China Weekly Wrap: Markets, Macro & Tech - Key Developments This Week

The week of 6-11 October

Good rainy HK afternoon,

WE’re back after taking the golden week off, and we’re back to fun stuff like the resumption of trade threats via truth social posts. In fact we’ve delayed this weeks update to see if there was any more clarity at all on the subject. We’re covering it in the news section.

Check out the portfolio review if you haven’t already - only available to full subscribers. Anticipate changes this coming week.

NOTE: Panda+ is now closed to new joiners. We thank everyone for their interest and custom.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

📊 Weekly Relative Performance Observations

Week of October 6–10, 2025

📉 Broad Takeaway

Asia ended the week mixed, with Japan (+2.2%) and Korea (+1.7%) leading on renewed global risk appetite, while Hong Kong (-3.1%) lagged sharply amid renewed tech and property weakness. Mainland China was relatively stable (CSI 300 -0.5%, SSE +0.4%) as large-cap defensives offset ChiNext’s deeper decline. The week underscored the divergence between resilient onshore A-shares and fragile offshore sentiment.

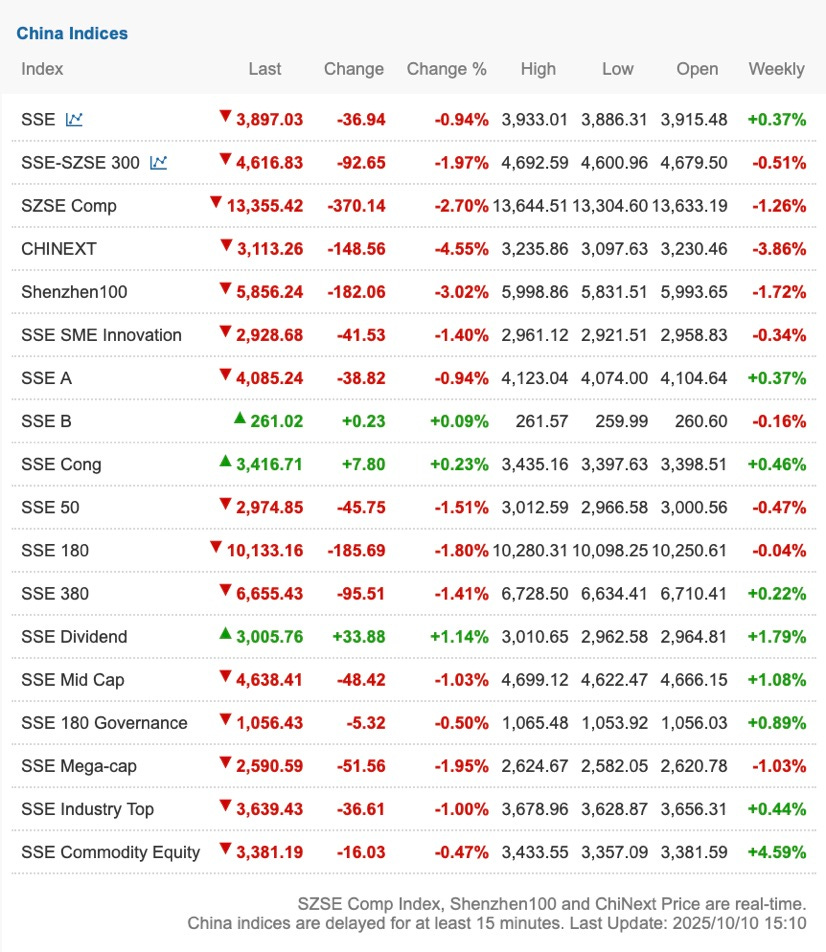

🇨🇳 Performance in Chinese Equities

Shanghai Composite (SSE): +0.37% – Steady, supported by dividend and commodity-linked names.

CSI 300: -0.51% – Large caps soft, with financials and consumer staples mixed.

SZSE Composite: -1.26% – Broader market drifted lower.

ChiNext Index: -3.86% – Sharp selloff in growth/innovation.

Shenzhen 100: -1.72% – Tech-heavy exposure continued to correct.

SSE SME Innovation: -0.34% – Mid-cap innovation names weak.

SSE 50 / SSE 180: -0.47% / -0.04% – Flat to mildly negative.

SSE Mid Cap: +1.08% – Small rebound driven by industrials.

SSE Mega-cap: -1.03% – Heavyweights corrected slightly.

SSE Commodity Equity: +4.59% – Strongest gainer on metals and oil rally.

SSE Dividend: +1.79% – Defensives attracted rotation.

📌 Takeaway: Onshore sentiment held up despite offshore volatility. Growth segments (ChiNext -3.9%) slumped, while commodity-linked and dividend sectors gained. This rotation toward cyclicals and high-yield names reflects positioning for policy continuity and rising geopolitical hedging demand in resources.

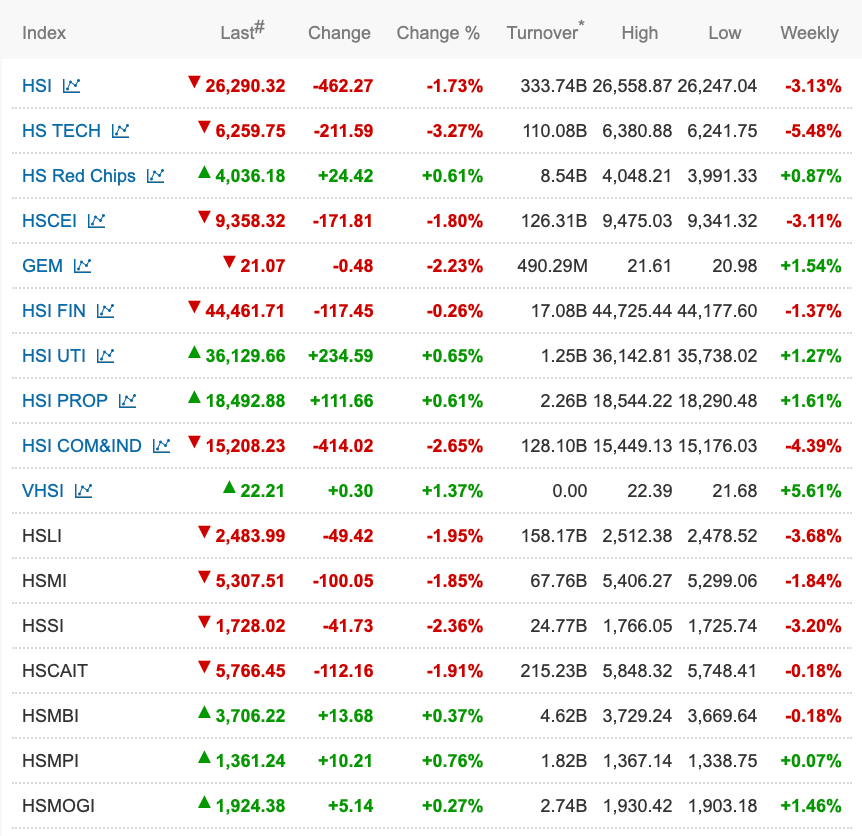

🇭🇰 Performance in Hong Kong Equities

Hang Seng Index (HSI): -3.13% – Broad weakness across sectors.

Hang Seng Tech (HSTECH): -5.48% – Steepest drop as internet and EVs corrected.

HS Red Chips: +0.87% – Rare bright spot, supported by select SOEs.

HSCEI: -3.11% – Mainland financials and property weighed.

GEM: +1.54% – Small-cap innovation rebound.

HSI Finance: -1.37% – Banks soft on weak loan growth data.

HSI Utilities: +1.27% – Defensive bid reappeared.

HSI Property: +1.61% – Mild rebound after prior heavy losses.

HSI Commerce & Industry: -4.39% – Consumer and cyclical names lagged.

VHSI: +5.61% – Volatility rose, reflecting risk aversion.

📌 Takeaway: Offshore China faced broad risk-off pressure. The Hang Seng Tech Index’s -5.5% drop erased much of September’s rebound, led by platform and EV weakness. Red Chips and utilities were isolated gainers. The volatility spike (VHSI +5.6%) suggests hedging activity picked up ahead of U.S. CPI and earnings season.

🌏 Regional Peers – Weekly Performance

🇯🇵 Japan (TOPIX: +2.19%)

Japan outperformed again as foreign inflows into buyback and corporate governance themes remained steady. The rally was broad-based — autos, banks, and industrials all gained — but notably defensives (utilities, railways, insurance) joined the move higher, signalling that investors are treating Japan as Asia’s “quality compounder” allocation rather than a cyclical trade. The yen firmed slightly, but the absence of fresh BoJ tightening talk allowed exporters to sustain momentum. The ongoing buyback cycle — now topping ¥10 trillion YTD — continues to attract global institutions. The key swing factor remains FX volatility: further yen strength could cap exporter margins, but structural reform and governance tailwinds are now deeply entrenched in foreign portfolio strategies.

🇰🇷 Korea (KOSPI: +1.73%)

Semiconductors once again led Korea higher, extending a two-week recovery on renewed optimism around Nvidia’s upcoming Q4 product cycle and signs of DRAM price stabilization. Foreigners were net buyers of Samsung and SK Hynix, while autos and battery names also firmed. However, domestic consumer and internet plays lagged, reflecting a narrow, tech-led market. The KOSPI remains a tactical proxy for AI hardware sentiment — volatility is high, but global allocators continue to re-enter Korea when valuations dip below 10x forward earnings. Positioning has turned modestly net long, though without conviction beyond semiconductors.

🇹🇼 Taiwan (FTSE TWSE Taiwan 50: -0.47%)

Taiwan paused after months of strong AI-driven gains. TSMC and Hon Hai (Foxconn) traded sideways, as investors trimmed exposure after a heavy summer rally. Domestic flows were solid but foreigners took profits, rotating some capital into Korea and Japan. The broader tech complex showed fatigue — AI hardware remains a structural story, but positioning is now crowded, and valuation multiples (TSMC >19x forward P/E) leave limited upside unless U.S. tech continues to rally. The near-term risk is that U.S. yields rise again, triggering de-rating pressure. Taiwan remains a core structural overweight for AI, but increasingly a tactical trim for global PMs seeking diversification.

🇮🇳 India (NIFTY 50: +1.57%)

India rebounded modestly after last week’s -2.7% decline. Banks and autos drove the recovery, while IT services were mixed ahead of Q3 earnings. Domestic mutual fund inflows remained strong, supporting price resilience even as foreign investors stayed net sellers for a third consecutive week. The valuation premium (21x forward P/E) continues to deter new foreign allocations, particularly as China/Hong Kong trade at one-third those multiples. Strategically, India remains the “steady growth anchor” in Asia, but the trade is crowded and momentum-driven, not value-based. Near-term, India benefits from local liquidity, but it risks rotation pressure if EM investors rebalance toward cheaper North Asia equities.

🇹🇷 Turkey (BIST 100: -1.22%)

The BIST corrected after a volatile +8.6% rally in late September. The pullback reflects profit-taking by local retail investors and a pause in FX-hedge-driven flows. Foreign participation remains minimal, leaving the market highly speculative and momentum-sensitive. Inflation remains above 60%, keeping macro hedging appeal alive, but policy credibility limits long-term foreign re-entry. The BIST remains a high-beta macro hedge, not a structural EM story.

🇸🇬 Singapore (MSCI Singapore: -0.36%)

Singapore traded softly, dragged by REITs and property developers amid U.S. rate volatility. Banks offered resilience, with solid loan growth offsetting funding cost pressures. The city-state continues to play its role as Asia’s portfolio stabilizer — low beta, high yield, and political stability. However, the absence of a clear growth driver (no tech, no resources, no large domestic consumption base) means Singapore remains defensive ballast, not a tactical overweight.

🇮🇩 Indonesia (FTSE Indonesia: 0.00%)

Indonesia consolidated after a strong September run. Energy and metals exporters held firm, but foreign inflows paused, reflecting full positioning after heavy Q3 buying. Bank earnings remained solid, but valuations are stretched relative to peers. Indonesia retains strong structural support from commodity exports and fiscal discipline, yet near-term catalysts are lacking. Investors are waiting for fresh resource price momentum or pre-election clarity before re-engaging.

🇵🇭 Philippines (PSEi: -0.61%)

The Philippines slipped as inflation re-accelerated, dampening consumption sentiment. The central bank’s hawkish tone weighed on property and retail sectors. With foreign ownership already low, downside was contained, but liquidity remains thin, keeping volatility high. The market continues to trade as a macro levered consumption play, vulnerable to inflation surprises and external funding conditions.

🇦🇺 Australia (ASX 200: -0.04%)

Australia was flat as miners gained on stronger iron ore and copper prices, offset by weakness in defensives and housing-related names. The RBA’s hawkish tone and sticky inflation capped upside. The ASX continues to trade as a geared bet on China’s infrastructure/property policy, with local fundamentals secondary. Investors remain tactically long resources but underweight financials.

💡 Strategic Takeaways

1. Onshore Rotation: Investors shifted toward dividend and commodity-linked plays, signaling cautious positioning for steady policy support and geopolitical risk hedging.

2. Offshore Capitulation: HSTECH’s -5.5% weekly loss shows fragile sentiment despite low valuations; institutional patience is wearing thin.

3. Regional Leadership: Japan and Korea’s outperformance reflects strong foreign inflows and structural themes — buybacks, semis, and corporate reform.

4. Re-emerging Volatility: VHSI jumped +5.6%, breaking a multi-week compression trend, suggesting renewed hedging ahead of key U.S. macro prints.

5. Strategic Positioning: The divergence between resilient onshore and weak offshore markets remains the key tactical opportunity for relative value traders.

📰 In the News This Week — Policy, Politics & Macro Signals (Oct 6–10, 2025)

China Announces New Export Controls on Rare Earths & Battery Inputs

Announced by: Ministry of Commerce (MOFCOM)

Date: Oct 9, 2025

Details: Beijing introduced new export controls (effective Nov 8) on rare-earth-related materials, superhard industrial inputs, and lithium battery components including graphite anodes. The directive covers both materials and manufacturing equipment.

Interpretation:

Extends China’s strategic use of export controls across the upstream supply chain — signaling a move from reactive countermeasures to systematic resource weaponization. The timing, ahead of U.S. elections and amid semiconductor tensions, underscores policy coordination.

Market read-through:

Bullish: domestic miners, rare-earth processors, and battery material suppliers.

Bearish: global EV producers and offshore tech reliant on Chinese inputs.

Macro: reinforces the “resource nationalism” theme; markets to price higher input volatility.

Trump Threatens 100% Tariffs on Chinese Imports

Announced by: U.S. President Donald J. Trump (official statement)

Date: Oct 10, 2025

Details: In response to China’s export controls, the U.S. will impose 100% tariffs on all Chinese goods starting Nov 1, 2025, and new export controls on “critical software.”

Interpretation: Marks a major escalation in the trade confrontation and formalises Tech Cold War 2.0 rhetoric. While details remain vague, the administration is framing this as a moral and economic response to “hostile” Chinese trade actions.

Market read-through:

Negative for offshore China equities, particularly exporters and tech hardware.

Heightens tail risk for global supply-chain rerouting, boosting ASEAN and Mexico.

Adds uncertainty to multinational earnings guidance in Q4.

Customs Crackdown on Advanced Chips (Nvidia China SKUs)

Announced by: PRC customs authorities / domestic media

Date: Oct 10, 2025

Details: China expanded semiconductor import checks to include all advanced chips, initially targeting Nvidia’s H20 and RTX Pro 6000D designed for China’s compliance markets.

Interpretation: Deepens enforcement of the dual-use tech control regime and reinforces Beijing’s drive toward indigenous AI compute capacity. This serves both security and industrial policy ends.

Market read-through:

Bearish: China AI/cloud data-center demand near-term.

Bullish: domestic chip, board, and EDA ecosystem; signals clear import-substitution tailwind.

MIIT Launches Satellite IoT Commercial Trials

Announced by: Ministry of Industry & Information Technology (MIIT)

Date: Oct 10, 2025

Details: MIIT authorized commercial trials for satellite IoT connectivity, linked to China’s “low-altitude economy” (drone logistics, smart agriculture, and autonomous flight corridors).

Interpretation: Part of China’s next-gen industrial digitization agenda, aiming to integrate aerospace, telecom, and advanced manufacturing. Reinforces the “space-to-earth data infrastructure” vision embedded in the 14th FYP’s digital economy initiatives.

Market read-through:

Positive for telecom hardware, UAV infrastructure, and AI-powered logistics.

Symbolic of dual-use innovation — civil-military tech crossover deepening.

Ministry of Transport to Impose Port Surcharges on U.S. Vessels

Announced by: Ministry of Transport

Date: Oct 10, 2025

Details: Effective Oct 14, China will impose “special port charges” on ships owned by U.S. companies, organizations, or individuals.

Interpretation: A narrow but politically charged retaliatory measure, designed to signal firmness without disrupting broader trade flows.

Market read-through:

Minor operational cost rise for U.S. shippers; symbolic escalation more than economic shock.

Highlights the tit-for-tat dynamic feeding volatility in logistics, ports, and shipping equities.

RMB Settlement Expands to Bulk Commodities

Announced by: Chinese domestic media citing BHP and China Mineral Resources Group (CMRG)

Date: Oct 2025

Details: BHP agreed to accept RMB settlement for iron ore trades with Chinese buyers beginning Q4 2025.

Interpretation: A milestone in de-dollarisation and the internationalisation of the renminbi, especially in commodities invoicing. Enhances China’s leverage in commodity finance and FX risk management.

Market read-through:

Structural positive for RMB adoption; neutral for short-term FX levels.

Reinforces CN push to denominate energy and metals in RMB.

World Bank Raises China Growth Forecast

Announced by: World Bank

Date: Oct 7, 2025

Details: China’s 2025 GDP forecast raised to 4.8% (from 4.0%), and 2026 to 4.2%, citing improved policy coordination and stabilization in property and manufacturing.

Interpretation: An endorsement of the “managed soft landing” thesis — the global institutional community sees China’s cyclical trough as past.

Market read-through:

Sentiment support for macro-sensitive A-shares (banks, construction).

Reinforces policy credibility heading into 2026; improves EM fund rebalancing optics.

Golden Week Travel Demand Holds Steady

Announced by: Citi Research / Ministry of Transport data

Date: Oct 7, 2025

Details: Nationwide travel demand during Oct 1–6 rose ~5% YoY, led by eastern China. Spending remained rational but resilient, skewed toward short-haul domestic trips.

Interpretation: Confirms modest but stable consumption — households remain cautious but are not retrenching. Reflects the “plateau, not collapse” dynamic in post-pandemic leisure spending.

Market read-through:

Modestly positive for travel, hospitality, and urban services.

Reinforces policy case for targeted consumption stimulus, not blanket demand boosts.

Solid-State Lithium Battery Breakthrough Announced

Announced by: Chinese Academy of Sciences (CAS) via China Daily

Date: Oct 10, 2025

Details: Researchers reported two advances in solid-state lithium tech — reduced interfacial resistance and improved ion transport — overcoming key commercial bottlenecks.

Interpretation: Strategic messaging aimed at sustaining China’s EV leadership narrative as export controls tighten; reinforces domestic confidence in homegrown innovation capacity.

Market read-through:

Supportive for long-term battery supply-chain valuations.

Adds thematic tailwind to CN “deep-tech” equities.

Copper Nears Record on China Re-entry Post-Holiday

Announced by: Bloomberg / LME data

Date: Oct 9, 2025

Details: Copper futures spiked over 3% to nearly $11,000/t, driven by strong Shanghai Futures Exchange buying and global supply disruptions.

Interpretation: Signals resurgent Chinese commodity appetite and underscores the re-inflation of industrial metals — a key barometer of policy transmission.

Market read-through:

Bullish for metals, mining, and grid electrification themes.

PPI tailwind for materials; risk of cost push for manufacturing equities.

China Commissions 2×1000MW Supercritical Coal Plant

Announced by: China Energy Construction / provincial authorities

Date: Oct 10, 2025

Details: The Puxi Phase III (2×1000MW) ultra-supercritical coal plant in Xian’ning entered operation, reinforcing energy security goals.

Interpretation: Part of Beijing’s “build the base, scale the new” power strategy — ensuring baseload reliability as renewables scale up.

Market read-through:

Bullish: Power equipment, EPC, and grid integration firms.

Macro: Supports stable electricity supply for manufacturing hubs.

📊 Macro Data Review – Week of Oct 6–10, 2025

This week’s macro signals were limited given the Golden Week holiday, but FX data and early post-holiday consumption indicators offered insight into external balances and domestic momentum. Reserves strengthened modestly, while Hong Kong’s PMI slipped but remained expansionary. On the consumption side, tourism and box office data showed resilient but rational household spending, consistent with a slow but steady recovery narrative.

External Sector – FX Reserves Edge Higher

China Foreign Exchange Reserves (Sep): US$3.339T (vs. Aug US$3.322T, cons US$3.31T)

Hong Kong Reserves (Sep): US$419.2B (vs. US$421.6B)

Interpretation:

China’s reserves rose slightly for a third straight month, reflecting valuation gains on non-dollar assets and modest capital inflows into onshore bonds and equities. The stability underscores PBoC’s success in maintaining FX equilibrium despite dollar strength and trade tensions.

Hong Kong’s reserves dipped marginally, consistent with ongoing capital outflows and intervention under the linked exchange rate system as the HKD stayed near the weak end of its band.

Market read-through:

Stable FX data supports the “managed stability” narrative for the RMB.

Inflows to onshore markets remain selective but positive, reinforcing A-share resilience vs. offshore weakness.

HK’s minor reserve draw aligns with soft liquidity and continued volatility in offshore funding costs.

Activity – Hong Kong PMI Holds Above 50

S&P Global PMI (Sep): 50.4 (prev 50.7, cons 50.7)

Interpretation:

Business activity in Hong Kong slowed slightly but remained in expansionary territory for a fourth consecutive month. Services and logistics weakened modestly, offset by stabilization in construction and trade-related sectors. The data aligns with a “low-growth plateau” rather than renewed contraction.

Market read-through:

Consistent with subdued equity turnover and mixed property sentiment.

PMI above 50 signals continued recovery but limited earnings traction for cyclical HK names.

Reinforces view that offshore liquidity, not local activity, remains the key drag on the Hang Seng Index.

Consumption – Steady, Rational Holiday Demand

Golden Week Tourism (Oct 1–6): Passenger throughput +5% YoY (Ministry of Transport)

National Day Box Office: ¥1.835B, 50M viewers, 99% domestic share (National Film Administration)

Interpretation: Holiday data confirm moderate but durable consumption momentum. Leisure travel rose modestly, led by eastern provinces, while box office results highlight the dominance of domestic content and cultural soft power emphasis. Spending remains value-conscious but not depressed, supporting expectations that consumption recovery will continue gradually rather than explosively.

Market read-through:

Supports consumer service and domestic tourism equities, but not enough to re-rate valuations.

Aligns with HSBC’s call for targeted consumption support (pensions, welfare, and urbanization incentives) rather than broad fiscal expansion.

Indicates social cohesion and internal confidence remain policy-sensitive levers heading into 2026.

Interpretation Summary

The week’s limited releases reinforced three core macro narratives:

External Stability: Rising reserves and a firm RMB indicate China’s external balance remains well-managed despite intensifying U.S. rhetoric.

Domestic Caution, Not Retrenchment: Holiday consumption shows resilience within a “rational spending” regime — households are participating, but selectively.

Liquidity Divergence: Onshore liquidity is steady, but Hong Kong continues to face tightness and weaker confidence, reflected in the Hang Seng’s underperformance.

Overall, the data support the thesis that China’s recovery remains stable but unspectacular — enough to sustain selective equity optimism, especially in onshore cyclicals and commodities, but not yet a trigger for full-scale risk re-rating.

🏢 Company News – Week of Oct 6–10, 2025

China Northern Rare Earth – Profit Surges Amid Export Control Tailwinds

Announced by: Company filing

Date: Oct 10, 2025

Details: China Northern Rare Earth (600111 CH) expects Q1–Q3 2025 net profit of CNY 1.51–1.57B, up 272%–287% YoY, citing price strength in rare-earth magnets and improved downstream margins.

Takeaways:

Earnings momentum validates Beijing’s recent rare-earth export control strategy — tightening overseas supply while improving domestic pricing power.

The sharp YoY rebound underscores the structural pricing leverage China retains in critical materials, echoing policy emphasis on resource security.

Market read-through:

Bullish for upstream resource equities and policy-backed rare-earth chains.

Reinforces the “strategic materials = profit center” narrative within China’s new industrial policy cycle.

Caijing Magazine Cover Story – “Hard Tech IPO Wave” Signals Capital-Market Reorientation

Announced by: Caijing Magazine (Issue dated Sept 29, 2025)

Date surfaced: Oct 11, 2025 (via media and policy circles)

Details:

The latest cover story of Caijing Magazine — titled “硬科技上市潮” (Hard-Tech IPO Wave) focuses on the emergence of deep-tech listings as the new core narrative of China’s capital markets. The article highlights the structural pivot away from consumer internet, property, and short-cycle manufacturing toward semiconductors, AI hardware, robotics, new materials, and aerospace.

The feature dissects how regulatory gatekeepers, including the China Securities Regulatory Commission (CSRC), are recalibrating IPO approval frameworks under the new “high-quality growth” mandate. It quotes multiple policy-linked economists describing the push for “科技硬实力” (technological hard power) as central to the next phase of capital-market reform.

The piece also emphasises three underlying trends:

Policy-led capital allocation: Hard-tech listings are increasingly channelled through STAR Market (Shanghai) and ChiNext (Shenzhen), with the CSRC deploying a fast-track review process for strategic sectors (chips, robotics, green energy).

IPO normalisation after 2023–24 freeze: Following two years of tightened scrutiny and capital drought, the reopening for “strategic technologies” signals a controlled thaw — not a full liberalisation, but a policy-managed resumption with thematic guidance.

Institutionalisation of market confidence: Caijing underscores Beijing’s belief that capital markets must now serve national development priorities, shifting from growth-at-all-costs to innovation-driven financing.

Interpretation:

This cover is symbolically powerful because Caijing sits at the intersection of policy, finance, and academia — its editorial line often echoes or previews regulatory thinking within the State Council’s Financial Stability and Development Committee (FSDC). By elevating “hard tech IPOs” to a national narrative, the publication is effectively signaling that the leadership has sanctioned a new cycle of capital formation, one grounded in industrial sovereignty rather than speculative growth.

It also dovetails with broader propaganda and policy coordination seen in Q3 2025 — e.g., the National Science and Technology Work Conference’s emphasis on “indigenous innovation chains”, the Ministry of Industry and Information Technology’s new AI + manufacturing integration pilot zones, and recent export control actions that define self-reliance through selective decoupling.

Market read-through:

Sentiment: Positive for STAR/ChiNext segments, which have lagged due to weak IPO flow; this narrative signals renewed policy sponsorship.

Sector impact: Favors semiconductors, precision manufacturing, aerospace components, and industrial software over consumer apps, fintech, and property developers.

Capital flow: Domestic institutional investors (e.g. insurance funds, policy banks, local government funds) likely to reweight toward “deep-tech” ETFs and IPO allocations, reinforcing structural support.

Strategic takeaway: Marks a third-generation capital-market reform cycle — 2009–15 (internet/consumption), 2016–22 (industrial upgrading/property finance), 2023 onward (deep tech and national capability).

In essence, Caijing’s cover captures the re-legitimization of China’s equity markets as instruments of industrial strategy. It’s not just about which companies list — it’s about redefining what kinds of growth the Party-state now wants capital to reward.

Complete Index Performance List:

🛒 Internet & Platforms

Alibaba fell sharply by –10.6%, the worst performer in the group, as investors rotated out of high-beta e-commerce and AI names after the Golden Week rally. Baidu dropped –8.9%, reflecting fading enthusiasm around its AI ecosystem and continued margin pressure. Tencent declined a milder –3.3%, showing its usual resilience as the sector’s defensive anchor. Meituan fell –4.2%, still weighed by food delivery competition and pricing scrutiny, while JD.com lost –5.8% on weak consumption data. Trip.com was broadly flat at –0.2%, helped by firm holiday travel bookings. Kuaishou slipped –3.2%, and NetEase lost –6.0% as investors de-risked gaming exposure.

Commentary:

Offshore China tech corrected hard, tracking the HSTECH Index’s –5.5% weekly decline. The selling was broad-based, driven by weaker global risk appetite and U.S.–China policy noise. Tencent and Trip.com held up best, while Alibaba and Baidu bore the brunt of profit-taking.

Takeaway:

Flows continue to consolidate into Tencent and Trip.com as low-volatility defensives. The rest of the internet complex remains hostage to sentiment swings until earnings visibility improves.

🚗 Autos & EVs

Autos were mixed but mostly lower. Li Auto dropped –7.5%, retracing recent strength, while Xiaomi declined –5.4% after a strong September. BYD eased –1.1%, resilient relative to peers, and Geely slipped –1.7%.

Commentary:

The group faced a combination of post-holiday demand normalization, high inventories, and ongoing tariff uncertainty. Investor preference remains with firms showing pricing discipline and diversified product lines.

Takeaway:

Autos continue to be a stock-picker’s market. BYD remains the relative safe haven, while Xiaomi’s EV optionality still underpins long-term rerating potential despite near-term weakness.

💊 Healthcare & Biopharma

Healthcare was the worst-performing sector of the week. CSPC Pharma fell –12.9%, the steepest drop among large caps, followed by WuXi Biologics at –10.2% and WuXi AppTec at –7.0%. Sino Biopharm also lost –7.0%, Hansoh Pharma declined –6.3%, Ali Health dropped –6.9%, and JD Health fell –5.8%.

Commentary:

Heavy derating hit both contract research names and e-pharmacies. Regulatory uncertainty, global biotech weakness, and profit-taking after a strong H1 rally combined to drive the sector lower.

Takeaway:

Investors remain cautious toward healthcare growth names as risk premiums rise. WuXi Biologics and AppTec retain structural leadership but near-term sentiment is fragile and liquidity thin.

🏦 SOEs & Financials

The financial complex remained under pressure. Among banks, ICBC fell –6.1%, CCB –0.4%, and Bank of China –8.8%, while BOC Hong Kong slipped –0.8%. Ping An declined –1.7%, China Life –5.8%, and AIA a heavy –8.5%. HKEX also eased –1.2% on weaker turnover, while telecoms gave back prior gains — China Mobile lost –5.6%, China Telecom –5.7%, and China Unicom –0.7%.

Commentary:

Yield-oriented SOEs failed to protect portfolios this week. The “carry trade” in high-dividend state banks and telcos unwound as bond yields edged higher and sentiment turned defensive.

Takeaway:

Dividends continue to anchor valuation but won’t drive rerating. The sector remains range-bound, with telcos in particular now facing fatigue after months of outperformance.

🏘 Property & REITs

Property and REITs were again weak. CR Mixc dropped –5.2%, CR Land –2.1%, and China Overseas was flat (–0.1%). CK Asset, however, managed a small gain of +1.0%, supported by buyback speculation and relative balance-sheet strength. Link REIT slid –6.6%, while Wharf REIC was nearly unchanged (–0.2%). SHKP eased –0.7%.

Commentary:

Despite continued chatter around RMB500bn in recapitalization support and arrears cleanup, the market remains unconvinced. Funding conditions are tight and leasing demand weak.

Takeaway:

The property complex remains largely uninvestable as a group. Only the most liquid, diversified developers and REITs with strong cash generation — notably CK Asset and SHKP — offer credible downside protection.

⚙️ Materials & Energy

Materials outperformed slightly relative to the broader market. Zijin Mining rose +1.8%, benefiting from firm gold and copper prices. China Hongqiao slipped –2.8%, while CNOOC dropped –6.5%, PetroChina –2.4%, Sinopec –2.8%, and China Shenhua –5.0%.

Commentary:

Base metals strength provided a rare bright spot for A-shares, but oil and coal names struggled. The major SOE producers saw muted buying interest despite stable crude, as investors rotated away from high-yield energy into hard-tech and metals exposure.

Takeaway:

Metals remain the cleaner macro hedge. Energy equities, though still dividend-heavy, are finding it hard to outperform without fresh earnings upgrades or commodity tailwinds.

The week marked a broad derisking across China and Hong Kong equities, with the Hang Seng Index down 3.1% and HSTECH off 5.5%, while onshore benchmarks such as the CSI 300 fell only 0.5%. The divergence highlights that foreign flows and sentiment, not fundamentals, dominated trading.

The only areas showing relative resilience were Zijin Mining and CK Asset, underscoring investor preference for tangible assets and defensiveness. High-beta growth sectors — particularly healthcare, internet, and EVs — bore the brunt of outflows.

Policy discourse continued to shift toward “hard-tech capital markets,” as flagged by Caijing Magazine, but that narrative hasn’t yet translated into market performance. Offshore China remains in a confidence rebuild phase, with volatility elevated (VHSI +5.6%).

⚖️ Bottom Line: Confidence correction, not capitulation

The post-holiday pullback was a positioning reset more than a macro shock, but it underscores how fragile offshore sentiment remains. Tech, healthcare, and EVs are back in valuation support zones, yet buying conviction is absent. Onshore markets look more stable but lack catalysts beyond policy rhetoric. Metals and select defensives (Zijin, CK Asset, Ping An) remain the only functional hedges.

Core positioning themes: stay selective in offshore tech (Tencent, Alibaba, Xiaomi), maintain metals exposure as a macro hedge, and treat financials and property purely as carry trades. Until there is concrete evidence of earnings traction or household demand recovery, this remains a trader’s market — not an investor’s one.

Have a great rest of the weekend and a lovely week ahead,

Panda Team