China Weekly Wrap: Markets, Macro & Tech - Key Developments This Week

The week of 8-12 September

Good Evening,

As mentioned in our recent post, it’s been an eventful time in the Panda world — but we continue to cover China market developments with our usual level of scrutiny and consistency. This week brought fresh policy and legislative moves, alongside several interesting corporate announcements. All very exciting — read on to find out more!

A quick programming note: tomorrow (Sunday) we’ll publish a special piece on earnings analysis, looking at the aggregate picture of 1H25 results in China and Hong Kong. This started out as an expanded feature here, but it quickly became clear that to do it justice, it deserved a standalone deep dive.

Much like this weeks piece on the semiconductor support tech (where we’re looking at things like Victory Giant thats up 17x in 2 years and 7x this year alone, and still just a $30bn company), the earnings review will eb paywalled, so do join up to read it, we’d love to have you!

And do check out the piece if you haven’t already:

Good Morning,

Its behind a paywall, so do consider subscribing if you are interested in reading it.

Turn context into conviction with Panda Perspectives+:

You already read the Substack for big-picture clarity.

Panda Perspectives+ adds the action layer live, personalised and ready when you are.

Advisory toolbox

1-on-1 strategy sessions

Direct time with our senior China-Asia analysts—for CIOs, PMs, analysts or founders who need to stress-test a thesis before capital moves.

Custom deep-dive research

From a 40-page teardown of BYD’s SiC supply chain to a same-week model on Shanghai micro-fabs delivered to your brief and timeline.

Live Q&A briefings for teams and ICs

Interactive calls (slides + recording included) that arm the entire desk with up-to-the-minute intelligence.

Panda Hand-Hold concierge

A dedicated analyst on speed-dial for emerging and private investors, quarterly portfolio health checks to iron out A-share quirks and FX traps, plus 30-minute mini-masterclasses that decode SAFE rules, cross-border custody and dual-currency settles.

Ready to sharpen your edge? Join in to the Founder tier for the intro service or browse the full advisory menu, or email us with “Upgrade”in the subject line and we’ll book your intro call within 24 hours.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

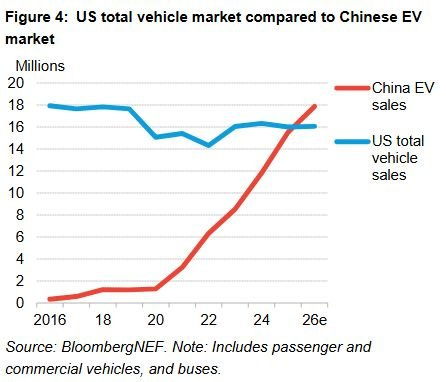

📊 Chart of the Week

By 2026, China’s EV sales are projected to firmly surpass total US vehicle sales, likely to match them this year. Courtesy of BNEF.

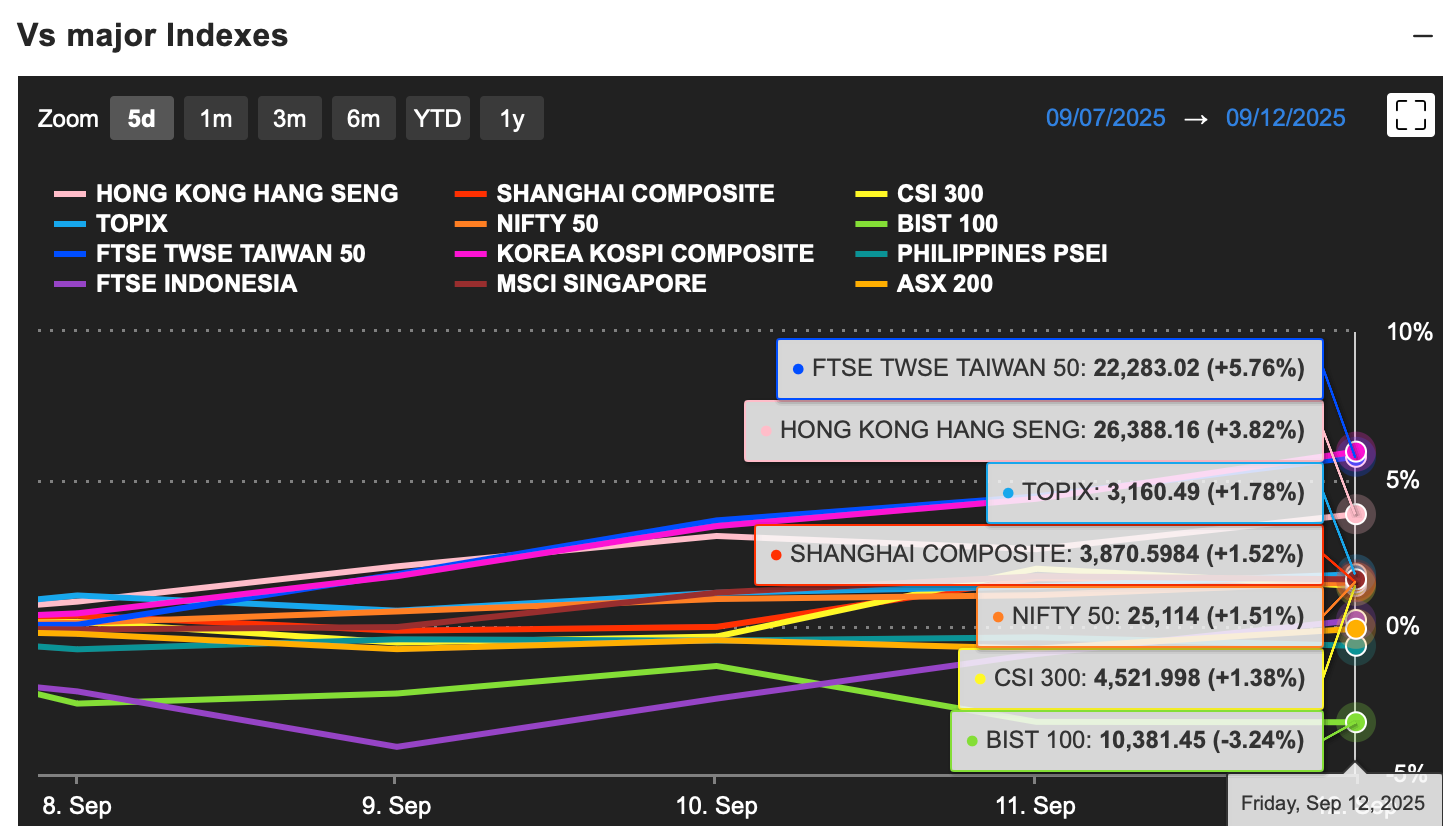

📊 Weekly Relative Performance Observations

Week of 8–12 September, 2025

📉 Broad Takeaway

Asian equities ended the week broadly higher, with Hong Kong and Taiwan leading gains while onshore China delivered smaller advances. The Hang Seng (+3.82%) and Taiwan (+5.76%) outperformed on strong tech and property rebounds, whereas the Shanghai Composite (+1.52%) and CSI 300 (+1.38%) posted more modest gains as domestic sentiment remained cautious. Japan and India rose steadily, while ASEAN performance was muted. Turkey reversed sharply (-3.24%), underscoring persistent volatility. Global conditions remained supportive, with U.S. yields contained and commodities stabilizing, giving Asia ex-China a strong bid.

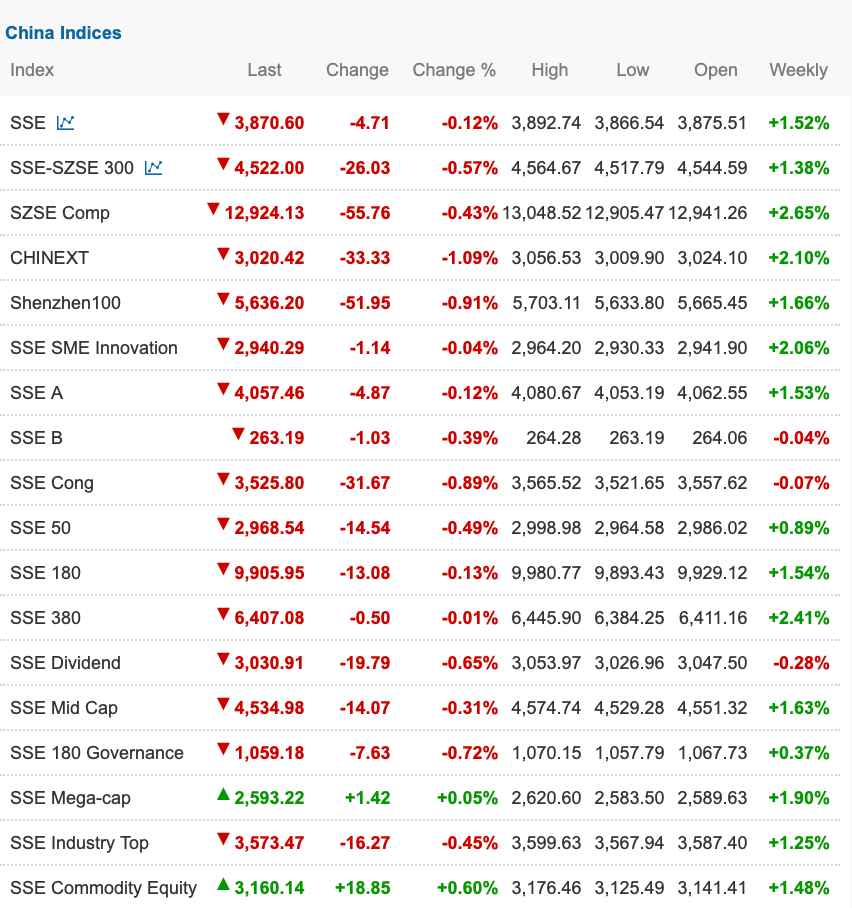

🇨🇳 Performance in Chinese Equities

Shanghai Composite (SSE): +1.52% – Gained modestly, supported by banks and mega-caps.

CSI 300: +1.38% – Large caps edged higher; financials and SOEs showed tentative flows.

SZSE Composite: +2.65% – Outperformed on mid-cap tech and growth exposure.

ChiNext Index: +2.10% – Innovation-linked sectors (AI, biotech, EV chain) drew selective buying.

Shenzhen 100: +1.66% – Rebounded on tech leadership.

SSE SME Innovation: +2.06% – Posted strong weekly rebound after prior softness.

SSE 50 / SSE 180: +0.89% / +1.54% – Large-cap benchmarks tracked CSI 300 modestly higher.

SSE Mid Cap: +1.63% – Cyclicals and growth outpaced large-cap peers.

SSE Mega-cap: +1.90% – SOE-linked mega-caps found renewed demand.

SSE Commodity Equity: +1.48% – Resource-linked equities strengthened alongside metals.

📌 Takeaway: Onshore A-shares moved higher across the board, with ChiNext (+2.10%) and SZSE Composite (+2.65%) showing leadership. Unlike recent weeks, SME Innovation rebounded (+2.06%), suggesting tentative stabilization in domestic risk appetite. Gains were broad but measured compared to offshore markets.

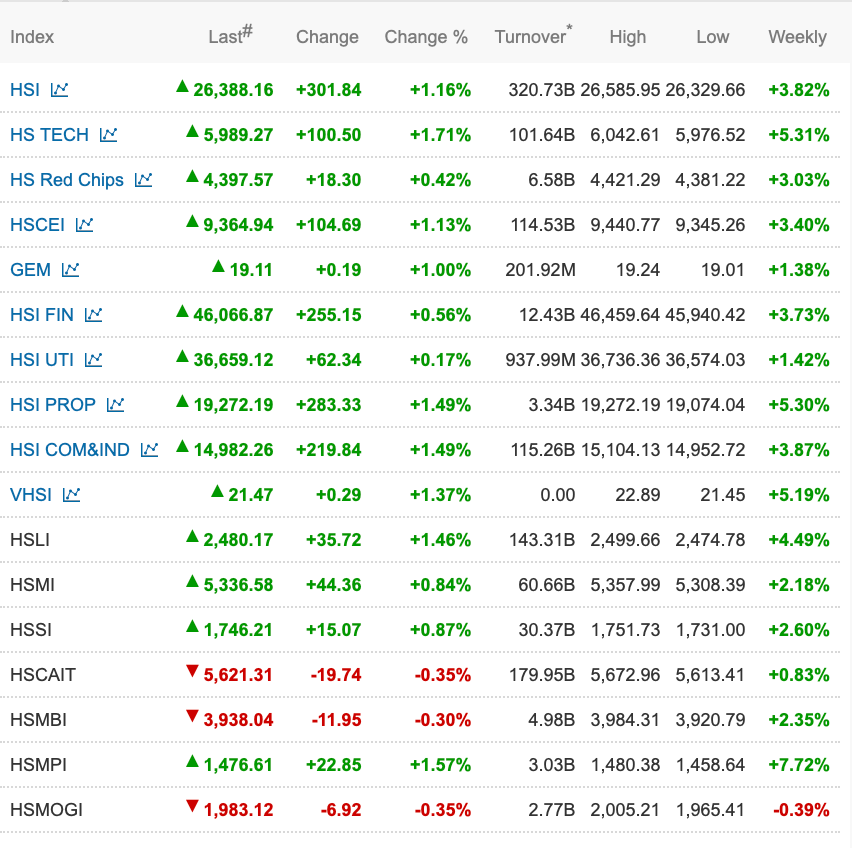

🇭🇰 Performance in Hong Kong Equities

Hang Seng Index (HSI): +3.82% – Led the region, boosted by tech, property, and finance.

Hang Seng Tech (HSTECH): +5.31% – Tech majors rallied strongly after weeks of volatility.

HSCEI (China Enterprises Index): +3.40% – Mainland financials and insurers advanced.

HS Red Chips: +3.03% – SOE-linked stocks rebounded.

HSI Finance: +3.73% – Banks and insurers climbed in line with market strength.

HSI Utilities: +1.42% – Defensive tone lagged broader market.

HSI Property: +5.30% – Surged, staging a major reversal from prior weakness.

HSI Commerce & Industry: +3.87% – Outperformed, led by consumer and industrial sectors.

VHSI (Volatility Index): -5.19% – Declined sharply, reflecting improved sentiment and risk appetite.

📌 Takeaway: Offshore China equities staged a decisive rebound, with property (+5.30%) and tech (+5.31%) leading. Bargain-hunting flows were evident, suggesting a tactical rotation into Hong Kong as investors tested “China value” trades. The sharp fall in volatility confirmed improving sentiment.

🌏 Regional Peers – Weekly Performance

🇹🇼 Taiwan (FTSE TWSE Taiwan 50: +5.76%) – Taiwan was the clear outperformer, with the rally concentrated in semiconductors and AI hardware. TSMC, MediaTek, and server-related names led gains as global demand signals for GPUs and data center capacity improved, while financials provided ballast. Foreign inflows accelerated, reflecting Taiwan’s dual identity as both a high-beta AI proxy and a defensive “North Asia safe haven” amid China policy uncertainty. However, breadth remains narrow — heavily tied to semiconductors — leaving Taiwan momentum-sensitive and vulnerable if AI enthusiasm falters or if U.S. tech faces a correction.

🇮🇳 India (NIFTY 50: +1.51%) – India posted another steady week, supported by banks and IT services. Domestic inflows from mutual funds and retail investors remain a powerful driver, keeping valuations elevated (~21x forward P/E) despite foreign rotation into cheaper China/HK. India’s structural growth narrative — demographics, earnings visibility, and policy continuity — remains intact, but tactically the risk is that momentum softens if global investors keep reallocating. For now, India retains its “structural overweight” crown, but upside looks capped in the near term without an earnings surprise.

🇯🇵 Japan (TOPIX: +1.78%) – Gains were broad-based as yen stabilization offered relief to exporters, while corporate reform themes (dividends, buybacks, governance improvements) continue to attract steady global allocation. Japan is evolving from a cyclical reflation trade into a “core compounder” market in global portfolios, reducing volatility but also its ability to lead the region decisively. Near term, USD/JPY remains the key swing factor, with investors watching closely for BOJ signaling on FX intervention risk.

🇰🇷 Korea (KOSPI: +1.25%) – Korea delivered a modest rebound, largely on semiconductor stabilization, but remains overshadowed by Taiwan in the global AI trade. Internet and consumer discretionary names lagged, highlighting the narrowness of gains. Foreign investors remain cautious, preferring selective hardware exporters over broad market beta. Korea sits awkwardly between Taiwan’s AI leadership and China’s domestic policy cycle, keeping it a “satellite allocation” rather than a core regional play.

🇵🇭 Philippines (PSEi: flat) – Markets stalled as hotter inflation data weighed on consumption optimism and raised the specter of tighter domestic monetary policy. The Philippines’ equity story remains highly tactical — leveraged to consumption themes — but macro disappointments quickly undermine sentiment given the limited depth of foreign participation. Without renewed consumer momentum or relief on inflation, upside remains constrained.

🇮🇩 Indonesia (FTSE Indonesia: flat) – Indonesia consolidated after a strong YTD run, with profit-taking in banks and commodity-linked names. Foreign flows paused as investors reassessed positioning after heavy inflows earlier this year. Longer-term appeal remains intact — high-yield profile, stable policy backdrop, and commodity leverage — but in the near term, the market looks fully priced. Investors appear to be waiting for the next commodity trigger or domestic policy catalyst before re-engaging.

🇹🇷 Turkey (BIST 100: -3.24%) – Turkey reversed sharply, snapping a two-month rally. The market remains retail-driven, with foreign participation thin, leaving it prone to sharp swings. While equities serve as a hedge against lira depreciation and inflation, this week highlighted how fragile that narrative is without global validation. Volatility remains a defining feature, with the BIST more a domestic macro hedge than a credible emerging-market allocation.

🇦🇺 Australia (ASX 200: flat) – Resource names held firm on signs of stabilizing Chinese demand, particularly in iron ore and base metals, but defensives and housing-related names dragged. Australia continues to trade as a geared bet on China’s construction cycle and commodity demand, leaving it hostage to developments in Beijing’s stimulus and infrastructure spending. The ASX remains rangebound until there is a decisive shift in China’s demand outlook.

🇸🇬 Singapore (MSCI Singapore: flat) – Banks stayed resilient, but REITs weakened as U.S. rate volatility pressured yield plays. Singapore continues to act as a regional “safe haven” allocation for global investors, offering defensive exposure and political stability. However, the lack of a fresh domestic growth driver limits upside, keeping Singapore more of a stabilizer in Asia portfolios than a tactical overweight.

🇦🇺 Australia (ASX 200: flat) – Commodity names steadied, but housing and defensives dragged. Market remains closely tied to China’s commodity demand cycle.

🇸🇬 Singapore (MSCI Singapore: flat) – Banks held firm, but REITs weakened on U.S. rate volatility. Acts as a defensive allocation but lacks a new growth driver.

💡 Strategic Takeaways

China gained but lagged peers – Onshore equities posted broad advances, but the CSI 300 (+1.38%) trailed Hong Kong and Taiwan. Growth segments like ChiNext and SME Innovation showed stabilization, but broad risk appetite remains selective.

Hong Kong surged – Offshore markets sharply outperformed onshore, with property and tech staging major rallies. Bargain-hunting and tactical value rotation were the clear themes, suggesting investors are testing whether Hong Kong can lead a China rebound.

Taiwan leadership – The TWSE 50 (+5.76%) dominated regional flows, with semiconductors driving momentum. Foreign inflows reinforced Taiwan’s status as the prime AI/semiconductor proxy in Asia.

India steady but stretched – India delivered respectable gains (+1.51%) but remains expensive relative to peers. Global allocators are increasingly eyeing China rotation, but India retains its structural overweight role.

Japan supported by FX – TOPIX (+1.78%) rose with a stable yen, giving exporters space to recover. Flows remain heavily dictated by USD/JPY.

Korea tentative – The KOSPI (+1.25%) bounced but continues to underperform Taiwan, reflecting investor selectivity. Korea remains a “middle ground” exposure.

ASEAN consolidation – Indonesia and Singapore were flat, while the Philippines struggled. ASEAN remains tactical rather than structural for regional investors.

Turkey volatility – BIST 100 (-3.24%) showed how fragile the retail-driven rally is, with sharp reversals underscoring lack of global support.

📰 In the News This Week

Fiscal Toolkit Reset: Bank Capital Boost & Local Debt Cleanup

Announced by: China’s Finance Ministry (FM comments + policy outline)

Date: Sept 12

Details:

FM flagged issuance of ¥500bn special bonds this year to strengthen major banks’ capital, intended to support ~¥6tn in incremental lending capacity.

Authorities highlighted progress on hidden local debt reduction during the 14th FYP, claiming over 60% of LGFVs have exited market financing.

By end-Aug, China had added ¥6tn of special bond quota, with ¥4tn already issued.

The 15th FYP fiscal agenda centers on deeper reforms, targeted support for consumption/investment, and maintaining policy flexibility.

Interpretation:

Capital top-ups bolster big-bank buffers ahead of renewed credit support to SOEs/LGFVs and priority sectors; reduces tail risk around NPL recognition.

The hidden-debt “progress” claim signals policy confidence, though investors will scrutinize LGFV spreads and swap execution for confirmation.

Execution pace of special bond issuance is positive for infrastructure demand and local-government cash flows.

Market read-through: positives for large banks, infra contractors, building materials, and SOEs; neutral-to-cautious on smaller lenders with thinner capital.

Paying the Arrears: Tackling Unpaid Local-Government Bills

Announced by: Media guidance citing senior leadership discussions

Date: Sept 11

Details:

Beijing is considering mobilizing state lenders/policy banks to extend credit to local authorities to clear a substantial backlog of arrears owed to private firms (widely discussed as ~$1T equivalent).

Framing emphasizes preventing knock-on damage to private-sector cash flow and broader employment.

Interpretation:

Clearing receivables could meaningfully ease liquidity stress for contractors, equipment makers, and service providers; improves working-capital cycles and reduces defaults in the private supply chain.

Credit risk is partially socialized to higher-quality balance sheets—near-term equity positive for upstream industrials; medium-term fiscal discipline questions remain.

US–China Engagement: Treasury’s Bessent to Meet He Lifeng in Madrid

Announced by: U.S. Treasury statement carried by media

Date: Sept 12

Details:

Treasury’s Scott Bessent to meet Vice Premier He Lifeng; agenda spans trade, economic and national-security issues, TikTok status, and AML cooperation.

Part of a European swing to Spain/UK for counterpart meetings; signals continued working-level channels.

Interpretation:

Guardrails remain in place despite strategic rivalry; incremental de-risking of headline risk for ADRs/offshore China.

Tech/platform items (data, AML, app governance) stay live issues—headline volatility possible, but dialogue itself is market-calming.

Anti-Protectionism Message at BRICS

Announced by: Remarks from President Xi

Date: Sept 8

Details:

Public call to resist protectionism and support an open global economy; emphasis on multilateralism and stable trade links.

Interpretation:

Positions China as advocate for market access amid rising trade barriers; supportive signaling for exporters and supply-chain integrators.

Rhetorical tailwind; practical gains hinge on parallel progress in bilateral talks and tariff/standards disputes.

Private Investment Push & Biomed Focus

Announced by: State Council meeting chaired by Premier Li Qiang (CCTV summary)

Date: Sept 12

Details:

Deployment of measures to “increase support,” “expand space,” and “break hidden barriers” restricting private investment.

Priority call-outs for biomedical technology development and acceleration of R&D-to-application conversion.

Interpretation:

Reinforces PPP-style pipelines and crowd-in of private capital into infrastructure, advanced manufacturing, and services.

Biomed emphasis is a sector-specific green light (R&D services, CRO/CMO, med-tech platforms), though approvals/pricing remain key sensitivities.

Social Spending Support: Childcare & Preschool Subsidies

Announced by: Finance Ministry

Date: Sept 12

Details:

¥100bn childcare subsidies allocated during the 14th FYP.

¥20bn earmarked this year for rollout of free preschool education.

Interpretation:

Signals targeted demand-side support alongside fiscal repair.

Beneficiaries: consumer services, early education, childcare operators, and indirectly staples such as infant formula/diapers.

Social-policy angle also reinforces Beijing’s theme of “inclusive growth” within the 15th FYP.

Reviving Idle Land Reserves

Announced by: Ministry of Natural Resources

Date: Sept 11

Details:

Encouragement of market-based approaches to activate idle land reserves.

Interpretation:

Aimed at improving land-use efficiency and cash generation for local governments; can unlock stalled projects and reduce carrying costs.

Property ecosystem read-through: supportive for select developers with redevelopment capability, urban renewal contractors, and building-materials volumes.

Platform Governance Watch: Xiaohongshu Summoned

Announced by: Cyberspace Administration of China (statement)

Date: Sept 11

Details:

Regulator summoned Xiaohongshu over issues described as “damaging internet ecology.”

Interpretation:

Reminder that platform governance remains an active policy lever; keeps a risk premium on content/social names.

Typically results in product/content rectification rather than structural penalties, but near-term share-price sensitivity persists for internet platforms.

Liquidity & Market-Stability Signaling

Announced by: China Securities Journal (policy commentary)

Date: Sept 8

Details:

Expert commentary flagging more active measures to maintain market liquidity and stability; discussion of a higher probability that the PBOC restarts government-bond trading operations before year-end.

Interpretation:

Messaging supports risk appetite by anchoring rates/term-premium expectations; helpful for brokers, duration-sensitive equities, and property credit channels.

Not a new tool, but indicates willingness to use balance-sheet signaling to smooth volatility.

📊 Macro Data Review – Week of Sept 8–12, 2025

This week’s macro releases highlighted stronger liquidity and credit impulse, with loan growth and TSF surprising to the upside. Inflation remained soft, with consumer prices still negative YoY and PPI deflation easing slightly. Trade data pointed to moderating exports but resilient imports, while FX reserves inched higher. The local government financing picture remains a critical backdrop, with Beijing emphasizing bond swaps and special issuance to contain hidden debt risks.

Money & Credit – Credit Impulse Returns

New Yuan Loans (Aug): CNY 590bn (cons CNY 800bn; prev -50bn) – Better than July contraction but still below consensus.

Total Social Financing (TSF, Aug): CNY 2.57tn (cons CNY 2.46tn; prev CNY 1.13tn) – Strong beat, showing robust credit impulse.

M2 Money Supply (Aug): +8.8% YoY (cons 8.7%, prev 8.8%).

M1 Money Supply (Aug): +6.0% YoY (cons 6.0%, prev 5.6%).

M0 Money Supply (Aug): +11.7% YoY (prev 11.8%).

Outstanding Loan Growth (Aug): +6.8% YoY (cons 6.9%, prev 6.9%).

Interpretation:

Credit growth has re-accelerated, with TSF strength showing that August’s liquidity push was effective. Loan issuance is still soft relative to targets, suggesting banks remain cautious, but aggregate credit demand improved. Stable M2 and stronger M1 reflect better corporate and household money circulation.

Inflation – Deflationary Pressures Persist

CPI (Aug): -0.4% YoY (cons -0.2%, prev 0.0%).

CPI (MoM): 0.0% (cons +0.1%, prev +0.4%).

PPI (Aug): -2.9% YoY (cons -2.9%, prev -3.6%).

Interpretation:

Consumer prices dipped further into deflation, underscoring weak demand. Producer prices deflated for the 18th consecutive month but at a slower pace, consistent with partial stabilisation in commodity inputs. Risks remain tilted toward entrenched low inflation unless domestic demand strengthens meaningfully.

Trade & FX Reserves – External Balance Holding

Exports (Aug): +4.4% YoY (cons +5.0%, prev +7.2%).

Imports (Aug): +1.3% YoY (cons +3.0%, prev +4.1%).

Trade Balance (Aug): $102.3bn (cons $99.2bn, prev $98.2bn).

FX Reserves (Aug): $3.322tn (cons $3.3tn, prev $3.292tn).

Interpretation:

Export growth slowed, consistent with weaker global electronics demand, while imports softened on commodity and intermediate goods. The trade surplus widened modestly. FX reserves edged higher, suggesting PBoC interventions remain controlled.

Activity Indicators

Vehicle Sales (Aug): +16.4% YoY (cons +15.2%, prev +14.7%).

Electricity Consumption (Aug): not yet released (prev +8.6% YoY).

Interpretation:

Vehicle sales momentum remains robust, confirming autos as a key policy-supported growth driver. Power demand data pending, but earlier months suggested resilient industrial usage.

Local Government Debt – Policy Backdrop

The Finance Ministry confirmed hidden local debt at ~10.5tn yuan by end-2024 and reiterated plans to use special bond quotas to manage repayment risks. A new 500bn yuan special bond issuance this year will recapitalise major banks, expected to unlock ~6tn yuan in lending capacity. Central transfers during the 14th FYP reached 50tn yuan, underscoring Beijing’s willingness to bear more fiscal burden.

Interpretation:

Beijing is signalling tighter fiscal discipline but also readiness to backstop system liquidity. Bank recapitalisation ensures credit pipelines stay open, while debt swaps aim to prevent localised defaults from spilling over. For markets, this reduces systemic risk but highlights the structural overhang of local government liabilities.

📌 Takeaway:

Macro data showed a constructive credit impulse and easing PPI deflation, but CPI weakness underscores fragile demand. External balances remain stable, FX reserves solid, and autos continue to be a growth pillar. The fiscal backdrop is evolving toward controlled risk containment, with Beijing injecting liquidity while engineering a multi-year workout of local debt. For investors, the mix points to selective stabilisation in credit-sensitive sectors (autos, property-linked supply chains) but no broad demand recovery yet.

🏢 Company News & Results

The earnings season is over, so please be on the lookout for our earnings wrap piece coming your way tomorrow (Sunday 14th of September)

Alibaba & Baidu’s AI Chips: From Trials to Training

What’s new: Both Alibaba and Baidu have begun training AI models with their own chips—partly shifting away from Nvidia. Alibaba is using in-house silicon for smaller models, while Baidu is testing its Kunlun P800 to train newer versions of ERNIE. None are fully off Nvidia yet, but this is a clear step toward supply-chain autonomy.

Why it matters:

Resilience under export curbs: Homegrown chips help mitigate U.S. restrictions on advanced GPUs, lowering procurement risk for foundation model roadmaps.

Cost/latency control: Vertical integration (especially on inference and mid-size training runs) can improve unit economics and deployment speed across cloud + consumer apps. (Inference—our read; training for cutting-edge models still favors Nvidia.)

Ecosystem lock-in: If Alibaba’s models train well on Alibaba chips (and Baidu’s on Kunlun), expect tighter coupling between their clouds, model gardens, and enterprise workloads—good for stickiness, potentially mixed for open interoperability.

Caveats & timeline:

Performance parity isn’t here for frontier-scale training; Nvidia remains preferred for the largest runs. But the bar for “good enough” keeps rising for small/medium models and inference at scale.

Expect a hybrid period (12–24 months) where internal chips shoulder specific workloads (data prep, finetunes, inference), while top-end training still rents Nvidia capacity.

Investor angle: Positive strategic optionality for BABA and BIDU (supply security + margin levers over time). Near-term P&L impact is limited; watch cloud attach, model performance benchmarks, and customer wins on in-house silicon.

Amap “Street Stars”: 40M Day-One Users, Direct Shot at Meituan

What’s new: Alibaba’s Amap launched Street Stars, an AI-driven ranking for restaurants/hotels/attractions, and drew 40 million users on day one. Amap serves ~170M DAU and paired launch with ¥1bn subsidies across 300+ cities and ~1.6M listings—a full-stack push into local lifestyle that squarely targets Meituan/Dianping.

How it works: Rankings are algorithmic (behavioral signals + reviews; some reports note Ant/Sesame data as inputs) and positioned as a non-pay-to-play “gateway” to lifestyle services from the Amap home screen.

Why it matters:

Distribution advantage: Placing curated local picks inside the default maps workflow collapses the search → decide → navigate funnel. That’s a native edge vs. app-hopping to Dianping.

Conversion economics: Coupons + navigation intent should boost in-store conversion and ad ROAS for merchants—classic two-sided marketplace flywheel.

Competitive heat: Meituan responded with a Dianping revamp and 25M extra coupons—expect a promotional arms race, and keep an eye on regulator sensitivity to price wars.

Signals of traction: Multiple outlets corroborate the 40M day-one figure and “largest food ranking platform” claim on launch-day engagement; SCMP and others report the AI-ranking push and scope (cities/listings).

Investor angle:

BABA: Strengthens the “super-app” positioning, deepens local-services moat via maps distribution; supportive for Hong Kong-listed BABA sentiment alongside ongoing ETF inflows into HK tech.

MEITUAN: Headline risk to local reviews/discovery traffic; watch share shifts in intent traffic (navigations to merchants) and promo intensity through Golden Week.

What to track next:

Sustained DAU/WAU for Street Stars post-promo; 2) merchant adoption and paid tools; 3) regulatory commentary on local-services discounting; 4) cross-sell into ride-hailing, payments, local commerce from Amap.

Hong Kong ETF Flows – Record Retail Participation

Chinese investors poured a record $26bn into Hong Kong-listed ETFs in 2025, with inflows concentrated in AI, biotech, and youth consumer themes.

Despite making up only 10% of China’s ETF market, Hong Kong ETFs attracted >50% of inflows this year, aided by Alipay access and strong performance of HSI-linked funds (up 30% YTD).

Takeaways:

Highlights strong retail appetite for Hong Kong’s thematic plays. The surge of flows has near-term technical implications for Hong Kong liquidity and could extend the relative outperformance of HSI vs. CSI 300.

Starbucks China – Sale in Final Round

Starbucks named Boyu Capital, Carlyle, EQT, and Sequoia China as final bidders for its China operations. A deal decision is expected by late October.

Takeaways:

Starbucks’ China divestment is one of the year’s largest consumer transactions. A sale to a domestic buyer would localize control, aligning with recent patterns in foreign consumer brands’ China exits. Depending on valuation, it could re-rate Chinese consumer private equity portfolios.

Hedge Fund Positioning – August Net Buying Surge

Goldman Sachs flagged that global hedge funds’ net buying of Chinese stocks in August hit the highest level since Sept 2024.

Southbound Stock Connect data show steady net inflows through early September, concentrated in tech and consumer names.

Takeaways:

While positioning remains light compared with 2021 peaks, the return of foreign hedge funds signals tentative confidence in policy support and selective sector resilience. This is a supportive flow backdrop for offshore equities.

Complete Index Performance List:

🛒 Internet & Platforms: Alibaba Leads; Meituan Holds; Trip.com Digests

Alibaba ▲ ~+15% (week) — Re-rating is earnings- and narrative-led: AI chip autonomy + Amap’s “Street Stars” traction (40m day-one users) sharpen the multi-year growth engine (cloud + local services + instant commerce).

Insight: Investors are again paying for optionality and operating discipline; China internet factor mix tilting back toward quality + revisions rather than pure value.

Baidu ▲ ~+19% (week) — Caught the AI tailwind on reports of increased use of in-house chips (Kunlun) for model training; search/ads steady, ERNIE ecosystem broadening.

Insight: The market is rewarding supply-chain resilience (less Nvidia dependence) and product cadence; multiple expansion hinges on credible model benchmarks and enterprise wins.

Tencent ▲ ~+6% (week) — Quiet compounding as ads offset gaming softness; steady buybacks.

Insight: The default OW for offshore China tech when investors want exposure without idiosyncratic blow-ups.

Meituan ▼ ~–6% (week) — Street Stars landed right in its core discovery funnel; subsidies remain elevated but the stock’s hold above lows says bearish positioning was crowded.

Insight: Tape says “bad but not worse.” For upside, the street needs a path to lower subsidy intensity without ceding share to Douyin/Amap.

Trip.com ~flat to down small — Giving back late-Aug gains despite strong prints.

Insight: Positioning clean-up, not thesis break; still a proxy on services consumption + outbound. Needs a catalyst (policy on inbound/outbound, guidance lift).

Positioning takeaway: Barbell Alibaba (growth optionality) + Tencent (defensive compounder); keep Meituan on show-me pending subsidy discipline and Amap competition; Baidu works as AI beta if product milestones keep coming; Trip.com is buy-the-dip into tourism catalysts.

🚗 Autos & EVs: Quality Bifurcation; NIO as Torque

BYD ▲ small — Scale + vertical integration keep margins resilient; export lanes stable.

Insight: Screens as quality factor in a price-war regime; relative winner on batteries + cost curve.

Xiaomi ▲ small — EV optionality continues to underpin the multiple; ecosystem execution > auto margins (for now).

Insight: Treat as a platform re-rate with EV as a call option.

NIO ▲ ~+3% (ADR) — Deliveries up, losses narrowed, cash runway intact.

Insight: High-beta lever on any EV demand stabilization; watch vehicle margin path to 16–17% and ONVO mix.

Li Auto ▼ small — Guidance trim still overhang; L-series fatigue narrative persists.

Insight: Needs i-series proof points to re-accelerate the flywheel.

Great Wall ▲ small — Better SUV/EV mix; export story (ASEAN/LatAm) still supportive.

Insight: Select share-gainer with FX/geography diversification.

Positioning takeaway: Stay with scale/vertical integration (BYD) and ecosystem rerate (Xiaomi); NIO as tactical torque; Li Auto needs product-cycle repair.

💊 Healthcare & Biopharma: Scale, Cash, and Pipelines Win

CSPC ▲ — Beat underscores pipeline breadth + disciplined execution.

WuXi AppTec ▲ — Recovery despite policy noise; global client stickiness priced back in.

Hansoh / Sino Biopharm ▼ — Rotation and profit-taking.

Insight: Flow is up the quality curve (balance sheet + late-stage assets).

Positioning takeaway: OW CSPC / WuXi as cash-generative R&D platforms; beta biotech stays event-driven.

🏦 SOEs & Financials: Yield Still Anchors, But Growth is Sparse

Banks (ICBC, BoC, CCB) ▼ ~3% — In-line but uninspiring; NIM gravity caps multiples.

Insurance mixed (AIA ▲, Ping An ~flat, China Life ▼) — Preference for capital-light models/overseas earnings shows.

Telecoms (China Mobile ▲ ~3% ) — Cash flow + dividends; AI/edge compute capex optionality.

HKEX ▲ ~1% — Turnover tailwind as HK tech outperforms; product breadth (ETFs/derivs) helps.

Insight: The yield trade remains intact; catalysts require visible policy shifts (fees/NIMs, pension flows, new products).

Positioning takeaway: Keep telcos and HKEX as dividend/liquidity anchors; banks are carry, not catalysts.

🏘 Property & REITs: Still a Drag; Only Quality Cash Flows Work

CR Mixc, China Overseas, CR Land, Link REIT ▼ — Ongoing skepticism despite supportive headlines (idle-land activation, arrears clean-up, bank recap talk).

Insight: Equity still demands hard evidence: pre-sales stabilization + funding channels + inventory digestion.

Positioning takeaway: Stay selective—tier-1 retail operators/recurring cash-flow REITs; avoid developers until funding + pre-sales improve simultaneously.

⚙️ Materials & Energy: Metals Bid; Solar Still in Shake-Out

Zijin ▲ double-digit; Hongqiao ▲ — Gold/Aluminium strength on restocking + macro hedging.

Energy SOEs mixed (CNOOC ▲, PetroChina flat, Shenhua ▼) — Stable cash machines; yield > growth.

Solar (LONGi, Tongwei soft) — Price wars persist; margin knives still falling.

Insight: Metals benefit from hedging flows and TSF beat; PV needs capacity exits or explicit policy discipline.

Positioning takeaway: Favor metals/mining as hedge + restock play; keep energy SOEs as yield ballast; avoid PV until supply response bites.

📎 Cross-currents to watch (why the tape moved):

ETF technicals: Mainland investors’ record flows into HK-listed ETFs added powerful liquidity beta to HSTECH/HSI.

Flows & positioning: Hedge-fund net buying (best since Sept ’24) + steady Southbound inflows created a supportive backdrop for offshore tech.

Product & platform wars: Amap’s “Street Stars” is structural, not just promo—puts discovery inside navigation, pressuring Meituan’s top-of-funnel.

Policy cushion: Talk of bank recap (¥500bn) and arrears cleanup reduced left-tail risk for cyclicals/financials, even if profits don’t re-rate yet.

📝 Strategic Takeaway – Week of Sept 8–12, 2025

This week extended the rotation to offshore China and tech beta: Hong Kong and Taiwan led decisively, while onshore A-shares gained more modestly. Flows and policy headlines did the heavy lifting; stock-specific leadership outperformed broad beta.

🔸 Hong Kong leadership — HSI +3.82% with strength across Commerce & Industry (+3.87%), Property (+5.30%), Finance (+3.73%), and HSTECH (+5.31%). Turnover was robust (HSI ~HK$320B Friday). Volatility edged up (VHSI +5.19% w/w) even as prices rallied—consistent with active positioning rather than complacency. Earnings and flow winners anchored the move: Alibaba up mid-teens, Tencent about +6%; Meituan down around −6% on Amap pressure; healthcare mixed (CSPC +4%, WuXi +5%).

🔸 Onshore up, but lagging — SSE +1.52%, CSI 300 +1.38%. Growth gauges outperformed: SZSE Comp +2.65%, ChiNext +2.10%, SME Innovation +2.06%, while mega-caps +1.90% and Commodity Equity +1.48%. The message is stabilization with a tilt to innovation and mid/small caps, but less punch than offshore.

🔸 Regional context — Taiwan +5.76% led North Asia on semiconductor and AI resilience; Japan +1.78% aided by a steadier yen; India +1.51% steady but expensive; Korea +1.25% a follower, not a leader; Turkey −3.24% reversed sharply. Asia ex-China had a clean risk bid.

🔸 Policy signals — The Finance Ministry outlined a ¥500B special bond for bank recap (implied ~¥6T lending capacity) and emphasized hidden-debt cleanup. Leadership discussed clearing LG arrears to private suppliers (confidence for industrial and capex chains). The State Council pushed to “expand space” for private investment with a biomed tilt. The Natural Resources Ministry encouraged activating idle land. The CAC summoned Xiaohongshu (platform governance risk premium persists). US–China: Treasury’s Bessent to meet He Lifeng next week (guardrails intact). Net effect: lower left-tail risk, targeted sector signals.

🔸 Flows and FX — Mainland investors have poured a record ~$26B YTD into HK-listed ETFs (AI, biotech, consumer themes). Hedge-fund net buying in August hit the strongest since Sept ’24, and Southbound remained positive—fuel for offshore outperformance. CNY fixing stayed tightly managed; no disorderly FX moves.

🔸 Sector tape — Internet and Platforms: Alibaba led (AI chips and Amap “Street Stars” 40M day-one users); Tencent compounded; Meituan sold off on discovery-funnel competition; Trip.com faded late-Aug strength. Autos and EVs: BYD steady on scale and vertical integration; Xiaomi bid on ecosystem rerate; NIO +3% post results (watch margin path); Li Auto softer, awaiting i-series evidence. Healthcare: CSPC and WuXi bid as investors climb the quality curve; profit-taking in Hansoh and Sino Biopharm. Materials and Energy: Zijin +double-digit, Hongqiao +3% on metals bid; energy SOEs mixed; PV margins still pressured.

⚖️ Bottom Line: Offshore Takes the Baton, Onshore Follows

Offshore China (HK) and North Asia tech set the pace, supported by powerful retail/ETF and hedge-fund flows plus policy that reduces tail risks (bank capital, arrears cleanup) without unleashing indiscriminate stimulus. Core investable themes: platform and product leadership (Alibaba, Tencent), AI and semis linkages (Taiwan leadership, Baidu optionality), SOE yield anchors (telcos, HKEX), quality healthcare (CSPC, WuXi), EV scale winners (BYD, Xiaomi), and selective metals as hedge and restock plays. The rally remains a stock-picker’s tape—offshore is where fundamentals get priced with discipline; onshore is the innovation lab catching a supportive draft.

Have a good one,

Leonid