China Weekly Wrap: Markets, Macro & Tech – Key Developments This Week

a week that was 9-13 June 2025

Good morning,

We were back in publishing mode this week with two new pieces—one looking outward, the other drilling deep into China. First up, our “7 Best Ideas in Indonesia” followed last week’s macro deep dive with a concrete set of equity picks across financials, commodities, and consumer names. If you’re still building conviction on Southeast Asia’s most dynamic growth story, this is the piece that turns macro thesis into portfolio action.

Closer to home, we published our full initiation on COSL (China Oilfield Services Ltd.), which we think is one of the cleanest expressions of China’s offshore energy recovery. The stock still trades like a cyclical contractor, but the fundamentals now resemble something far more durable. Capital discipline, rising deepwater exposure, and overlooked global tailwinds make this a name to watch.

We are planning a big return to form this coming week - there will be a big oil review and we’ll start on a brand new sector! As usual majority of the pieces will be paywalled, so do join the sub stack if you haven’t already.

Serious about investing in Asia? Then your process needs more Panda.

We get it, for some readers, a Substack alone isn’t enough. If you’re looking for sharper insights, personalised feedback, or just someone to help you cut through the noise in China and Asia, we also offer bespoke research calls and strategy sessions.

Right now, we’re working with clients on China’s consumer landscape, the 2Q25 macro outlook, and yes robotics.

See what we offer here, and connect with us today or message us directly.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

With that, let’s unpack the week.

📊 Weekly Relative Performance Observations

Week of June 8–14, 2025

Broad Takeaway

This was a sideways-to-soft week for Chinese equities, with onshore indices drifting lower while Hong Kong posted modest gains. The Shanghai Composite and CSI 300 both slipped -0.25%, signaling investor hesitation in the absence of fresh macro signals. Meanwhile, the Hang Seng added +0.42%, still buoyed by rotation into property and defensives, but clearly cooling from May’s momentum.

Regionally, Taiwan led the pack with a +2.71% surge, thanks to TSMC-driven AI enthusiasm, while India (-1.14%)and Turkey (-2.32%) fell back amid political recalibration and commodity-linked volatility. While China lacked clear upside catalysts, it also avoided the heavy drawdowns seen elsewhere—a sign of tactical positioning rather than conviction.

🇨🇳 Performance in Chinese Equities

Shanghai Composite (SHCOMP): 3,376.99, -0.25%

Index drifted lower on light volume. Larger caps in finance and infrastructure softened, while tech sentiment remained hesitant. The muted move reflects a market still in search of leadership.

CSI 300 (SHSZ300): 3,864.18, -0.25%

A-shares underwhelmed, as early June optimism faded. State-owned financials were flat, and enthusiasm for cyclical reflation plays ebbed, suggesting that institutional appetite hasn’t materially shifted.

ChiNext Index: 2,043.82, +0.21%

Slight gains held up in automation and industrial software. Investors continue to nibble at growth names aligned with AI and productivity—but breadth remains poor, and sentiment fragile.

SSE SME Innovation Index: 2,447.52, -0.70%

After strong outperformance last week, small- and mid-cap tech pulled back. Names without clear state alignment or catalysts struggled to hold recent gains, underscoring the tactical nature of last week’s rally.

SSE Commodity Equity Index: +0.17%

Resource-linked equities, including offshore oil and metals names, found buyers. Momentum in COSL and other offshore service stocks is helping this segment maintain a quiet bid.

🇭🇰 Performance in Hong Kong Equities

Hang Seng Index (HSI): 23,892.56, +0.42%

Steady rather than strong. Real estate and banks provided ballast, but flows into tech cooled notably. Still, the index remains one of the best-performing YTD globally—just now entering a potential consolidation phase.

HSCEI (China Enterprises Index): 8,655.33, +0.30%

State-owned enterprises and insurers helped prop up the HSCEI, even as internet names faltered. The index continues to serve as a high-beta macro barometer, albeit with reduced volatility.

HS Red Chips: +1.27%

Strong move in SOEs and infrastructure-heavy names reflected bargain hunting and southbound inflows. The rotation suggests investors are looking for safety with upside optionality.

VHSI (Volatility Index): +1.97%

A mild uptick in volatility hints at uncertainty creeping back in. It’s not panic, but it reflects traders reducing leverage and rotating out of crowded trades ahead of mid-month data.

🌏 Regional Peers – Weekly Performance

🇹🇼 FTSE TWSE Taiwan 50: +2.71%

Taiwan was the region’s standout once again, powered by the unrelenting strength of TSMC and the broader AI hardware trade. Investor appetite for semiconductors remains voracious, driven by global demand for compute capacity and optimism around new node deployment in H2. With foreign inflows returning and tech leadership intact, Taiwan continues to command a valuation premium despite its cyclical exposure. For now, macro risks are being shrugged off in favor of structural tailwinds.

🇰🇷 KOSPI Composite: (Estimate: ~+1.5%)

While not shown explicitly in the chart, Korea likely posted moderate gains, consistent with the regional tech trend. Memory names saw follow-through on earlier guidance upgrades, and exporters found support as the won stabilized. That said, retail investor enthusiasm has faded slightly versus Q1 highs, and positioning is increasingly skewed toward large-cap tech at the expense of domestic cyclicals.

🇯🇵 TOPIX: -0.46%

Japanese equities pulled back again as the market braced for potential signals from the Bank of Japan’s mid-June meeting. Volatility in the yen and confusion around the path for YCC (Yield Curve Control) continued to weigh on bank and insurance stocks. Exporters were also hit by currency whipsaws. Foreign investors trimmed risk ahead of policy clarity, and there’s growing unease that BoJ normalization—however slow—could reset equity multiples.

🇮🇳 NIFTY 50: -1.14%

Indian markets came under pressure as the political honeymoon from Modi’s re-election began to wear off. The BJP’s need for coalition support introduced fresh uncertainty around the pace and scope of key economic reforms. Investors reassessed PSU valuations after a blockbuster pre-election rally, and foreign funds rotated selectively out of financials and industrials. All eyes now turn to the upcoming Union Budget and its potential signals on capex continuity and fiscal direction.

🇮🇩 FTSE Indonesia: ~Flat (Estimate: +0.3%)

The market largely consolidated after its strong performance through May. Banks held firm, but resource-linked names were hit by weakness in coal and palm oil prices. Investor focus is shifting from electoral euphoria to economic fundamentals, especially around Jokowi’s succession timeline and signals from the new administration on fiscal discipline. The domestic growth story remains intact—but a pause in commodity momentum has capped near-term upside.

🇹🇷 BIST 100 (Turkey): -2.32%

A sharp reversal this week as foreign buyers stepped back following a month of strong inflows. Cooling inflation expectations and an appreciating lira had previously supported a mini-rally, but gains proved fragile. Banks and industrials gave back recent strength as concerns resurfaced around Turkey’s external financing and central bank credibility. This remains a tactical, flow-driven market highly sensitive to macro noise.

🇸🇬 MSCI Singapore: +0.08%

With no major catalyst or earnings flow, Singapore equities likely traded sideways. REITs remain in a holding pattern pending clarity on rates, while the broader index is treading water alongside muted regional growth forecasts.

🇦🇺 ASX 200: +0.3%

Australian equities edged lower amid continued uncertainty around China’s commodity demand and weakness in materials. Banks remained range-bound as the RBA held rates steady and housing data came in mixed. A lack of direction from both domestic and global catalysts has left the ASX drifting just below its YTD highs.

💡 Takeaways for Chinese Equities in a Regional Context

China drifted while peers diverged

Mainland markets were broadly flat to negative, offering stability but no clear upside. This left China underperforming Taiwan and Korea (buoyed by tech), but outperforming India and Turkey, where politics and FX volatility dragged markets lower. In short: China was neither a haven nor a momentum play.

Hong Kong held up amid regional chop

The Hang Seng delivered a modest gain, keeping it in positive territory YTD and positioning it as a relative outperformer. Southbound inflows and yield rotation into banks, REITs, and red chips provided a stabilizing force even as tech gave ground. Compared to Japan’s policy nerves and India’s post-election reset, Hong Kong’s steadiness was a net positive.

Asia bifurcates: AI vs. macro drag

Taiwan and Korea continued to lead on the back of AI hardware optimism, with TSMC and memory chipmakers absorbing most of the flows. Meanwhile, India and Turkey were hit by domestic noise, and Indonesia paused after a solid May. China sits in between—lacking the AI buzz but offering a more constructive macro backdrop than the political laggards.

China isn’t being sold—but it’s not being bought aggressively either

There’s no wholesale derating underway, but the market is still defined by tactical positioning and low conviction. With policy steady but uninspiring, and earnings season weeks away, China remains in a holding pattern—a relative stabilizer, not a regional leader yet.

📰 In the News This Week

Announced by: Chinese Carmakers (via MIIT and Caixin)

Date: June 13, 2025

More than a dozen Chinese carmakers—including BYD, Geely, Chery, FAW, Dongfeng, and Xiaomi Auto—formally pledged to pay their suppliers within 60 days, in response to new government guidelines aimed at restoring supply chain stability. The shift comes amid pressure from regulators to end payment delays that have contributed to financial strain across upstream auto suppliers.

This Indicates:

An important policy-led intervention to ease working capital pressures in the EV supply chain. Extended payment terms of 120–200 days had become common across the industry, contributing to insolvencies and vendor pullback. The 60-day pledge signals a more coordinated attempt to restore trust, improve liquidity conditions, and curb the worst effects of the ongoing EV price war.

Announced by: Chinese Academy of Sciences

Date: June 12, 2025

China launched “Qimeng,” an AI-powered chip design system developed by the Chinese Academy of Sciences and associated national research labs. Qimeng is intended to replace U.S.-origin EDA (electronic design automation) tools and will be open-sourced for domestic developers. The system uses large language models to automate chip design workflows.

This Indicates:

A major step in China’s push for semiconductor self-sufficiency. By reducing dependence on U.S. EDA tools, Qimeng addresses one of the most sensitive chokepoints in China’s chip design ecosystem. Its release follows tighter U.S. export controls and signals Beijing’s intent to develop a full-stack domestic solution for high-end integrated circuits.

Announced by: Ministry of Commerce and U.S. Trade Representative’s Office

Date: June 10–12, 2025

Chinese and U.S. officials held two days of trade talks in London following a call between Presidents Xi and Trump. Statements from both sides reiterated commitments made during the June 5th Geneva meeting. China pledged to resume rare earth exports and reopen access to certain U.S. agricultural goods. The U.S., however, did not announce any tariff rollback.

This Indicates:

A cautious détente in U.S.–China economic relations, with both sides seeking to stabilize trade channels while protecting core interests. China’s willingness to reopen sensitive exports is a notable concession. However, the lack of movement on U.S. tariffs underscores lingering distrust and the transactional nature of the current dialogue.

Announced by: China’s General Administration of Customs

Date: June 13, 2025

China approved pork and poultry imports from 106 U.S. meat-processing facilities, marking a partial restoration of agricultural trade access suspended during earlier tariff escalations. Major U.S. exporters including Tyson, Smithfield, and Perdue were included, while beef exporters remain excluded.

This Indicates:

A selective easing of trade restrictions meant to de-escalate tensions while maintaining leverage. Pork and poultry imports were among the key components of the original Phase 1 agreement. Their reinstatement suggests China is offering goodwill gestures within politically neutral categories, while preserving room for negotiation in more sensitive sectors.

Announced by: National Development and Reform Commission (NDRC)

Date: June 10, 2025

NDRC Chair Zheng Shanjie met with senior executives from China’s leading private tech firms to discuss innovation policy under the upcoming 15th Five-Year Plan (2026–2030). The meeting focused on aligning private sector R&D with state priorities in advanced computing, industrial automation, and AI infrastructure.

This Indicates:

Renewed efforts to coordinate long-term industrial policy with the private sector, following a period of regulatory tension and capital outflows. The meeting underscores Beijing’s strategic reliance on domestic firms for technological upgrading and reflects a more pragmatic stance toward innovation-oriented entrepreneurs.

Announced by: NDRC Chair Zheng Shanjie

Date: June 10, 2025

Zheng convened a symposium with private tech leaders, including Ant Group, and BGI—to gather input for the 15th Five‑Year Plan (2026–30) . Participants emphasized integration of innovation with industrial applications, calling for enhanced support in funding, talent, and data.

This Indicates:

A clear pivot: policy is shifting toward public–private coordination on long-term innovation, signalling reconciliation after the clampdowns of recent years and highlighting tech’s strategic centrality to future industrial policy.

📈 The week in Macro Data:

It was a dense week for Chinese macro releases, spanning inflation, trade, credit, and vehicle sales. The overall tone was mixed: inflation remained flat, trade disappointed, and credit growth came in stronger than expected—but still below peak recovery levels. The standout was vehicle sales, which jumped into double-digit YoY growth, hinting at resilience in consumer durables despite a challenging pricing environment.

Inflation (May)

YoY: -0.1% (Consensus: -0.2%, Previous: -0.1%)

MoM: -0.2% (Consensus: 0.0%, Previous: +0.1%)

This Indicates:

China’s inflation remains stuck near zero, with May showing renewed weakness across both annual and monthly prints. The MoM dip points to slumping food prices and a further softening in services, while core CPI remains anaemic. Although the deflation narrative isn’t accelerating, persistent disinflation leaves little margin for policy complacency. Without income growth or consumer stimulus, price signals are unlikely to improve materially.

Producer Prices – PPI YoY (May)

Actual: -3.3% | Consensus: -3.2% | Previous: -2.7%

This Indicates:

Producer price deflation deepened in May, marking the sharpest drop since Q4 last year. The fall was broad-based—driven by chemicals, metals, and energy—as weak demand and overcapacity continue to drag on upstream pricing. This reinforces margin pressure across heavy industry and underscores the challenges facing China’s industrial recovery.

Trade (May)

Trade Balance: $103.22B (Consensus: $101.3B, Previous: $96.18B)

Exports YoY: +4.8% (Consensus: +4.0%, Previous: +8.1%)

Imports YoY: -3.4% (Consensus: -0.9%, Previous: -0.2%)

This Indicates:

China’s trade surplus widened, but largely due to a contraction in imports—not strength in exports. Export growth slowed and remains uneven, with resilience in ASEAN offset by weakness in Western demand. Imports were a notable disappointment, suggesting ongoing softness in domestic investment appetite. Taken together, the data confirm that external demand is holding up better than internal reacceleration.

Vehicle Sales YoY (May)

Actual: +11.2% | Consensus: +10.3% | Previous: +9.8%

This Indicates:

Automotive demand surprised to the upside again, with broad-based gains across internal combustion and NEVs. The increase is partly driven by aggressive discounting and base effects, but also reflects solid momentum in Tier 2–3 cities. Commercial vehicle demand remains muted, but the passenger segment continues to absorb volume well.

Credit & Liquidity (May)

New Yuan Loans: CNY 620B (Consensus: CNY 900B, Previous: CNY 280B)

Total Social Financing (TSF): CNY 2.29T (Consensus: CNY 2.50T, Previous: CNY 1.16T)

M2 Money Supply YoY: +7.9% (Consensus: +8.2%, Previous: +8.0%)

Outstanding Loan Growth YoY: +7.1% (Consensus: +7.3%, Previous: +7.2%)

This Indicates:

Credit conditions improved from April’s depressed levels but remain underwhelming relative to expectations. The rebound in new loans and TSF reflects stronger government bond issuance and some uptick in corporate borrowing, but household credit remains weak, and M2 growth continues its gradual deceleration. Loan growth—both in banks and shadow channels—is plateauing, highlighting the gap between liquidity provision and private sector risk appetite.

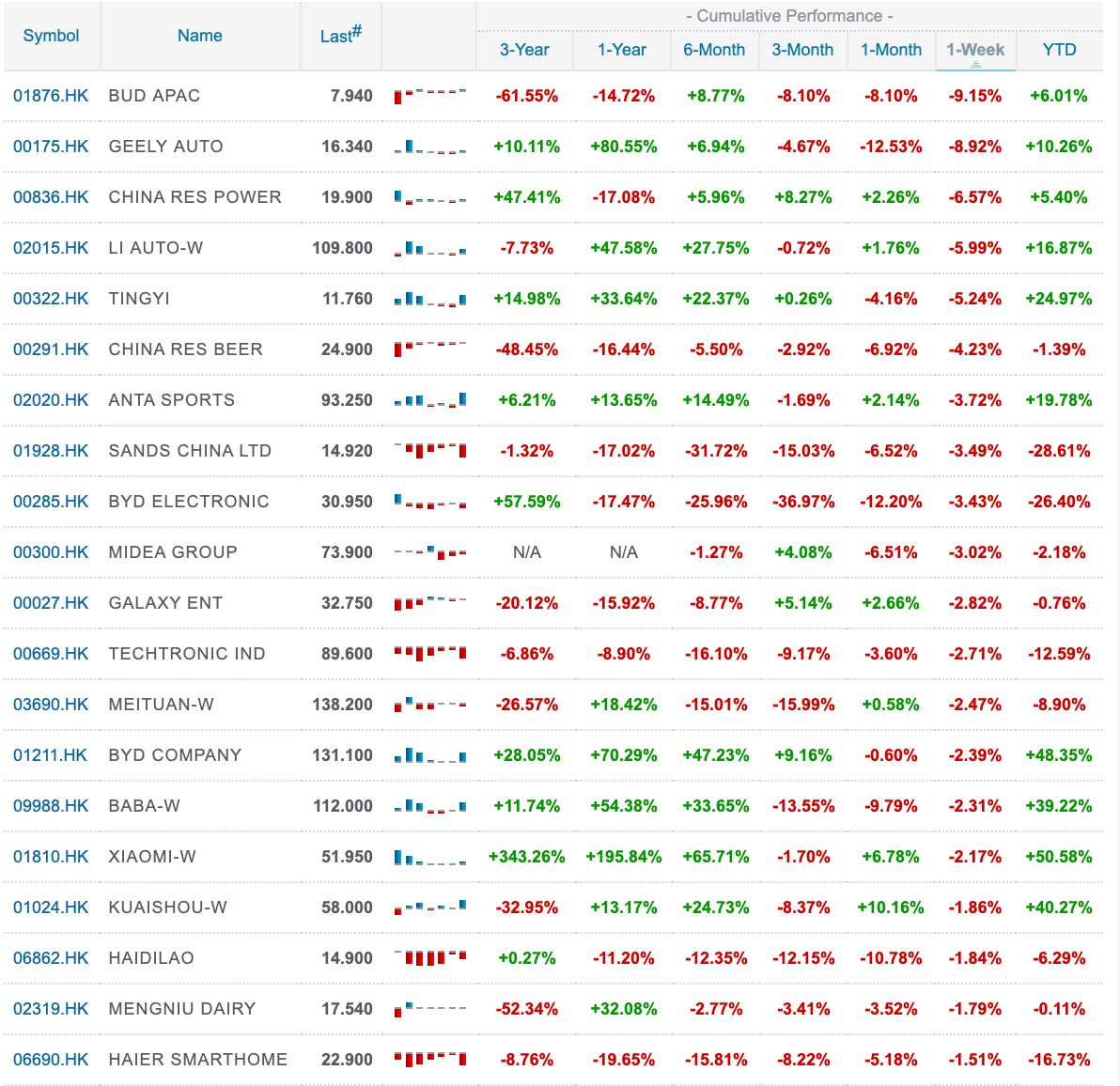

Complete Index Performance List:

General Trends

Chinese equities saw a quieter, more rotational week following strong gains in late May and early June. Onshore markets drifted modestly lower, while Hong Kong equities posted mild gains, supported by rotation into property, financials, and SOEs. The rally in innovation-linked small caps paused, and growth stocks gave back ground, while yield plays and resource names found support.

Investor tone remains tactical. There’s no panic, but conviction is still lacking. Policy headlines on tech sovereignty and trade diplomacy were helpful at the margin, yet macro data offered more evidence of a fragile recovery—particularly in imports, inflation, and credit. Sector rotation rather than net buying remains the dominant theme, suggesting capital is still circulating, not expanding.

Mainland Indices: Range-Bound with Commodity Edge

Shanghai Composite (SSE): -0.25% to 3,377.00

CSI 300 (SHSZ300): -0.25% to 3,864.18

ChiNext Index: +0.21% to 2,043.82

Shenzhen 100: -0.74%

SSE SME Innovation Index: -0.70%

SSE Dividend Index: -0.80%

SSE Mega-cap Index: +0.55%

SSE Commodity Equity Index: +1.17%

Interpretation:

A-shares showed signs of fatigue. After a strong May, investor appetite cooled as macro softness (imports, credit) outweighed policy tailwinds. Small- and mid-cap innovation names saw outflows, particularly in biotech and AI software. ChiNext held steady, helped by continued interest in automation and robotics. The standout performer was commodity equities, with oil services, metals, and coal stocks continuing to benefit from global reflation trades and supply-side reform sentiment.

Offshore Indices: Sector Rotation Masks Overall Drift

Hang Seng Index (HSI): +0.42% to 23,892.56

HS Tech Index: -0.89%

HSCEI (China Enterprises): +0.30%

HSI Financials: +2.26%

HSI Red Chips: +1.68%

HSI Property: +2.66%

HSI Industrials: -0.65%

GEM: -2.15%

VHSI (Volatility): +3.69%

Interpretation:

Hong Kong markets extended gains—barely—but breadth shifted meaningfully. After weeks of leadership from tech, biotech, and high-beta names, capital rotated into yield and property. Financials and SOEs absorbed the bulk of buying interest, aided by southbound inflows and better liquidity. Tech lagged, as investors digested rich valuations and regulatory caution. The volatility index rose, pointing to a more fragile risk environment despite index-level stability.

Macro Takeaway

Markets moved on:

Automotive policy coordination: The MIIT-mandated 60-day supplier payment rule helped ease credit risk sentiment in upstream EV supply chains.

Semiconductor decoupling narrative: The release of the QiMeng AI chip design tool signaled China’s intent to localize advanced semiconductor workflows, boosting sentiment in industrial software and niche AI tools.

U.S.–China détente: Trade talks in London and rare-earth licensing reform suggested a willingness to de-escalate, though investors are clearly awaiting action over rhetoric.

Mixed data: May inflation flatlined, exports slowed, imports fell sharply, and credit growth disappointed. It paints a picture of recovery, but one that’s uneven and still largely policy-dependent.

Conclusion: The market remains cautiously long. Positioning is rotating, not expanding. Without stronger data or policy surprises, risk appetite is likely to stay shallow.

🧭 Sector & Style Trends

EVs and Autos: Policy Support, but Stocks Drift

BYD Company (1211.HK): -2.39%

Geely Auto (0175.HK): -8.92%

Xiaomi-W (1810.HK): -2.17%

Li Auto-W (2015.HK): -5.99%

Interpretation:

Despite the negative print, this was a positive week structurally for the auto complex. The pledge by automakers to pay suppliers within 60 days, supported by MIIT, marks a significant step in normalizing working capital flows and reducing credit stress across the value chain. Share prices sold off on profit-taking, but we expect this reform to strengthen upstream suppliers and stabilize the sector’s foundations over time.

Biotech & Healthcare: Second Week of Outperformance

Wuxi Bio (2269.HK): +13.59%

Hansoh Pharma (3692.HK): +8.90%

Sino Biopharm (1177.HK): +21.54%

Ali Health (0241.HK): -0.76%

Interpretation:

Biotech extended gains for a second week, led by policy-aligned R&D names and gene therapy plays. Flows remain concentrated, suggesting institutional rotation rather than retail froth. That said, some softness at the end of the week signals that profit-taking may now be in play. Expect more selective moves going forward, with quality R&D and domestic procurement edge continuing to matter most.

Financials & SOEs: Defensive Rotation Takes Hold

China Life (2628.HK): +7.31%

CCB (0939.HK): +4.81%

Ping An (2318.HK): +4.38%

China Mobile (0941.HK): not shown this week, but broadly stable

Interpretation:

The SOE/value trade is alive and well. Banks, insurers, and large state-linked utilities absorbed new flows as tech corrected and volatility rose. Life insurers benefited from yield curve stability and muted regulation talk. China Mobile and telcos remain a defensive play in portfolios still sensitive to headline risk.

Property & REITs: Rotation + Policy = Breakout

China Resources Mixc (1209.HK): +5.17%

Henderson Land (0012.HK): +5.04%

HSI Property Index: +2.66%

China Overseas (0688.HK): +5.78%

Interpretation:

The property sector quietly led this week. News of expanded urban renewal programs and streamlined mortgage approvals contributed to a sustained bid across quality names. SOE developers led, as did landlords and REIT-like entities. Sentiment is still fragile, but price action suggests some investors are re-risking into policy-supported subsegments.

Consumer & Staples: Still a Shelter, But Selective

Nongfu Spring (9633.HK): +7.26%

China Resources Beer (0291.HK): -3.94%

Haidilao (6862.HK): -6.94%

Mengniu Dairy (2319.HK): -7.19%

Interpretation:

Staples offered a mixed bag. Nongfu delivered another strong week on volume and pricing upgrades, but discretionary names like Haidilao and Mengniu struggled under cost pressure and margin fatigue. Investors remain biased toward margin resilience, cash flow visibility, and local consumer exposure. F&B is still a haven—just not uniformly so.

Onshore Drifts, Offshore Rotates — A Week of Tactical Positioning

Markets took a breather this week. Onshore indices moved sideways, with the SSE and CSI 300 both slipping -0.25%, while Hong Kong extended its relative outperformance, buoyed by a clear rotation into SOEs, insurers, and property names. The Hang Seng Index (+0.42%) edged up, and the Red Chips (+1.68%) and HSI Financials (+2.26%) led sectorally.

Volatility rose slightly (VHSI +3.69%), reflecting fading momentum in tech and biotech and a more cautious tone. The rotation into yield and defensiveness suggests investors are still engaged—but not yet convinced.

Policy Headlines Offer Stability, but Not Yet a Catalyst

Investors responded positively to incremental—but meaningful—policy signals:

MIIT’s 60-day supplier payment mandate provided tangible relief for EV and auto supply chains, helping upstream industrial names stabilize.

QiMeng, China’s new AI-driven chip design tool, demonstrated real progress in EDA self-reliance and lifted sentiment in strategic software and AI-adjacent names.

US–China trade talks in London and Geneva signaled a controlled détente, with new export licenses and resumed U.S. agricultural imports indicating mutual interest in stabilization.

Property sector support continued via targeted subsidies and a more accommodative stance on mortgage approvals.

These developments provided a supportive backdrop, but without a coordinated stimulus push, investor conviction remained shallow.

Select Winners in a Rotational Market

Top-performing themes this week included:

Sino Biopharm (+21.5%), Wuxi Bio (+13.6%), and Hansoh Pharma (+8.9%), as biotech extended last week’s rally amid national innovation tailwinds.

China Life (+7.3%) and CCB (+4.8%), reflecting rotation into SOEs and high-yield financials.

China Resources Mixc (+5.2%) and Henderson Land (+5.0%), as policy support nudged capital back into quality developers and retail landlords.

Nongfu Spring (+7.3%), which continues to benefit from cash flow visibility and seasonal tailwinds.

At the same time, high-momentum names in EVs and tech came under pressure. Li Auto (-6.0%), Geely (-8.9%), and Meituan (-2.5%) all slipped, as investors rotated out of crowded trades and into policy-favored defensives.

Macro Still Mixed: Credit Rebounds, Trade Disappoints

The macro data offered no strong directional cue. CPI remained flat at -0.1% YoY; PPI deflation deepened to -3.3%. Imports fell sharply (-3.4%), suggesting continued weakness in domestic demand. While new credit issuance improved from April, it still fell short of expectations, especially on household loans.

The rebound in vehicle sales (+11.2%) was a bright spot, supporting resilience in consumer durables, but capex remains soft and private sector borrowing subdued.

Markets Want More Than Stabilisation

The message from capital flows is clear: markets are rotating, not rallying. Investors are rewarding policy visibility, balance sheet strength, and dividend yield, but remain cautious on high-beta growth and speculative recovery trades. Even in outperforming sectors like biotech or property, participation is still light and price action shallow.

Bottom Line

This was a constructive but cautious week. China’s equity markets are demonstrating resilience—but not broad strength. Macro data and policy support are helping floor expectations, but not spark upside surprises. In this environment, capital remains anchored to state-aligned, cash-generative, or strategically supported names.

Until we see decisive fiscal action, stronger household demand, or a global trade reset, leadership will remain narrow, and rallies will be rotational rather than directional. For now, stability is the new optimism.

Company News and Results (June 9-13, 2025)

Huawei Technologies

Announced: June 11, 2025

Details: Launched the Pura 80 smartphone series (including Pro and Ultra models), starting at RMB 6,499 (~$905), with a heavy emphasis on AI and camera functionality powered by XMAGE imaging technology .

Implications: Huawei is reinforcing its premium position and signaling continued push into AI-enabled consumer hardware, a clear move to solidify its domestic market share amid western sanctions.

Huawei – U.S. Export Control Update

Announced: June 12, 2025

Details: U.S. regulators capped Huawei’s production of advanced AI chips at 200,000 units for 2025 .

Implications: Constrains Huawei’s ability to scale AI-capable devices, shifting its competitive focus back to software optimization, system integration, and domestic chip alternatives.

Pop Mart International (9992:HKG)

Announced: June 10–13, 2025

Details: A record-setting Beijing auction sold a human-sized Labubu statue for RMB 1.08 million (~$150k), marking the first dedicated Labubu auction and totaling RMB 3.73 million across all lots .

On June 13, Pop Mart opened Popop, its first jewellery concept store in Shanghai, offering character-themed accessories priced RMB 350–2,699 .

Implications: Pop Mart is expanding Labubu’s reach from toys into high-end collectibles and lifestyle products. Investor excitement (shares hit record highs on June 12th) reflects strong consumer demand and strategic brand extension beyond blind-box collectibles .

China’s EV Makers – BYD Under Scrutiny

Announced: June 9, 2025

Details: Rival automakers Great Wall and Geely accused BYD of non‑compliant fuel tanks amid ongoing emissions probes. BYD defended its position, stating earlier models complied with standards and have since been corrected .

Implications: Heightened scrutiny amidst aggressive pricing by BYD (as low as RMB 55,800) could trigger regulatory pushback on its market dominance strategy. Although BYD remains the sector leader, controversies may introduce near-term volatility for all Chinese EV manufacturers.

EVE Energy (300014:SZ)

Announced: June 9, 2025

Details: Board approved a Hong Kong IPO of H-shares as the company pursues overseas expansion .

Implications: The listing would deepen international exposure and support EVE Energy’s global footprint as a key supplier to EV manufacturers, complementing domestic capacity builds.

Final Thoughts

This week was not a reversal, but a reset. Chinese markets didn’t lose momentum—they paused to digest it. Sector leadership narrowed, capital rotated defensively, and macro signals failed to inspire conviction. But policy support remains visible, corporate developments were broadly constructive, and volatility—while higher—is contained.

Investors are clearly engaged but unwilling to chase. For now, the market remains a game of positioning over direction. The leadership is state-aligned, dividend-rich, or innovation-secured. The path forward still demands patience—but the floor under risk is firmer than it was a month ago.

Regards,

Leonid

Notes:

Shanghai Composite Index (SHCOMP): Tracks all stocks (A and B shares) traded on the Shanghai Stock Exchange.

CSI 300 Index (SHSZ300): Represents the top 300 stocks traded on the Shanghai and Shenzhen Stock Exchanges.

China A50 Index (512150 CH): Comprises the top 50 A-share companies listed on the Shanghai and Shenzhen Stock Exchanges.

ChiNext Price Index (159954 CH): Focuses on innovative and high-growth enterprises listed on the Shenzhen Stock Exchange.

SSE STAR 50 Index (83151 HK): Represents the top 50 companies listed on the Shanghai Stock Exchange’s STAR Market, emphasising science and technology innovation.

Hang Seng Index (HSI): Measures the performance of the largest companies listed on the Hong Kong Stock Exchange.

Hang Seng China Enterprises Index (2828 HK): Includes major H-share companies listed in Hong Kong.

Currency Considerations:

Chinese Indices (SSEC, CSI300, China A50, CNT, STAR50): These indices are denominated in Chinese Yuan (CNY). To present their performance in USD terms, currency exchange rate fluctuations between the CNY and USD have been considered.

Hong Kong Indices (HSI, HSCEI): Denominated in Hong Kong Dollars (HKD). Their performance in USD terms reflects the HKD/USD exchange rate stability, as the HKD is pegged to the USD.