China Weekly Wrap: Markets, Macro & Tech – Key Developments This Week

a week that was 7 - 11 April 2025

Good afternoon,

Welcome back to The China Weekly Wrap from Panda Perspectives—your digest of the key developments in China’s financial markets and macro landscape. And this week, there’s plenty to unpack.

We’ve also been busy on the blog with two new deep dives: one on UBTech, part of our Humanoid Robotics series, and another on EHang, where we explore what China’s drone ambitions say about industrial policy, technology leadership, and market structure.

UBTech: The Next Step in Humanoid Robotics

EHang: Flying Taxis, Chinese Policy, and the Urban Air Future

If you haven’t had a chance to read them yet, do take a look. Both of them are paywalled—so if you’re not already a subscriber, now’s a great time to join. We’d love to have you.

Coming up this weekend: a full portfolio review for premium members, where we’ll walk through our real-time reaction to the recent market volatility.

Next week is Marco week, stay tined for our 3 (by the looks of things) part series on what happening in China and how it can develop from here.

Serious about Asia investing? Your process needs more Panda. We full appreciate that for some this is not enough and you’d like a more personalised service that will help get results in China and Asia. Currently we’re doing calls on China consumer, 2Q25 Outlook and yes, Robotics. See what we offer here, and connect with us today or message us directly.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

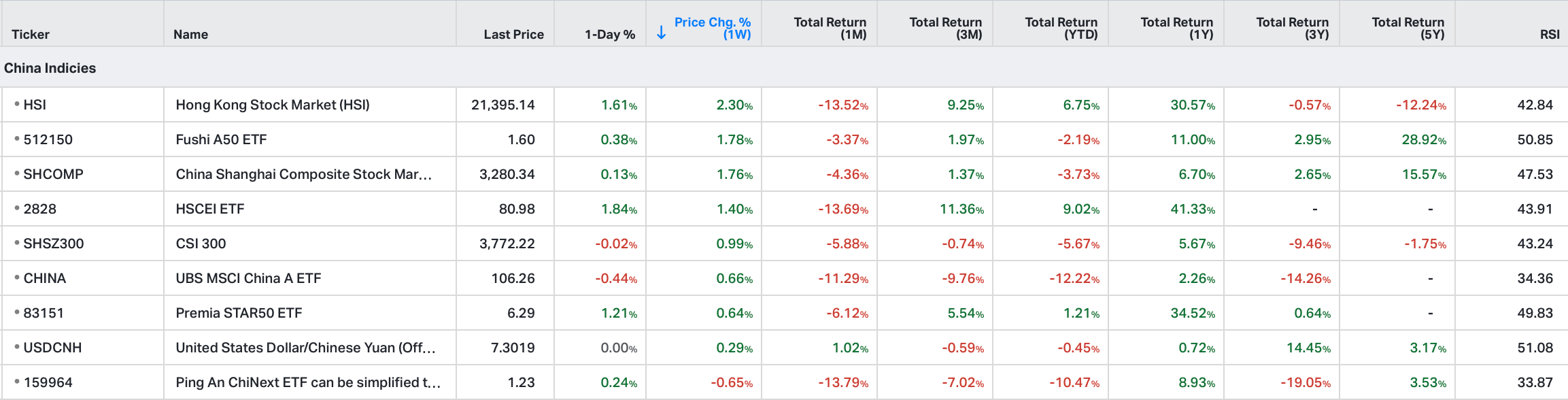

As of April 18, 2025 close of business, here’s a summary of the weekly, month-to-date (MTD), and year-to-date (YTD) performances of major Chinese and Hong Kong stock indices that we follow. We will do an end of the month reconciliation at the end of April to see whats what across a few weeks. (*see notes at the end of the post).

Weekly Relative Performance Observations

Performance in Chinese Equities

HSI (Hang Seng Index) (+2.30%)

Highlights: The HSI rebounded strongly, outperforming most Chinese indices this week.

Context: Gains were led by financials and red chips, as signs of stabilisation in capital flows and some foreign re-entry helped sentiment in offshore markets.

HSCEI ETF (2828) (+1.40%)

Highlights: The HSCEI ETF posted a solid weekly gain, snapping a multi-week losing streak.

Context: Investors rotated back into SOEs and large-cap names amid signs of policy stability and relative value versus global peers.

Shanghai Composite (SHCOMP) (+1.76%)

Highlights: The SHCOMP advanced modestly despite continued economic uncertainty.

Context: Defensive sectors and dividend-paying stocks led the gains as investors remained cautious amid lack of stimulus headlines.

CSI 300 (SHSZ300) (+0.99%)

Highlights: The CSI 300 rose but underperformed the SHCOMP, weighed down by subdued bank and energy names.

Context: Investors rotated slightly out of large-cap SOEs toward more balanced exposure as earnings season got underway.

ChiNext ETF (159964) (-0.65%)

Highlights: ChiNext was the only major Chinese index to decline this week.

Context: Growth and innovation-heavy names remained under pressure as risk appetite stayed muted and valuations remained sensitive to interest rate expectations.

Regional Peers’ Performance

MSCI Singapore (+5.45%)

Highlights: Singapore led regional gains, extending its outperformance streak.

Context: The market benefitted from strength in financials and REITs, alongside rising investor interest in ASEAN as a relative safe haven.

TOPIX (Japan) (+3.74%)

Highlights: Japanese equities rallied strongly, with the TOPIX up nearly 4%.

Context: A weaker yen and solid corporate earnings continued to attract foreign inflows, particularly into cyclical and value stocks.

KOSPI (Korea) (+2.08%)

Highlights: Korea’s benchmark index advanced on the back of improved global tech sentiment.

Context: Semiconductors rebounded, while institutional buying supported the market throughout the week.

Shanghai Composite (China) (+1.76%)

(For comparison purposes with regional peers.)

CSI 300 (China) (+0.99%)

(For comparison purposes with regional peers.)

FTSE TWSE Taiwan 50 (-2.36%)

Highlights: Taiwan’s benchmark index posted the weakest performance among regional majors.

Context: Concerns over tech inventory cycles and potential geopolitical stress weighed on semiconductors and large-cap exporters.

Key Takeaways for Chinese Markets

Offshore Rebound: Hong Kong markets staged a comeback this week, outperforming onshore indices for the first time in several weeks.

Cautious Optimism: While gains were broad-based, investor confidence remains fragile. Trading volumes were moderate, suggesting this could be a technical bounce.

Growth Still Lags: The ChiNext and other innovation-heavy segments continued to underperform, showing that risk appetite hasn’t fully returned.

Macro and Policy Still in Focus: Investors remain watchful for any signals from Beijing on fiscal or monetary easing. Without a policy catalyst, rallies may lack staying power.

In The News This Week

Diplomacy & External Relations

President Xi Concludes State Visit to Vietnam

Announced by: Chinese State Media

Date: April 10–12, 2025

Details: President Xi’s visit focused on deepening strategic cooperation with Vietnam, including Belt and Road integration, energy and logistics projects, and cross-border trade. A total of 36 cooperation agreements were signed across digital economy, transport infrastructure, and green development.

This Indicates: China is strengthening economic diplomacy in Southeast Asia to hedge against decoupling pressures from the West and to secure key regional partnerships.

President Xi Begins State Visit to Malaysia

Announced by: Chinese State Media

Date: April 18, 2025

Details: The Malaysia trip saw the signing of 23 bilateral agreements covering palm oil, clean energy, digital trade, and semiconductor collaboration. Beijing also committed to expanding the East Coast Rail Link under Belt and Road.

This Indicates: Continued Belt and Road expansion, with a focus on deepening China’s role in ASEAN infrastructure and value chains.

Malaysia’s Anwar: ASEAN Rejects Unilateral Tariffs, Seeks Stronger Ties with China

Announced by: MKTNews

Date: April 17, 2025

Details: Prime Minister Anwar Ibrahim reiterated Malaysia’s rejection of unilateral tariff actions and signaled support for multilateral economic cooperation. He stressed ASEAN’s collective interest in deepening ties with China to build economic resilience.

This Indicates: A broader regional pushback against protectionism, and ASEAN alignment with China as trade frictions with the West escalate.

Science, Tech & Strategic Innovation

Chinese Scientists Develop Ultrafast Memory Chip with Zero Standby Power

Announced by: Nature Magazine

Date: April 17, 2025

Details: Researchers from Fudan University reported a breakthrough in memory chip design using antiferroelectric materials. The new prototype stores data at picosecond switching speeds while consuming virtually zero standby power, potentially outperforming existing DRAM and flash memory solutions.

This Indicates: A significant milestone in China’s bid for semiconductor independence, with implications for both commercial and defense computing. While not immediately investable, it reinforces China’s push to lead in frontier tech.

Trade War Update

China Orders Halts to Boeing Jet Deliveries as Trade War Expands

Announced by: Sources via MKTNews

Date: April 15, 2025

Details: China instructed its airlines to halt new Boeing jet deliveries and suspend purchases of U.S.-made aircraft parts following steep U.S. tariffs on Chinese goods (up to 145%). Beijing responded with 125% retaliatory tariffs on U.S. products. Some Boeing 737 Max deliveries may be allowed case-by-case, but the move is a significant blow to Boeing’s position in China.

This Indicates: Escalating retaliation in the trade war, affecting the aviation sector and signaling a pivot toward Airbus and China’s own Comac C919 for future aircraft demand.

China Open to Talks If Trump Shows Respect, Names Point Person

Announced by: Sources via MKTNews

Date: April 16, 2025

Details: China laid out conditions for resuming trade talks, demanding a designated U.S. negotiator backed by Trump, curbs on anti-China rhetoric, and willingness to address issues like sanctions and Taiwan.

This Indicates: A conditional opening for diplomacy, though Beijing is clearly asserting the need for a more respectful and predictable U.S. stance before meaningful negotiations can proceed.

China Policy & Macro Commentary

DFRatings Signals Rate & RRR Cut Likely in Q2

Announced by: DFRatings

Date: April 14, 2025

Details: DFRatings (东方金诚信用评估有限公司 or Dongfang Jincheng, a Chinese domestic credit rating agency headquartered in Beijing). believes the timing has now matured for the PBOC to cut both policy rates and the reserve requirement ratio (RRR), potentially bringing easing forward within Q2.

This Indicates: Growing market consensus that monetary easing is imminent, likely in response to weak credit growth and external headwinds.

PBOC Policy Framework Clarified via State Media

Announced by: Financial Times (China) via social media

Date: April 14, 2025

Details: A PBOC-affiliated publication outlined three scenarios for further easing: (1) external shocks like new U.S. tariffs, (2) fiscal+monetary coordination to reduce crowd-out risk, and (3) systemic instability in asset markets.

This Indicates: A clear framework guiding future PBOC actions, emphasizing a domestic-led “dual circulation” model rather than RMB depreciation or export subsidies.

Premier Li Urges Clearer Market Communication

Announced by: Chinese Premier Li via MKTNews

Date: April 17, 2025

Details: In a series of remarks, Premier Li called for more transparent and stable communication with markets, a predictable development environment for enterprises, and better delivery of policy to guide expectations.

This Indicates: A response to investor frustration over inconsistent policy signals, with a push toward improving credibility and forward guidance.

Steel Exports Hit Highest Q1 Levels Since 2016

Announced by: Reuters

Date: April 14, 2025

Details: China’s Q1 steel exports reached their highest level since 2016, signaling robust overseas demand and possible inventory shifts in anticipation of trade friction.

This Indicates: China’s industrial exporters are still competitive globally, though the surge may also reflect front-loading due to rising geopolitical tensions.

Data Released This Week

Macro Week: Strong Data, Growing Concerns

China’s latest macro data came in stronger than expected across several fronts—GDP, industrial production, and retail sales all surprised to the upside, suggesting the recovery still has legs. But the intensifying trade war and uncertain policy signals continue to cloud the outlook. That’s why this week, we’re going deeper than usual on the data and the market context around it. Welcome to Macro Week at Panda Perspectives April 22-27 2025.

Q1 2025 GDP Growth: +5.4% YoY

Exceeding expectations of 5.1% and matching Q4 2024’s growth rate.

This Indicates:

Strong Start to the Year: The economy showed resilience, driven by robust industrial output and a surge in exports ahead of new U.S. tariffs.

Export Front-Loading: The significant export growth may be attributed to businesses accelerating shipments before the implementation of higher tariffs.

Sustainability Questions: Analysts caution that this momentum may not be sustainable as the full impact of the trade war unfolds in subsequent quarters.

Fiscal Revenue (Q1 2025): -1.1% YoY

Total fiscal revenue declined to 6 trillion yuan ($821.54 billion), while fiscal expenditure rose by 4.2%.

This Indicates:

Budgetary Strains: The decline in revenue, coupled with increased spending, suggests mounting fiscal pressures.

Stimulus Measures: The government is likely increasing expenditure to support economic growth amid external challenges.

Debt Concerns: The widening fiscal deficit may raise concerns about the sustainability of public finances, especially in the context of ongoing trade tensions.

Fixed Asset Investment (FAI) Q1 2025: +4.5% YoY

A slight deceleration from the 4.8% growth in the first two months of the year.

This Indicates:

Mixed Investment Climate: While infrastructure and manufacturing investments remain robust, the property sector continues to lag.

Private Sector Hesitancy: Private investment growth remains subdued, reflecting cautious business sentiment amid economic uncertainties.

Policy Focus: Authorities may need to implement measures to boost private investment and address sectoral imbalances.

Retail Sales (Q1 2025): +4.6% YoY

An improvement from the 3.5% growth in the previous quarter.

This Indicates:

Consumer Spending Recovery: Retail sales data suggests a rebound in consumer confidence and spending.

Policy Support Effectiveness: Government initiatives, such as consumption vouchers and subsidies, are likely contributing to the uptick in retail activity.

Sustainability Watch: Continued monitoring is necessary to assess whether this recovery in consumption is sustainable in the face of external headwinds.

Industrial Production (March 2025): +6.5% YoY

An acceleration from the 5.8% growth recorded in February.

This Indicates:

Manufacturing Strength: The industrial sector shows robust growth, potentially driven by increased demand and preemptive production ahead of tariff implementations.

Export-Oriented Output: The surge may reflect efforts to fulfill international orders before new trade barriers take effect.

Future Outlook: Sustaining this growth may be challenging as global demand adjusts to the evolving trade landscape.

New Credit Issuance (Q1 2025): +18.5% YoY

Total new credit reached 15.2 trillion yuan, with significant contributions from government bond issuance.

This Indicates:

Stimulus-Driven Credit Expansion: The increase in credit suggests proactive fiscal measures to support economic activity.

Government-Led Growth: The surge is primarily driven by public sector borrowing, highlighting the government’s role in sustaining growth.

Private Sector Caution: Despite overall credit growth, private sector borrowing remains tepid, indicating lingering risk aversion among businesses.

New Yuan Loans (March): CNY 3.64T

Above consensus of CNY 3T and well above February’s CNY 1.01T.

This Indicates:

Credit Rebound: A strong jump in new lending suggests early effects of monetary easing or preemptive borrowing ahead of expected policy shifts.

Corporate + Government Borrowing: Local government bond issuance and business credit drove the rebound.

Supportive Liquidity Conditions: Reinforces the PBoC’s cautious but pro-growth stance.

M2 Money Supply YoY (March): +7.0%

Flat versus February and slightly below the 7.1% consensus.

This Indicates:

Stable Liquidity Growth: Money supply growth remains steady, suggesting no major injection of systemic liquidity yet.

Wait-and-See Mode: Indicates the PBoC may still be holding fire on aggressive monetary easing.

Outstanding Loan Growth YoY (March): +7.4%

Slightly higher than February’s 7.3%.

This Indicates:

Loan Demand Is Picking Up: Possibly driven by SOEs and infrastructure-related sectors.

Mild Improvement in Credit Transmission: Private sector loan appetite still unclear.

Total Social Financing (March): CNY 5.89T

Well above consensus (CNY 4.8T) and more than double February’s CNY 2.23T.

This Indicates:

Heavy Front-Loading: Government bond issuance and off-balance-sheet lending surged.

Policy Push: Suggests authorities are accelerating support to offset trade and external weakness.

Exports YoY (March): +12.4%

Huge rebound from February’s +2.3%, beating consensus (+4.4%).

This Indicates:

Front-Running the Trade War: Exporters likely rushed shipments before U.S. tariff hikes.

Short-Term Boost: Risk of reversal as tariffs begin to bite in Q2.

Imports YoY (March): -4.3%

Better than February’s -8.4% but still in contraction.

This Indicates:

Weak Domestic Demand: Still-low import activity reflects soft consumer and industrial demand.

Inventory Drawdowns: May also reflect lower raw material restocking.

Balance of Trade (March): $102.64B

Down from $170.5B in February but well above consensus.

This Indicates:

Export-Led Surplus: March surplus was driven almost entirely by exports, not domestic demand.

Vulnerable to Retaliation: Highlights asymmetry that could be targeted in trade negotiations.

Industrial Capacity Utilisation (Q1): 74.1%

Down from 76.2% in Q4 2024.

This Indicates:

Utilization Slippage: Despite strong production, spare capacity widened.

Supply-Demand Imbalance: Suggests continued structural overcapacity in heavy industry.

Urban Unemployment Rate (March): 5.2%

Down from 5.4% in February.

This Indicates:

Labour Market Recovery: Gradual improvement, though youth unemployment (not shown) remains elevated.

Support for Consumption: Mildly positive signal for demand outlook.

House Price Index YoY (March): -4.5%

Slightly better than February’s -4.8%.

This Indicates:

Property Slump Not Over: Still deeply negative YoY, with Tier 3/4 cities worst affected.

Policy Pressure: Adds urgency for targeted real estate support measures.

FDI YTD YoY (March): -10.8%

Improved from February’s -20.4%.

This Indicates:

Capital Flow Strain Easing Slightly: Still negative, but recovering from earlier lows.

Geopolitical Drag Continues: Trade war + regulatory uncertainty remain key deterrents.

Loan Prime Rate 5Y: 3.95% (Unchanged)

This Indicates:

Wait-and-See Mode: PBoC holding steady despite market expectations for easing.

Cuts Still Likely in Q2: Signals that policymakers may be saving firepower as the trade war escalates.

Complete Index Performance List:

General Trends

Chinese equity markets saw a broad-based rebound this week, with both mainland and Hong Kong indices closing in positive territory. The recovery was underpinned by stronger-than-expected macro data (Q1 GDP, retail sales, industrial output), tentative signs of policy support, and diplomatic momentum from President Xi’s Southeast Asia visits.

The Shanghai Composite Index (SSE) rose +1.19% to 3,276.73, helped by state-linked rhetoric around economic stability and improving investor sentiment.

The CSI 300 Index edged up +0.59% to 3,772.52, supported by SOE buying and expectations for upcoming stimulus, though large-caps underperformed smaller peers.

The ChiNext Index fell slightly (-0.64%) to 1,913.97, weighed by continued pressure on speculative growth names, though losses narrowed into Friday.

In Hong Kong, sentiment was stronger:

The Hang Seng Index (HSI) climbed +2.30%, reversing prior weeks’ losses on the back of property and finance strength.

The Hang Seng Tech Index (HS TECH) rose +1.90%, despite headwinds from U.S.-China tensions.

The Hang Seng China Enterprises Index (HSCEI) gained +1.23%, led by financials and energy sectors.

Relative Outperformance

HSI Financials (HSI FIN): +4.60% – Led gains on the back of rate-cut speculation and a stabilising yield curve.

HSI Property (HSI PROP): +3.90% – Strong bounce in oversold names, despite persistent weakness in the mainland housing market.

SSE Conglomerates: +2.76% – Lifted by infrastructure-linked SOEs and fiscal stimulus bets.

HSMOGI (Oil & Gas Index): +4.60% – Benefited from rising crude prices and supply-side tailwinds.

SSE B Index: +1.79% – Continued to attract defensive inflows due to foreign investor preference.

Sector-Specific Dynamics

Technology & Innovation

HS TECH (+1.90%) and ChiNext (-0.64%) saw mixed performance, with tech sentiment stabilising but failing to break out.

Despite strong industrial output and new memory tech headlines, the lack of concrete stimulus for innovation sectors capped gains.

Financials & Real Estate

HSI FIN (+4.60%) and SSE Dividend Index (+1.86%) showed strength as investors priced in potential rate cuts.

Property sectors rebounded (e.g., HSI PROP +3.90%), despite the house price index remaining deeply negative YoY (-4.5%).

Industrials & Commodities

SSE Commodity Equity (+0.57%) and HSI COM&IND (+0.90%) were steady, as optimism about domestic infrastructure offset concerns about falling global capacity utilisation.

Utilities and dividend-heavy sectors saw modest gains as defensive plays came back into favour.

Large-Cap vs. Small-Cap Performance

Large-Cap Stability: Indices like CSI 300 (+0.59%) and SSE 50 (+1.45%) recovered from prior weakness, supported by institutional flows into SOEs and financials.

Mid & Small-Cap Lag: Names in ChiNext (-0.64%), SME Innovation (-0.18%), and SSE Mid Cap (+0.66%)underperformed, reflecting tepid risk appetite and lingering concerns around profitability.

Defensive Tilt: B-shares, high-yield utilities, and mid-cap biotech names continued to attract relative interest.

Key Takeaways

Macro Strength Supported a Bounce

Q1 GDP (+5.4%), retail sales (+5.9%), and industrial output (+7.7%) all surprised to the upside, validating the idea of a bottoming growth cycle—at least for now.

Hong Kong Markets Led Rebound

HSI (+2.30%) and HSCEI (+1.23%) outperformed mainland indices, driven by foreign inflows and hopes for more pragmatic diplomacy after Xi’s regional visits.

Tech and Growth Still Shaky

ChiNext (-0.64%) and SME Innovation (-0.18%) continue to underperform amid valuation concerns and limited policy follow-through on innovation.

Volatility Subsided, But Risks Remain

The VHSI fell -21.65%, suggesting fading panic, but lingering trade war and policy credibility concerns keep investors cautious.

Capital Rotation Toward Yield and Safety

Financials, SOEs, and income-generating sectors like utilities and energy saw inflows, reflecting a defensive but constructive tone.

Narrative Shifts but Clarity Still Lacking

While this week saw better data and coordinated messaging (Li’s market stability remarks, DFRatings’ comments), markets continue to wait for action over headlines—especially in tech, property, and fiscal delivery.

Top 20 Index Constituents:

Corporate News and Results this week:

ENGINEAI Launches Two Consumer-Grade Humanoid Robots

Announced by: ENGINEAI

Date: April 15, 2025

Details: ENGINEAI, a Chinese robotics startup, launched two humanoid robots: the PM01 priced at 188,000 yuan and the SA01 at 42,000 yuan. PM01 is aimed at institutional and R&D use, while SA01 targets educational and consumer settings.

This Indicates: A growing trend of commercial viability in China’s humanoid robotics race, with lower-cost units bringing potential for broader adoption.

Goldman Sachs Warns of $800 Billion U.S. Outflows from China Stocks in Extreme Scenario

Announced by: Goldman Sachs

Date: April 17, 2025

Details: Goldman outlined a worst-case decoupling scenario where U.S. investors could be forced to divest $800 billion in Chinese equities, while Chinese investors might liquidate up to $1.7 trillion in U.S. assets.

This Indicates: How rapidly financial fragmentation could escalate if geopolitical tensions deepen—underscoring the risk premium on China exposure.

Chagee Tea Chain Raises $411 Million in U.S. IPO

Announced by: Bloomberg / Chagee Holdings

Date: April 16, 2025

Details: Premium tea brand Chagee completed a $411 million IPO in the U.S., pricing at the top of its marketed range. The Shanghai-based company sold 14.7 million ADSs at $28 apiece, pushing its founder into billionaire status.

This Indicates: Appetite for distinctive Chinese consumer brands remains healthy among global investors—even amid geopolitical volatility.

Baidu’s Apollo Go Expands Driverless Zone in Wuhan

Announced by: Baidu

Date: April 12, 2025

Details: Baidu received approval to expand its driverless ride-hailing area in Wuhan to 250 square kilometers—China’s largest fully autonomous operational zone to date.

This Indicates: Continued regulatory momentum for China’s autonomous driving sector and a lead for Baidu in commercializing robotaxi services.

Alibaba to Spin Off Freshippo Grocery Chain

Announced by: Alibaba

Date: April 11, 2025

Details: Alibaba revived its plan to spin off Freshippo (Hema) with a targeted Hong Kong IPO later this year. The move is part of its ongoing restructuring to unlock value and focus on core e-commerce operations.

This Indicates: A signal that capital markets are re-opening to strategic tech IPOs and that Alibaba is pushing ahead with asset-light transitions.

The tariffs and trade war remain the main drivers of the markets, the market is wobbly, and there is not a particular focus on quality it doens’t appear. Nevertheless we continue to navigate it and this coming week we’ll explore the state of the economy. Luckily next week has minimal updates schedules in terms of data releases, so we can focus on analysis.

With that I wish you a very good day,

Leonid

Notes:

Shanghai Composite Index (SHCOMP): Tracks all stocks (A and B shares) traded on the Shanghai Stock Exchange.

CSI 300 Index (SHSZ300): Represents the top 300 stocks traded on the Shanghai and Shenzhen Stock Exchanges.

China A50 Index (512150 CH): Comprises the top 50 A-share companies listed on the Shanghai and Shenzhen Stock Exchanges.

ChiNext Price Index (159954 CH): Focuses on innovative and high-growth enterprises listed on the Shenzhen Stock Exchange.

SSE STAR 50 Index (83151 HK): Represents the top 50 companies listed on the Shanghai Stock Exchange’s STAR Market, emphasising science and technology innovation.

Hang Seng Index (HSI): Measures the performance of the largest companies listed on the Hong Kong Stock Exchange.

Hang Seng China Enterprises Index (2828 HK): Includes major H-share companies listed in Hong Kong.

Currency Considerations:

Chinese Indices (SSEC, CSI300, China A50, CNT, STAR50): These indices are denominated in Chinese Yuan (CNY). To present their performance in USD terms, currency exchange rate fluctuations between the CNY and USD have been considered.

Hong Kong Indices (HSI, HSCEI): Denominated in Hong Kong Dollars (HKD). Their performance in USD terms reflects the HKD/USD exchange rate stability, as the HKD is pegged to the USD.