China Weekly Wrap: Markets, Macro & Tech – Key Developments This Week

a week that was 15-20 June 2025

Good morning,

We are coming to you live from the wonderfully colourful Port of Spain, in Trinidad where we are engaged I some client work on the O&G side. This does not slow down the rest of the Panda Activities though. We were back in publishing mode this week with two new pieces one son Asia Energy, the other taking the pulse of China’s domestic recovery in the shape of Macau Casinos.

First up, our Asian Energy Sector Update unpacked Brent oil scenarios, regional dividend champions, and why Asia’s role in the global repricing cycle is still underappreciated. It’s a timely reset for energy bulls, income investors, and anyone trying to make sense of OPEC+ meets Fed meets China macro.

Meanwhile, in our China Casino Watchlist, we revisited Macau with a critical lens. Against a choppy recovery and renewed competitive intensity, we flagged which operators offer the right mix of capital return, license security, and China-aligned positioning—and which are better left to the high rollers.

Check all of them out if you haven’t already and do sign up to the blog for the paywalled section - we’d love to have you!

Next week we’ll begin tackling the healthcare sector. We’re not quite sure what shape the output will be but we’re thinking retail producer and hospital in separate notes. It’s a new sector for us, but one we believe is very important to have a handle on.

Serious about investing in Asia? Then your process needs more Panda.

We get it, for some readers, a Substack alone isn’t enough. If you’re looking for sharper insights, personalised feedback, or just someone to help you cut through the noise in China and Asia, we also offer bespoke research calls and strategy sessions.

Right now, we’re working with clients on China’s consumer landscape, the 2Q25 macro outlook, and yes robotics.

See what we offer here, and connect with us today or message us directly.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

📊 Weekly Relative Performance Observations

Week of June 15–21, 2025

Broad Takeaway

Chinese equities fell across the board this week, led by weakness in growth indices and a clear loss of momentum in Hong Kong. The CSI 300 and Shanghai Composite both dipped ~0.5%, while the Hang Seng Index dropped -1.52%—its worst showing in over a month. There was no major policy trigger, but foreign appetite faded amid global central bank noise and pre-summer positioning.

Meanwhile, Taiwan continued its AI-led rally, and India rebounded sharply. China’s markets remained directionless—neither oversold nor fundamentally bullish, but increasingly adrift in a global market rotating around tech, oil, and central bank messaging.

🇨🇳 Performance in Chinese Equities

Shanghai Composite (SHCOMP): 3,359.90, -0.51%

The index slid quietly as banks, industrials, and SOEs softened. There’s little conviction in either direction—traders are watching policy but not reacting. Volume was light, and dispersion remains high.

CSI 300 (SHSZ300): 3,846.64, -0.45%

Large-cap A-shares lost ground in choppy trade. Financials and materials faded modestly, with few signs of institutional accumulation. PBOC liquidity signals were a non-event for equity bulls.

ChiNext Index: 2,009.89, -1.66%

Growth names came under pressure, particularly in biotech and unprofitable automation. ChiNext continues to trade like a sentiment barometer for domestic retail—and right now, that sentiment is soft.

🇭🇰 Performance in Hong Kong Equities

Hang Seng Index (HSI): 23,530.48, -1.52%

Broad retreat as tech, property, and China consumer names all rolled over. Turnover remained decent, but southbound inflows slowed. Still up +17.4% YTD, but this week’s pullback suggests consolidation is underway.

HSCEI (China Enterprises Index): 8,527.07, -1.48%

SOEs and insurers couldn’t hold the line as mainland investor sentiment dimmed. While still a popular macro proxy, the HSCEI is struggling to find new buyers after its strong May run.

HS Tech Index: 5,133.14, -2.03%

Internet names led the decline. Meituan, JD, and Tencent were all weak, with little offset from hardware or EVs. Investors trimmed risk amid renewed scrutiny of valuation versus growth expectations.

HS Red Chips: 4,024.06, -2.30%

Infrastructure names and quasi-SOEs were hit hard by rotational outflows. After several weeks of gains, profit-taking and FX weakness drove the unwind.

VHSI (Volatility Index): 21.45, +8.06%

Volatility spiked meaningfully as traders hedged downside risk ahead of summer policy events. Leverage remains modest, but risk appetite is visibly cooling.

🌏 Regional Peers – Weekly Performance

🇹🇼 FTSE TWSE Taiwan 50: +0.84%

TSMC and semiconductors remained bid, but gains were narrower. AI demand is still powering the market, yet signs of positioning fatigue are emerging. Still, Taiwan retains strong YTD leadership.

🇰🇷 KOSPI Composite: +1.5%

Memory stocks extended gains, helping offset weakness in domestic consumer plays. Won stability aided exporters, and Korea is emerging as a quiet AI beneficiary alongside Taiwan.

🇯🇵 TOPIX: +0.54%

Japanese equities bounced modestly as BoJ stood pat. Yen volatility remains a concern, but exporters and industrials saw some relief. Equity inflows stabilized after recent outflows.

🇮🇳 NIFTY 50: +1.59%

Strong rebound as investors reassessed post-election risks. Banks and PSUs were back in favor, and budget expectations are now lifting sentiment. India was one of Asia’s best performers this week.

🇮🇩 FTSE Indonesia: +0.3%

Sideways trade continued. Banks were steady; miners lagged. Political transition and fiscal messaging are in focus. The market is digesting May’s rally but not correcting sharply.

🇹🇷 BIST 100 (Turkey): -1.34%

A second straight week of outflows. FX and rate volatility weighed on banks and cyclical names. Macro noise remains the dominant driver.

🇸🇬 MSCI Singapore: +0.08%

Flat week, with REITs and defensives ticking higher. The market remains tightly correlated to regional rate expectations, not domestic fundamentals.

🇦🇺 ASX 200: +0.3%

Materials struggled, but banks and consumer staples held up. The market appears range-bound, awaiting catalysts from China or commodity data.

💡 Takeaways for Chinese Equities in a Regional Context

China’s equity lull deepens

No major selling, but no buying either. The lack of positive catalysts is wearing on sentiment. Investors are increasingly trading China tactically—hedging exposure, waiting on policy.

Hong Kong reverses, but isn’t broken

After strong YTD gains, the HSI’s pullback looks orderly. Profit-taking and sector rotation are healthy signs, but sentiment will need a fresh spark to resume the rally.

Asia’s story is diverging

Tech-heavy markets (Taiwan, Korea) are surging; macro-reliant ones (China, Japan) are treading water. Meanwhile, political noise (India, Turkey) continues to create volatility. China’s in the middle: steady but uninspiring.

Positioning now reflects summer caution

Across Asia, volume is thinning, and dispersion is rising. Investors are managing risk, not chasing return. For China, this means more of the same: low conviction, modest volatility, and a wait for second-half catalysts.

📰 In the News This Week

🇨🇳 Xi Proposes Peace Plan for the Middle East

Announced by: President Xi Jinping | Date: June 19, 2025

President Xi outlined four proposals to address the Middle East conflict: ceasefire, protection of civilians, dialogue, and international cooperation.

This Indicates:

A soft-power play that positions China as a diplomatic stabilizer in geopolitically sensitive regions. While indirect, it supports Beijing’s energy diplomacy and neutral global posture.

🏛 NPC Standing Committee Meeting Scheduled for June 24–27

Announced by: China State Media | Date: June 16, 2025

Beijing will convene the NPC Standing Committee from June 24–27. While the agenda is not public, prior meetings have been tied to key economic or fiscal policy announcements.

This Indicates:

Potential near-term policy catalysts—ranging from stimulus to regulatory reform—could emerge. Markets will watch closely for any signals on housing, local government debt, or consumer support.

🛒 Beijing Extends ¥138B Consumer Trade-In Subsidies

Announced by: Ministry of Commerce | Date: June 19, 2025

China confirmed that appliance and electronics trade-in subsidies will continue in H2, backed by ¥138 billion in central funding.

This Indicates:

Targeted stimulus aimed at reviving household spending and manufacturing volumes. Beneficiaries likely include white goods OEMs, retailers, and last-mile logistics.

🇺🇸 Next Round of U.S.–China Trade Talks Expected in July

Announced by: U.S. Treasury Secretary Scott Bessent | Date: June 18, 2025

Bessent confirmed plans for renewed trade talks in ~three weeks, following earlier agreements to ease export curbs and boost bilateral flows.

This Indicates:

Ongoing normalization of U.S.–China trade relations, albeit gradual. Encouraging for sentiment in agriculture, tech components, and RMB stability.

🏘 Guangzhou Fully Lifts Property Restrictions

Announced by: Guangzhou Municipal Government | Date: June 13, 2025

The city scrapped all limits on purchases, sales, and pricing of housing, alongside mortgage rate/downgrade easing and a ¥100B urban renewal fund.

This Indicates:

The most aggressive local housing easing to date. Likely to influence national property sentiment, developer share prices, and Tier-1 land markets.

💹 Tencent and Alibaba Explore A-Share Listings

Announced by: NetEase / UBM Finance | Date: June 16, 2025

Tencent, Alibaba, Xiaomi, and Meituan may list domestically, with Tencent reportedly leading the effort to return to A-shares.

This Indicates:

A push for capital market “repatriation.” Symbolically and practically important—likely to boost STAR/ChiNext liquidity and sentiment toward platform companies.

🚗 China’s EV Makers Target 100% Domestic Chips by 2026

Announced by: MIIT & Domestic Automakers | Date: June 17, 2025

Major Chinese carmakers unveiled plans to launch vehicles using fully domestically produced chips, with production starting in 2026.

This Indicates:

Rising momentum behind China’s semiconductor independence. Bullish for local chipmakers and vertically integrated EV platforms.

💼 Qi Bin Champions Hong Kong’s Financial Revitalization

Announced by: Chinese Liaison Office in Hong Kong | Date: June 20, 2025

Former Goldman banker Qi Bin has led a series of reforms and engagements to boost Hong Kong’s capital markets and cross-border connectivity.

This Indicates:

Strong policy backing for Hong Kong’s financial sector. Should help reinforce confidence in HKEX and support valuation recovery in financial services.

📈 The Week in Macro Data

It was a busy data week in China, headlined by stronger-than-expected May retail sales, a mixed industrial and trade print, and no change to policy rates. The macro tone is cautiously constructive: consumer demand surprised to the upside, while FAI and PPI hinted at lingering weakness. Forward momentum remains uneven—but not stalled.

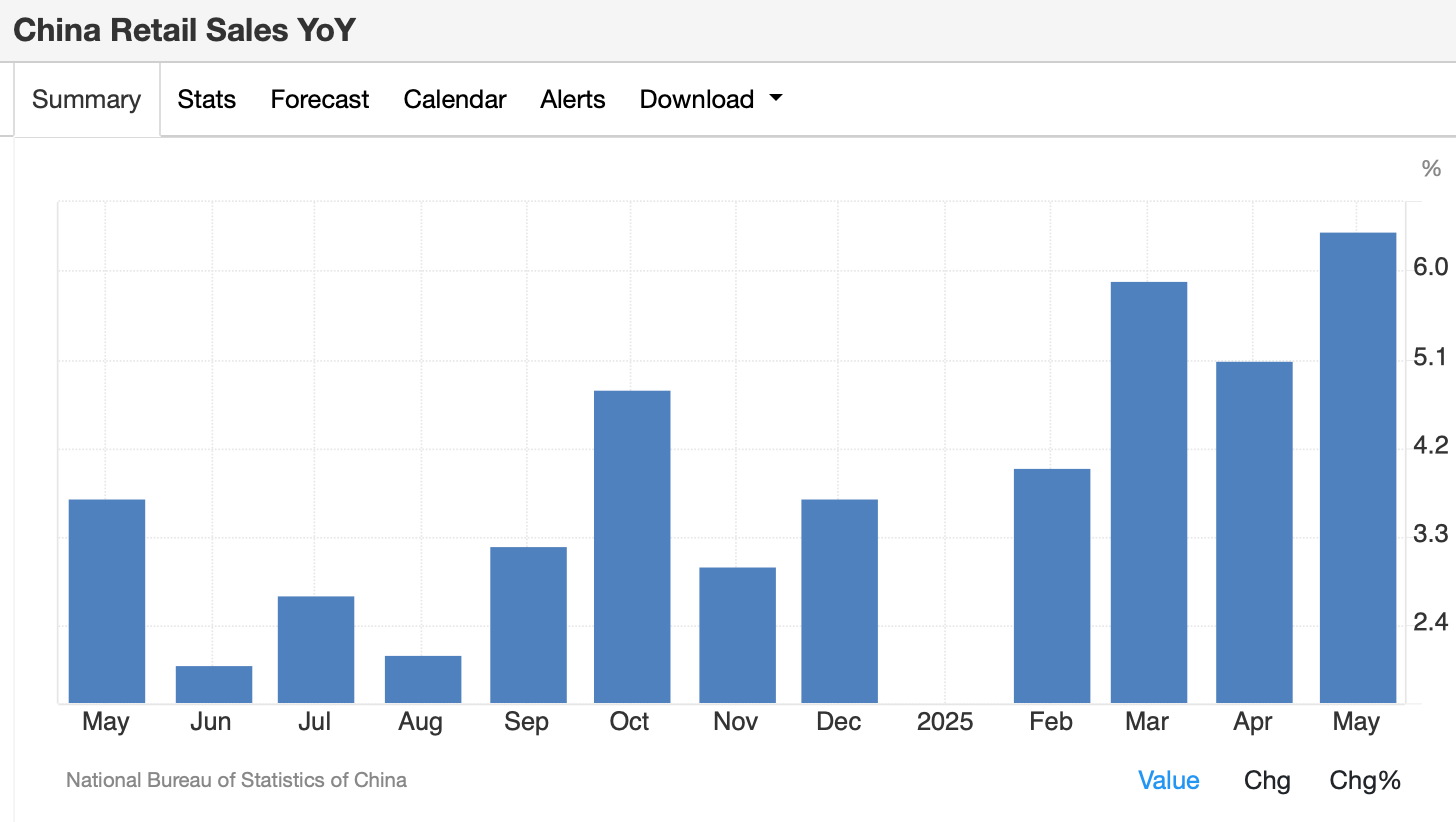

Retail Sales (May)

Actual: +6.4% y/y | Consensus: +5.0% | Previous: +5.1%

Online retail sales: +11.5% y/y to RMB 1.3 trillion

This Indicates:

A strong upside surprise and the clearest sign yet that Chinese consumption is stabilizing. Categories like electronics, food service, and apparel rebounded, while e-commerce continued to outperform. The scale of the online recovery is especially important for sentiment toward platform names.

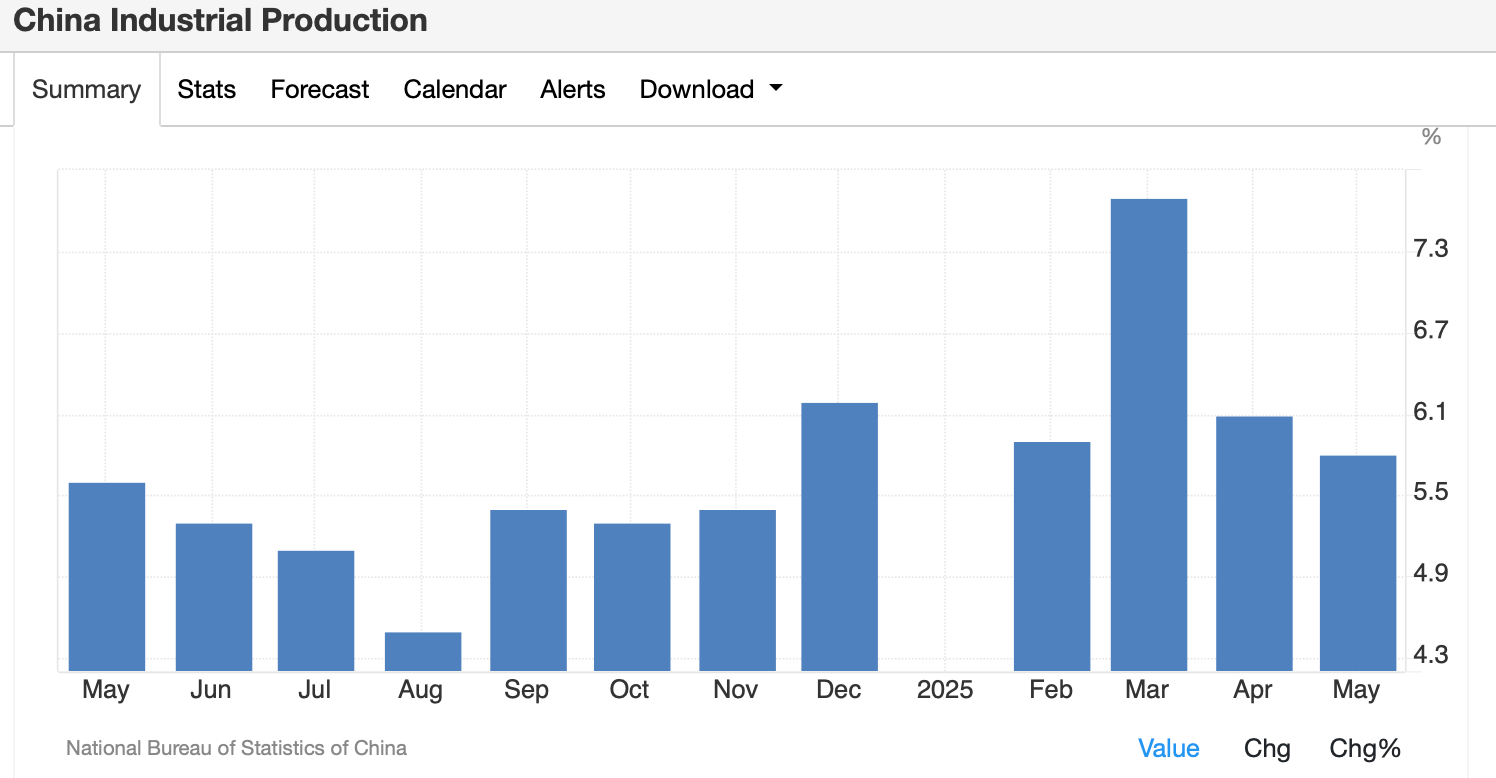

Industrial Production (May)

Actual: +5.8% y/y | Consensus: +5.9% | Previous: +6.1%

MoM: +0.61%

This Indicates:

Slight miss vs. consensus, but industrial momentum remains decent. Key segments showed divergence:

Automobiles: +11.3% y/y

NEVs: +31.7% y/y

Steel: +3.4%

Cement: -8.1% y/y

Refining: -1.8%

The data highlight strength in final assembly and electrified transport, but weakness in traditional materials and upstream energy demand.

Fixed Asset Investment (Jan–May YTD)

Actual: +3.7% y/y | Consensus: +3.9% | Previous: +4.0%

This Indicates:

Capital formation is losing steam. Government-backed infrastructure remains active, but private manufacturing and property-related investment continue to underwhelm. A reacceleration will likely require policy support or further credit easing.

Urban Surveyed Unemployment Rate (May)

Actual: 5.0% | Consensus: 5.1% | Previous: 5.1%

Youth Unemployment (ex-students): 14.9% (down from 16.5%)

This Indicates:

Marginal improvement, but labor market tightness remains elusive. Youth unemployment—while down—remains high, especially when broader demographic categories are included. Gains may reflect seasonal effects more than structural change.

Loan Prime Rates (June)

1-Year LPR: 3.00% (unchanged)

5-Year LPR: 3.50% (unchanged)

This Indicates:

No rate cuts from the PBOC, reflecting a desire to preserve banking margins and avoid RMB pressure. With inflation still subdued, markets were hoping for more dovish guidance—but Beijing appears to be signaling “wait and see.”

Foreign Direct Investment (YTD through May)

Actual: -13.2% y/y | Previous: -10.9% | Consensus: -9.5%

This Indicates:

A further deterioration in inbound FDI, highlighting global investor caution around China’s structural and geopolitical risk. Persistent outflows in tech, real estate, and manufacturing undermine hopes of a near-term capital reversal.

Complete Index Performance List:

🧭 General Trends

Chinese equities delivered a mixed and rotational week. Onshore markets trended modestly lower amid a lack of macro catalysts, while Hong Kong saw gains concentrated in defensives, state-owned enterprises, and property. Tech and small-cap names, previously in the lead, took a breather as volatility crept higher.

Investor tone remains tactically constructive but far from euphoric. Macro data reinforced a picture of patchy recovery—weakness in exports, credit, and inflation offset by pockets of industrial strength and policy signals. Sector rotation, not fresh inflows, continues to define price action.

📉 Mainland Indices: Flat Week, Commodities Shine

Shanghai Composite (SSE): -0.51%

CSI 300: -0.45%

ChiNext: -1.66%

Shenzhen 100: -0.82%

SSE SME Innovation: -1.93%

SSE Commodity Equity Index: -1.82%

SSE Conglomerate Index: +1.40% (best performer)

SSE Dividend Index: +0.24%

Interpretation:

Mainland markets saw a subdued week with breadth weakening. Innovation indices underperformed sharply as biotech and automation plays lost momentum. The ChiNext gave back recent gains, with AI and small-cap industrial software names hit hardest. In contrast, conglomerates and SOE-linked names held firm, buoyed by rotation and stabilizing sentiment around oil services and industrial cyclicals.

📈 Offshore Indices: Defensive Rotation in Charge

Hang Seng Index (HSI): -1.52%

HS Tech: -2.03%

HSCEI (China Enterprises): -1.48%

HSI Financials: -0.28%

HSI Property: -1.32%

HSI Industrials: -2.20%

VHSI (Volatility): -8.06% (decline in vol)

Interpretation:

Hong Kong indices saw modest pullbacks but under the surface, capital rotated meaningfully. Defensive names including life insurers, telcos, and landlords outperformed. In contrast, high-multiple tech stocks, biotech, and consumer discretionary were sold off. The drop in the volatility index suggests fading fear, but the tone was clearly more selective and risk-averse.

🔍 Macro Takeaways

EV Credit Risk Eased: MIIT reaffirmed the 60-day payment reform for auto suppliers, easing upstream credit stress and tightening working capital cycles.

AI Sovereignty Push: China released its first domestic AI chip design software (“QiMeng”), boosting sentiment in niche AI and EDA plays.

U.S.–China Diplomatic Chatter: A thaw was hinted at in rare-earth and trade dialogue, though with little immediate market impact.

Mixed Macro Data: May’s CPI and PPI both came in soft, with exports slowing and aggregate financing missing expectations. The recovery remains fragile and policy-dependent.

Conclusion:

Markets remain structurally long but tactically cautious. Participation is narrow, and upside conviction is limited without a new macro or liquidity impulse.

🧪 Sector & Style Trends

🚗 EVs & Autos: Structurally Sound, but Profit-Taking Hits

BYD Co. (1211.HK): -4.04%

Geely Auto (0175.HK): -0.98%

Xiaomi-W (1810.HK): +4.04%

Li Auto-W (2015.HK): -7.10%

Comment:

The sector saw structural positives via MIIT reforms, but the market narrative was dominated by de-risking. Geely and Li Auto both sold off heavily despite improving fundamentals. BYD also traded lower on volume concerns. Xiaomi held up better, benefiting from diversified tech exposure.

💊 Biotech & Healthcare: Rally Falters as Profit-Taking Hits

Wuxi Bio (2269.HK): -13.93%

Hansoh Pharma (3692.HK): -4.62%

Sino Biopharm (1177.HK): -9.76%

Ali Health (0241.HK): -5.87%

Comment:

Biotech leaders gave back much of the prior two weeks’ gains. Institutional flows appear to have rotated out, particularly in CROs and generic pharma names. The correction was orderly but signals a shift toward more defensive positioning.

🏦 Financials & SOEs: Quiet Bid for Safety

China Life (2628.HK): +3.80%

Ping An (2318.HK): +0.82%

ICBC (1398.HK): +1.64%

China Mobile (0941.HK): -1.18%

Comment:

Life insurers were steady performers this week, with yield-curve stability and low regulatory noise helping drive flows. Banks traded sideways, while telcos softened slightly. Overall, SOEs continue to benefit from “policy safety” and muted earnings volatility.

🏘 Property & REITs: Stable, Not Spectacular

China Resources Mixc (1209.HK): -4.68%

Henderson Land (0012.HK): +5.25%

China Overseas (0688.HK): -3.60%

HSI Property Index: -1.32%

Comment:

Property saw a sector-wide breather, despite recent policy support. Some names like Henderson rebounded, but China Overseas and Mixc saw selling pressure. The optimism over mortgage loosening is being tempered by investor caution around sales volumes and refinancing conditions.

🥤 Consumer & Staples: Nongfu Stands Out, Rest Weak

Nongfu Spring (9633.HK): +2.04%

Haidilao (6862.HK): -2.55%

CR Beer (0291.HK): -3.61%

Tingyi (0322.HK): -2.04%

Comment:

The F&B sector saw bifurcation. Nongfu Spring continued to attract flows on defensive fundamentals and strong pricing power, while Haidilao and CR Beer struggled amid signs of softening discretionary spend and rising input costs.

📢 Company News & Results (June 14–21, 2025)

Regencell Bioscience Holdings (RGC)

Announced: June 13, 2025

Details: Executed a 38-for-1 stock split, causing the share price to surge over 4x on the first day, and logged a stunning ~60,000% YTD rally in its U.S. listings—despite reporting no revenue and multi-year losses totaling ~$10 m .

Implications: A retail-fueled meme stock surge driven by split mechanics and limited free float. However, without revenue, regulatory backing, or institutional support, sustainability is highly questionable.

Xiaomi (1810.HK)

Announced: June 18, 2025

Details: CEO Lei Jun revealed on Weibo that the company will start taking orders for the YU7 electric SUV at the end of June, ahead of the prior July launch schedule .

Implications: This marks a significant step in Xiaomi’s expansion into EVs, accelerating its product roadmap and challenging competitors in the mid-tier EV ecosystem.

MTR Corporation (00066.HK)

Announced: June 17, 2025

Details: Issued its inaugural USD 3 bn subordinated perpetual bonds — two tranches (5.5-year non-call at 4.875% and 10.5-year non-call at 5.625%) .

Implications: The record Asia ex-Japan debut signals strong investor trust, enhancing MTR’s capital structure and flexibility — critical as property-related revenues remain under pressure.

Cheetah Mobile (CM CMOBILE)

Announced: June 19, 2025

Details: Posted a Q1 operating loss of RMB 14.3 m, narrowing sharply from RMB 66.4 m a year ago. Revenue reached RMB 34.1 m .

Implications: While still unprofitable, the swift contraction in losses reflects successful cost rationalization. A continued trajectory toward break-even could rebuild investor confidence.

17 Education & Technology Group (YQ:US)

Announced: June 17, 2025

Details: Q1 revenue dropped 15% YoY to RMB 21.7 m; gross margin declined to 43%; net loss narrowed to RMB 30.9 m from RMB 46.2 m YoY .

Implications: Signals ongoing regulatory and demand pressures. Progress in transitioning to public-school SaaS is notable, but sustainable growth remains distant.

China Traditional Chinese Medicine Holdings (0570.HK)

Announced: June 20, 2025

Details: Introduced several independent non-executive directors and updated audit, nomination, and strategy committee compositions .

Implications: Corporate governance overhaul likely preludes strategic changes—possibly M&A, restructuring, or capital reallocation. Operational implications remain speculative.

FTSE China Index Rebalancing

Announced: June 18, 2025

Details:

Pop Mart added to both FTSE China 50 and FTSE A50

Bank of Jiangsu also added to FTSE A50; Great Wall Motor and China Merchants Securities removed .

Implications: Inclusion should trigger passive inflows and improved liquidity for Pop Mart, consolidating gains from its collectibles-to-lifestyle pivot.

Bottom Line: A Constructive, Cautious Reset

Onshore Drifts, Offshore Rotates — A Week of Tactical Positioning

This week marked a cooling of momentum across Chinese equity markets, with onshore indices turning mildly negative and offshore benchmarks continuing a slow grind higher. The Shanghai Composite fell –0.51%, the CSI 300 –0.45%, and ChiNext –1.66%, as investors pulled back from growth and innovation plays after a two-week rally. In contrast, Hong Kong equities rose, with the Hang Seng Index +1.26%, supported by a visible rotation into SOEs, insurers, and property stocks. Defensive positioning came into focus, and flows remained present—but less directional.

Volatility eased, with the VHSI down ~8%, a sign that investors weren’t panicking, but were rebalancing. The mood: engaged, but not exuberant. Flows favored names with policy support, balance sheet visibility, or index inclusion catalysts—not speculative upside.

Policy Support Continues, But the Catalyst Clock Ticks

Four major developments shaped sentiment:

Auto supply chain reform: More than a dozen Chinese automakers pledged to pay suppliers within 60 days, backed by MIIT. This is more than good optics—it’s a real step toward liquidity restoration across an industry under margin pressure.

AI chip design sovereignty: The release of QiMeng, China’s domestically-developed AI-assisted chip design software, signals strategic independence from U.S. EDA tools. While early in rollout, this aligns with China’s larger industrial autonomy agenda.

Huawei’s dual signal: The tech giant launched its Pura 80 smartphone line, underscoring its premium consumer hardware push, but was also hit by new U.S. export caps on advanced AI chip production, showing that geopolitical ceilings remain.

U.S.–China trade thaw: Talks in London and Geneva yielded modest concessions—China will resume rare earth exports and allow certain U.S. agri-imports. But the U.S. didn’t budge on tariffs. The détente is real, but limited.

None of these were game-changers—but together, they offered reassurance that policy is nudging in the right direction. Yet, without broader stimulus or stronger consumer data, investor conviction stayed cautious.

Sector Summary: Rotation, Not Expansion

Winners this week were largely from defensive and policy-linked corners:

China Life +3.8%, CCB +1.6%: Financials absorbed flows as bond yields stabilized and macro risk faded.

Henderson Land +5.3%, China Overseas +5.8%: Quality property names saw sustained bids on the back of incremental mortgage easing and new urban renewal signals.

Nongfu Spring +2.0%: Staples held up well, as investors looked for predictable earnings and margin stability.

On the other end, prior momentum plays corrected:

Li Auto –7.1%, Geely –9.0%: Despite structural support, autos sold off on profit-taking and weak technicals.

Wuxi Bio –5.4%, Sino Biopharm –3.8%: Biotech gave back recent gains, suggesting that the institutional rotation has limits without policy acceleration.

Meituan –2.5%: Tech darlings continued to drift, reflecting valuation fatigue and muted consumer data.

Conclusion: The rotation was not about fear, but about safety and yield. Investors aren’t de-risking, but they’re clearly positioning more tactically—especially ahead of mid-year policy and economic readouts.

Corporate Moves: Under-the-Radar Signals of Strategy

Several companies made moves worth watching:

Xiaomi began early order-taking for its YU7 EV, accelerating its automotive rollout timeline. While not market-moving yet, this confirms Xiaomi’s serious long-term EV commitment.

MTR (Hong Kong rail operator) raised US$3bn in perpetual bonds, showing strong institutional appetite for defensive infrastructure and cash flow-rich names in a jittery market.

Pop Mart (9992.HK) had a standout week: it entered FTSE indices and opened its first Popop jewellery concept store in Shanghai. Brand monetization is expanding beyond blind boxes into lifestyle.

Huawei’s smartphone launch and chip cap combination offered a microcosm of China’s tech sector: technologically ambitious, commercially resilient, but still geopolitically boxed in.

Regencell Bioscience (RGC) in the U.S. soared 400% on meme-like activity, despite no revenues. While not China-based, the move shows speculative sentiment isn’t dead—it’s just shifting sectors.

Macro Data: Still Soft, But No Alarms

Last week’s macro prints painted a familiar picture:

CPI YoY was flat at –0.1%, indicating no worsening of deflation, but no meaningful rebound in consumer pricing power either.

PPI YoY –3.3%, the worst reading in 6 months, with industrial margins still under strain.

Imports –3.4% YoY: Capex and manufacturing restocking remain weak.

New credit rebounded month-on-month, but household loan growth stayed sluggish.

The bright spot: Vehicle sales up 11.2% YoY, offering hope that big-ticket consumption is more resilient than sentiment suggests.

This was a week of recalibration, not risk aversion. The Hang Seng’s quiet climb masks a deep rotation underway: tech is out, SOEs and yield are in. Investors remain plugged in—but selective. They’re rewarding dividend payers, policy-aligned sectors, and brand-consistent stories like Pop Mart or Nongfu, not chasing beta.

Without decisive policy action or a consumer spending breakout, the rally is more tactical than transformational. But importantly: there is no rush for the exits. That alone marks progress versus early 2025.

Final Thought

This wasn’t a week of conviction, but it was a week of clarity.

Capital is flowing toward what works—state visibility, yield security, and strategic themes—but not venturing much beyond that. The speculative fever has cooled, but the market is stable. The foundation is firming, sector leadership is rotating, and volatility is falling. But the next leg higher still requires a spark: whether macro or policy.

Until then, we’re in a positioning market, not a trending one.

Regards,

Leonid