Manufacturing PMI rose to 50.2 in February 2025, up from 49.1 in the previous month and exceeding market expectations of 49.9. This marks the highest reading since last November, attributed to the resumption of factory operations post–Lunar New Year and the effect of various stimulus measures. Key sub-indexes improved:

• Output: 52.5 (up from 49.8)

• New Orders: 51.1 (up from 49.2)

• Buying Levels: 52.1 (up from 49.2)

• New Export Orders: 48.6 (up from 46.4)

• Employment: 48.5 (up from 48.4)

Delivery times lengthened (51.5 vs. 50.3), input costs rose for the first time in four months (50.8 vs. 49.5), and the drop in selling prices slowed (48.5 vs. 47.8). Business confidence dipped slightly from a ten-month high but remained generally optimistic (54.5 vs. 55.3 in January).

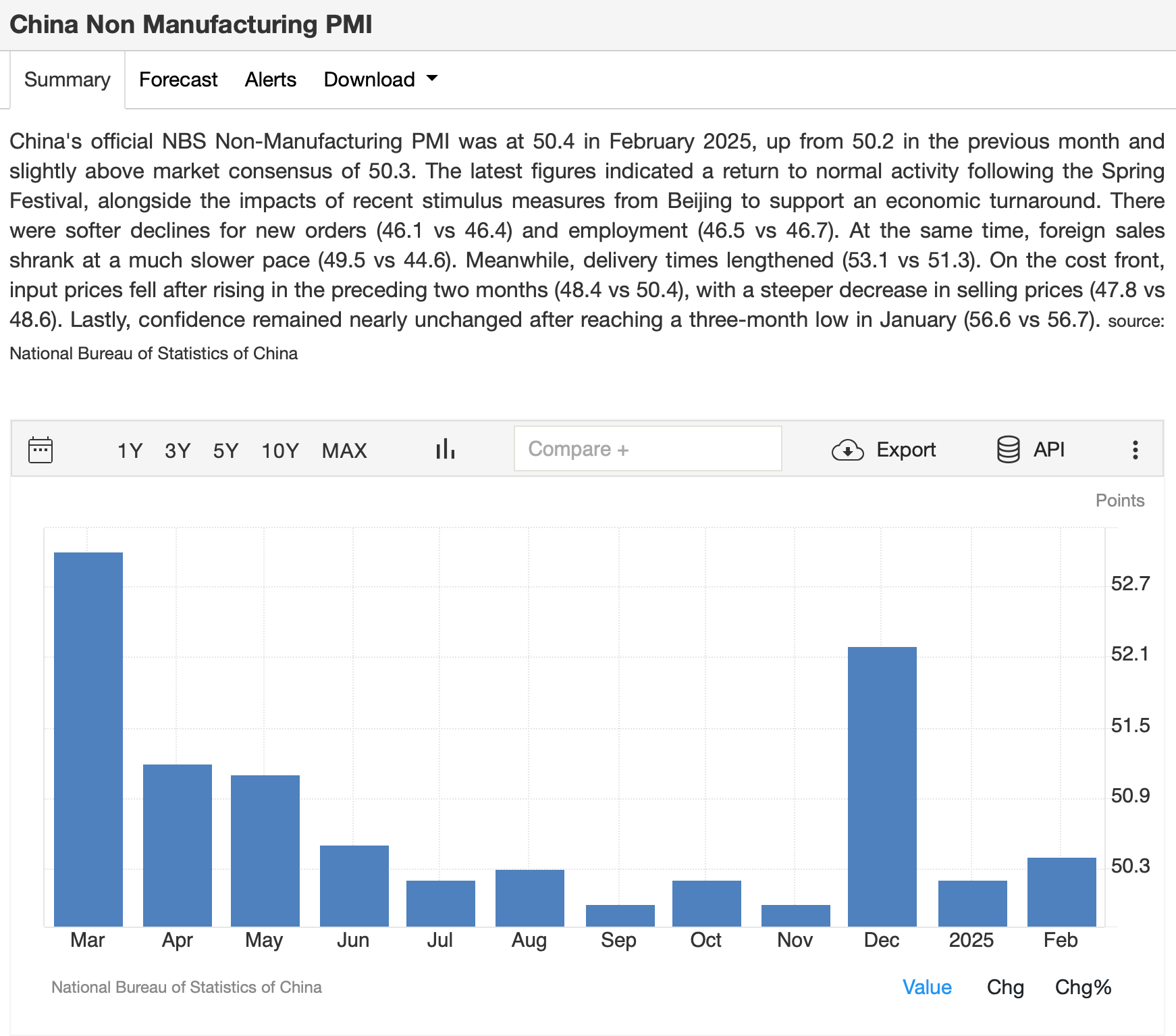

Official NBS Non-Manufacturing PMI – February 2025

Announced by: National Bureau of Statistics (NBS)

Date: 28 February 2025

Event: February 2025 Official Non-Manufacturing Purchasing Managers’ Index (PMI)

Details:

China’s official NBS Non-Manufacturing PMI in February 2025 stood at 50.4, up from 50.2 in January and slightly above consensus estimates of 50.3. The reading suggests a continued, albeit modest, expansion in the services and construction sectors:

• Service Sector Index: 48.5 (vs. 49.7 previously), still signaling softness but showing partial improvement in business volume (46.5 vs. 49.7).

• Foreign Clients: Contracted at a slower pace (no specific sub-index value provided).

• Delivery Times: 53.1 (vs. 51.9), indicating longer lead times.

• Input Prices: 48.9 (vs. 50.4), suggesting a slight rise in costs for a third consecutive month.

• Selling Prices: 47.8 (vs. 48.6), reflecting a steeper decline in output charges.

• Business Confidence: 56.6 (vs. 56.7), essentially unchanged from the three-month low in January.

The post-Spring Festival normalization and ongoing government stimulus measures are helping sustain the sector’s gradual recovery, though external demand remains a concern.

NBS Composite PMI – February 2025

Announced by: National Bureau of Statistics (NBS)

Date: 28 February 2025

Event: February 2025 NBS Composite Purchasing Managers’ Index (PMI)

Details:

China’s NBS Composite PMI Output Index rose to 51.1 in February 2025 from 50.1 in January, marking its strongest expansion in three months. The manufacturing sector rebounded more robustly, while services maintained moderate growth. This comes ahead of the “Two Sessions” (National People’s Congress and Chinese People’s Political Consultative Conference) set for March 5–15, during which policymakers are expected to unveil more pro-growth targets, such as a 5% GDP growth goal, a 4% fiscal deficit ratio, and 2% consumer inflation. Planned measures include boosting consumer spending and fostering private-sector innovation, signaling continued policy support for the economy.

Complete Index Performance List:

General Trends

Chinese equity markets ended mixed this week, with mainland indices posting notable losses and Hong Kongbenchmarks also declining. On the mainland, the Shanghai Composite (SSE) dropped -1.72% to 3,320.90, pressured by weakness in both financial and technology shares. The SSE-SZSE 300 Index (large-cap A-shares) lost -2.22% to 3,890.05, reflecting subdued sentiment among institutional investors.

Shenzhen’s boards fared worse. The ChiNext Index plunged -4.87% to 2,170.39, reversing prior gains in biotech and AI segments. The Shenzhen 100 Index slipped -3.30% to 4,668.34, amid broad-based selling in innovation-driven companies.

In Hong Kong, the Hang Seng Index (HSI) ended the week down -2.38%, while the Hang Seng TECH Index (HS TECH) declined -3.02%. Renewed global macro concerns and profit-taking in Chinese tech overshadowed earlier optimism, leading to a net pullback in Hong Kong–listed names.

Relative Underperformance

ChiNext (-4.87%): The growth-heavy ChiNext was the worst performer, highlighting investor profit-taking in high-valuation sectors such as biotech, semiconductors, and AI.

Hang Seng TECH (HS TECH) (-3.02%): Hong Kong–listed tech names declined, as sentiment toward internet and platform companies softened amid broader risk-off conditions.

Shenzhen 100 (-3.30%): Shenzhen’s large-cap innovators also faced losses, reflecting a shift away from higher-beta, innovation-driven stocks as global uncertainties weighed on risk sentiment.

SSE-SZSE 300 (-2.22%): Large-cap A-shares tracked lower, indicating that even well-established, blue-chip companies could not escape the week’s risk-off mood.

Hang Seng Index (HSI) (-2.38%): Despite some mid-week stabilising factors, the HSI ended in negative territory, as global headwinds and reduced appetite for Chinese financials and real estate weighed on overall performance.

Sector-Specific Dynamics

Technology & Innovation: Mainland tech stocks, especially on the ChiNext, faced a sell-off. In Hong Kong, tech shares were similarly pressured, driving the HS TECH Index to a -3.02% weekly loss.

Financials & Real Estate: Mainland financials underperformed, amid concerns over loan quality and slower growth. In Hong Kong, property names saw limited gains early in the week but succumbed to broader selling pressure, with real estate indices ending mixed.

Industrials & Commodities: The SSE Commodity Equity Index (from your screenshot, -1.22% for the week) reflected softening external demand. Industrials had pockets of resilience but were generally weighed down by the broader market sell-off.

Large-Cap vs. Small-Cap Performance

Large-Cap Indices: The SSE-SZSE 300 fell -2.22%, slightly less severe than some of the small-cap boards, but still indicative of a broad-based risk aversion.

Small-Cap & Innovation-Focused Indices The ChiNext (-4.87%) and Shenzhen 100 (-3.30%) underperformed, highlighting a rotation away from higher-risk, higher-valuation stocks in the current environment.

Additional Observations

Profit-Taking in Growth Sectors: After several weeks of optimism, especially around AI and biotech, investors locked in gains amid valuation worries and macro uncertainty.

Global Macro Concerns: Renewed focus on global monetary tightening and geopolitical tensions contributed to a defensive shift, with market participants becoming more cautious.

Hong Kong’s Pullback: Both the HSI (-2.38%) and HS TECH (-3.02%) ended lower, underscoring how fragile sentiment remains in offshore Chinese markets when faced with external headwinds.

Policy Signals: Investors are still waiting for stronger, more concrete policy measures—particularly around real estate and tech—to offset global volatility.

Key Takeaways

Broad-Based Declines: Mainland indices posted sizable losses, led by the ChiNext and Shenzhen boards, while Hong Kong’s HSI and HS TECH also finished the week in negative territory.

Growth Under Pressure: High-valuation tech and innovation-driven names saw the steepest declines, as investors grew wary of lofty valuations amid uncertain global conditions.

Shift Toward Defence: The retreat from high-growth plays suggests some rotation into less volatile or undervalued sectors, though not enough to buoy the broader indices.

Cautious Sentiment: Without fresh policy catalysts or a clear improvement in global risk appetite, Chinese equities may remain volatile in the near term, with Hong Kong–listed names particularly sensitive to foreign capital flows.

Top 20 Index Constituents:

Bottom 20 Index Constituents:

Corporate News and Results this week:

Huawei Achieves Key Breakthrough in AI Chip Production

Announced by: Huawei

Date: 25 February 2025

Details: Huawei unveiled its latest Ascend 910C processors, achieving a roughly 40% production efficiency boost compared to prior generations. The improvement underscores Huawei’s focus on AI and high-performance computing, challenging established players like Nvidia.

This Indicates: China’s ongoing drive toward technological self-reliance. Despite external trade pressures, Huawei’s chip progress showcases Beijing’s intent to nurture homegrown innovation and reduce reliance on foreign suppliers.

Announced by: Leading Chinese NEV Companies

Date: 1 March 2025

Event: February 2025 New Energy Vehicle (NEV) Sales Report

Details:

China’s major NEV manufacturers have reported their February 2025 delivery figures, showing a mix of year-over-year growth and seasonal slowdowns following the Lunar New Year. While some brands sustained strong momentum, others experienced sequential declines due to production adjustments and shifting consumer demand.

Company Breakdown

Nio Inc.

Total Deliveries: 13,192 units

Month-over-Month Change: +14.99% for Nio brand, -31.51% for Onvo sub-brand

Highlights:

The ES6 and ET5 models continued to lead Nio’s portfolio.

Nio expanded its battery swap station network, reinforcing its infrastructure advantage.

Xpeng Motors

Total Deliveries: 30,453 units

Month-over-Month Change: Stable for the fourth consecutive month above 30,000 units

Highlights:

Strong performance from the P7 sedan and G9 SUV.

Xpeng emphasized upcoming software updates for autonomous driving features.

Li Auto

Total Deliveries: 26,263 units

Month-over-Month Change: -12.24%

Year-over-Year Change: +29.69%

Highlights:

L7 and L9 SUVs remain top-selling models.

The company attributed its monthly decline to seasonal effects post-Lunar New Year.

Leapmotor

Total Deliveries: 25,287 units

Month-over-Month Change: Flat vs. January

Year-over-Year Change: +167.78%

Highlights:

The C11 SUV continues to be a volume driver.

Leapmotor strengthened its presence in lower-tier cities.

Zeekr (Geely Group)

Total Deliveries: 31,277 units

Month-over-Month Change: -25.56%

Year-over-Year Change: +50.96%

Highlights:

Zeekr 001 and Zeekr X remained top-selling models.

The company is actively expanding into European markets.

Pending Announcements

• BYD and Tesla China have not yet reported their February 2025 sales figures.

Key Takeaways

Xpeng maintains stability, staying above 30,000+ units for the fourth straight month.

Leapmotor posts the strongest year-over-year growth (+167.78%), showing increasing market traction.

Zeekr sees the highest YoY growth among premium NEVs (+50.96%).

Li Auto delivers strong annual growth (+29.69% YoY), though sequential decline reflects post-holiday seasonality.

BYD & Tesla China figures remain awaited, which could shift overall market rankings once released.

While monthly deliveries softened for some brands due to the Lunar New Year slowdown, overall growth remains strong, especially for companies with tech-driven features, premium models, and expanding infrastructure. The sector remains highly competitive, with brands vying for leadership in autonomy, battery efficiency, and international expansion.

Announced by: China International Capital Corp (CICC) & China Galaxy Securities

Date: 28 February 2025

Event: Reports of a Potential Merger Between CICC and China Galaxy Securities

Details:

Recent reports indicate that China International Capital Corp (CICC) and China Galaxy Securities are in discussions for a potential merger that would create China’s third-largest brokerage firm, with combined assets of approximately 1.4 trillion yuan (USD 193 billion). According to sources, the deal has government backing and may be executed via a share swap, with an official announcement expected in the coming weeks.

However, both CICC and China Galaxy Securities have denied the merger reports. In separate statements filed with the Hong Kong Stock Exchange, the companies stated that they have not received any information from government departments, regulatory authorities, or shareholders regarding such a transaction.

Market speculation surrounding the merger aligns with Beijing’s broader strategy to consolidate China’s securities industry, creating larger investment banks that can compete with global financial giants like Goldman Sachs and Morgan Stanley. The Chinese government has encouraged mergers and acquisitions within the brokerage sector to strengthen domestic financial institutions and enhance capital market stability.

Following the reports, shares of both companies surged:

• CICC’s Shanghai-listed shares jumped 10%, while its Hong Kong-listed shares gained 18%.

• China Galaxy Securities saw a 10% rise in Shanghai and a 20% increase in Hong Kong.

Despite the denials from both companies, investors and industry analysts remain watchful for further developments. An official confirmation or clarification is awaited from the companies or regulatory authorities.

THE NPC week is always interesting so we’re looking forward to it. Let the fun part of the year begin!

Have a great week ahead,

Leonid