China Weekly Wrap: Markets, Macro & Tech – Key Developments This Week

a week that was 21 - 25 April 2025

Good afternoon,

Welcome back to The China Weekly Wrap from Panda Perspectives — your digest of the key developments in China’s financial markets and macro landscape. Coming to you in the middle of Mini Marathon races, where mini Pandas are taking part all day today.

This week was a special one: Macro Week on the blog, where we dove deep into the state of China’s economy, property market, and consumer trends. If you missed it, now’s the perfect time to catch up.

Here’s what we published:

China Macro Outlook 2025: The difficult transition, the reasons for hope.

China Property: From Collapse to Calm?: A deep look at how the sector is stabilizing — and what it still lacks.

Chinese Consumption 2025: Cooling spending, persistent strength, and where the real opportunities may lie.

All three pieces are part of a broader project to build out a real, grounded framework for investing in China today. They’re available to all subscribers — but if you’re not one yet, we’d love for you to join.

Coming up next week: we shift gears into practical investment ideas coming directly out of Macro Week — sector picks, company highlights, and specific themes that we believe are best positioned for the next leg of China’s recovery. These upcoming posts will be paywalled and designed to offer clear, actionable insights for serious investors.

Serious about Asia investing? Your process needs more Panda. For those looking for personalised support — whether it’s China consumer, 2Q25 market strategy, or robotics and industrials — we’re also offering advisory calls. Learn more here or message us directly to book a time.

Reminder: Nothing in this Substack is investment advice. This content is for informational purposes only. Please do your own research or consult a licensed financial advisor before making any investment decisions. Past performance is no guarantee of future results.

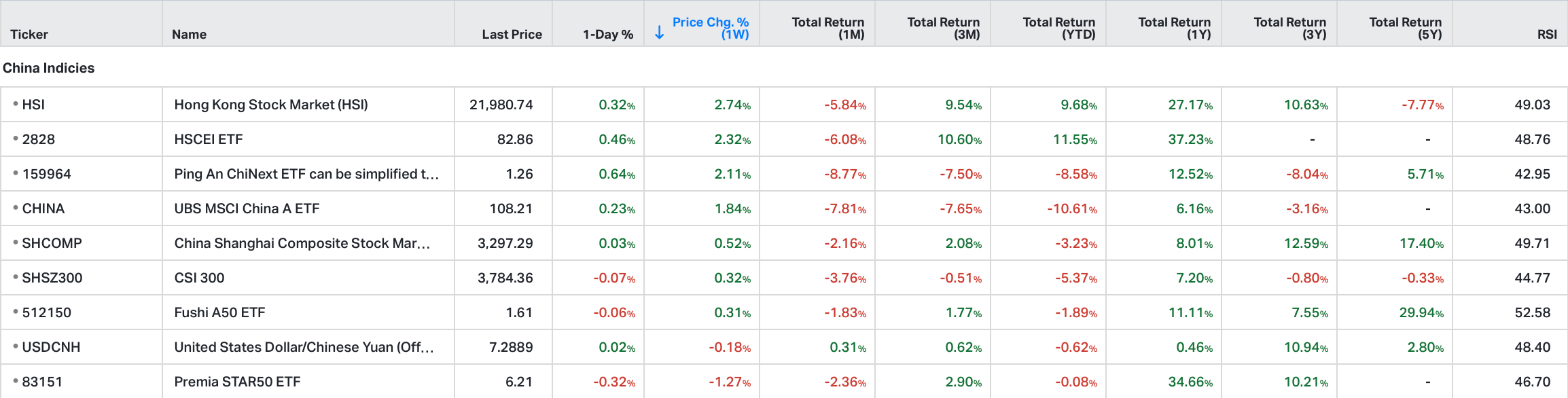

As of April 25, 2025 close of business, here’s a summary of the weekly, month-to-date (MTD), and year-to-date (YTD) performances of major Chinese and Hong Kong stock indices that we follow. We will do an end of the month reconciliation at the end of April to see whats what across a few weeks. (*see notes at the end of the post).

Weekly Relative Performance Observations

Performance in Chinese Equities

HSI (Hang Seng Index) (+2.74%)

Highlights: The HSI rose sharply, delivering one of its best weekly performances this year.

Context: Gains were broad-based, led by financials, tech, and consumer stocks. Improved sentiment around capital flows, stabilizing U.S.-China rhetoric, and strong Southbound Connect inflows supported the rally.

HSCEI ETF (2828) (+2.32%)

Highlights: The HSCEI ETF posted another strong weekly gain, tracking the broader move in Hong Kong-listed Chinese stocks.

Context: State-owned enterprises (SOEs) and financials drove returns, benefiting from re-rating hopes and improving risk appetite in offshore China names.

Shanghai Composite (SHCOMP) (+0.52%)

Highlights: The SHCOMP edged higher in a quieter week for onshore equities.

Context: Defensive sectors (industrials, utilities) outperformed, while tech and consumption remained muted. Domestic liquidity conditions remained stable but no major stimulus announcements materialized.

CSI 300 (SHSZ300) (+0.32%)

Highlights: The CSI 300 posted a modest gain, underperforming the SHCOMP.

Context: Larger cap names struggled for momentum, as investors shifted toward mid-cap and innovation names with clearer earnings visibility heading into Q2 results.

ChiNext ETF (159964) (+2.11%)

Highlights: ChiNext outperformed major A-share indices this week, reversing recent underperformance.

Context: Growth and innovation-focused stocks rebounded as investors rotated cautiously back into select healthcare, AI, and green tech sectors.

Regional Peers’ Performance

FTSE TWSE Taiwan 50 (+3.10%)

Highlights: Taiwan led regional performance this week.

Context: Strong buying in semiconductors (particularly AI-linked names) drove gains, despite ongoing concerns around U.S.-China tensions.

Hong Kong Hang Seng (+2.74%)

Highlights: Hong Kong staged an impressive recovery, nearly matching Taiwan’s performance.

Context: Rebalancing flows and better-than-expected earnings in tech and financial sectors helped lift sentiment.

TOPIX (Japan) (+2.69%)

Highlights: Japan’s TOPIX index continued its strong run.

Context: A weak yen and upbeat earnings guidance sustained inflows, particularly from global funds reallocating out of U.S. tech.

Key Takeaways for Chinese Markets

Offshore Leadership: Hong Kong equities, particularly the HSI and HSCEI, outperformed onshore markets for a second week, signaling tentative foreign investor re-engagement.

Selective Growth Rotation: The ChiNext staged a meaningful rebound, suggesting that parts of the innovation ecosystem are starting to attract bargain hunters.

Muted Onshore Gains: Mainland indices advanced, but lacked conviction without new fiscal or monetary catalysts. Defensive positioning persisted in A-shares.

Macro Week Backdrop: This week’s cautious optimism fits the broader Macro Week narrative we outlined — stabilisation is happening, but it’s fragile and selective.

In The News This Week

Macro Economy & Policy

Consumer Goods Trade-In Program Drives 720 Billion Yuan in Sales

Announced by: Chinese Ministry of Commerce

Date: April 24, 2025

Details: Over 120 million people participated in the trade-in program, boosting sales across autos and consumer durables.

This Indicates: Strong domestic demand support to counterbalance soft external demand.

China’s Renewable Energy Capacity Surpasses Thermal for First Time

Announced by: National Energy Administration of China

Date: April 25, 2025

Details: Wind and solar additions pushed renewables past thermal generation in total capacity for the first time.

This Indicates: Major milestone in China’s green transition and longer-term policy pivot.

Youth Employment Incentives and Entrepreneurship Plan Extended

Announced by: Chinese State Council

Date: April 25, 2025

Details: SOE hiring incentives extended through 2026; new 17-point plan unveiled for youth employment and entrepreneurship.

This Indicates: Stabilising the youth labor market remains a political and economic priority.

China to Broaden Free Trade Zone Reforms

Announced by: National Development and Reform Commission (NDRC)

Date: April 21, 2025

Details: Expanded FTZ reforms include autonomous vehicle pilot zones, futures market access liberalisation, and biopharma R&D “whitelists.”

This Indicates: Beijing is betting on liberalisation and innovation to counter external pressures and drive domestic competitiveness.

Steel Exports Reach Highest Q1 Levels Since 2016

Announced by: China Iron and Steel Association

Date: April 14, 2025

Details: Q1 steel exports surged to levels unseen since 2016, reflecting both strong global demand and inventory front-loading amid trade concerns.

This Indicates: Chinese manufacturers remain highly competitive, but external demand could be volatile due to escalating tariffs.

Diplomacy & External Relations

China and Indonesia Launch Strategic Dialogue Mechanism

Announced by: China’s Ministry of Foreign Affairs

Date: April 21, 2025

Details: China and Indonesia agreed to establish a comprehensive strategic dialogue mechanism covering trade, infrastructure, and regional security.

This Indicates: Strengthening ASEAN ties to hedge against decoupling pressures and deepen Belt and Road integration.

Cross-Border E-Commerce Zones Approved in 15 Cities

Announced by: State Council of China

Date: April 25, 2025

Details: The State Council approved cross-border e-commerce pilot zones in 15 cities, including Hainan, expanding digital trade infrastructure.

This Indicates: Beijing’s push to diversify export pathways amid rising global protectionism.

Trade War & U.S. Relations Update

While there were signs of tentative thawing in U.S.-China trade relations this week — with Beijing reviewing tariff exemptions and Washington floating the idea of major tariff cuts — it remains early days. Both sides are signaling a willingness to ease tensions selectively, especially in sectors like healthcare and key industrial inputs. However, given the deep structural mistrust and broader geopolitical competition, whether this opening leads to meaningful negotiations or simply tactical positioning remains to be seen. Nevertheless, for posterity lets note the important developments:

China Weighs Tariff Exemptions for U.S. Goods

Announced by: Ministry of Commerce (MOFCOM)

Date: April 25, 2025

Details: Beijing is reviewing potential tariff exemptions for U.S. goods, particularly in healthcare, chemicals, and industrial inputs.

This Indicates: Strategic selectivity in softening retaliation, targeting sectors critical to China’s economy.

Healthcare Sector Identified Early in Tariff Talks

Announced by: AmCham China

Date: April 25, 2025

Details: Healthcare was among the earliest sectors discussed for tariff review and potential exemption.

This Indicates: High priority sectors like healthcare could see faster normalization even amid broader trade tensions.

Trump Administration Considers Major Tariff Cuts

Announced by: White House (sources)

Date: April 21, 2025

Details: The Trump administration is reportedly weighing a 50–65% reduction in tariffs to create conditions for new talks.

This Indicates: Tactical signaling from the U.S. ahead of elections, but with real potential for temporary de-escalation if mutual trust improves.

China Pulls Back from U.S. Private Equity and Shifts Global Investment Focus

Announced by: Private sector sources

Date: April 21, 2025

Details: CIC and other Chinese sovereign investors are reducing U.S. exposure and reallocating capital to the UK, Saudi Arabia, and Japan.

This Indicates: A longer-term pivot in Chinese outbound investment flows, with structural implications for private capital markets.

Data Released This Week

China’s latest macro data painted a picture of resilience, with key indicators like industrial production and retail sales coming in solidly. However, deeper concerns around private sector investment, profitability, and fiscal sustainability continue to cast a shadow. Check out Macro Week at Panda Perspectives (April 21–26, 2025), where we’re digging deeper into what the numbers actually tell us about the state — and future — of China’s economy.

Loan Prime Rates (April 2025)

1-Year LPR: 3.10% (unchanged)

5-Year LPR: 3.60% (unchanged)

This Indicates:

Stable Monetary Policy: The People’s Bank of China (PBOC) kept lending rates unchanged for a second month, signaling caution despite external and internal pressures.

Focus on Targeted Support: Authorities are favoring structural tools (e.g., relending, subsidies) rather than broad rate cuts.

Limited Easing Room: Stable rates reflect concerns about RMB depreciation pressures and financial stability amid a volatile external environment.

Industrial Profits (YTD March 2025): -0.3% YoY

Slight improvement from prior readings but missed expectations of a slight return to growth (+0.1%).

This Indicates:

Profitability Remains Under Strain: Despite stronger industrial output, pricing pressures and high input costs continue to squeeze margins.

Uneven Recovery: Sectors tied to traditional heavy industry and real estate are dragging overall corporate profitability.

Policy Watch: Weak corporate profits may increase pressure for more targeted support measures, especially for SMEs and manufacturers.

Services Trade Balance (March 2025)

March Deficit: -$19.5 billion

Q1 2025 Deficit: -$58.6 billion

This Indicates:

Ongoing Services Imbalance: High outbound tourism and external services payments continue to weigh on the current account.

External Vulnerability: Services trade remains a structural drag, limiting the offset to goods surplus strength.

Auto Sector Update (Q1 2025)

Passenger Car Sales: 5.117 million units (+5.8% YoY)

New Energy Vehicle (NEV) Sales: 2.419 million units (+36.4% YoY)

This Indicates:

NEV Boom Continues: China’s EV sector remains a bright spot, outpacing overall auto market growth.

Policy Tailwinds: Subsidies, trade-in incentives, and broader industrial policy support are lifting sales.

Consumption Recovery Skewed: Big-ticket, policy-favoured sectors are recovering faster than discretionary everyday spending.

Complete Index Performance List:

General Trends

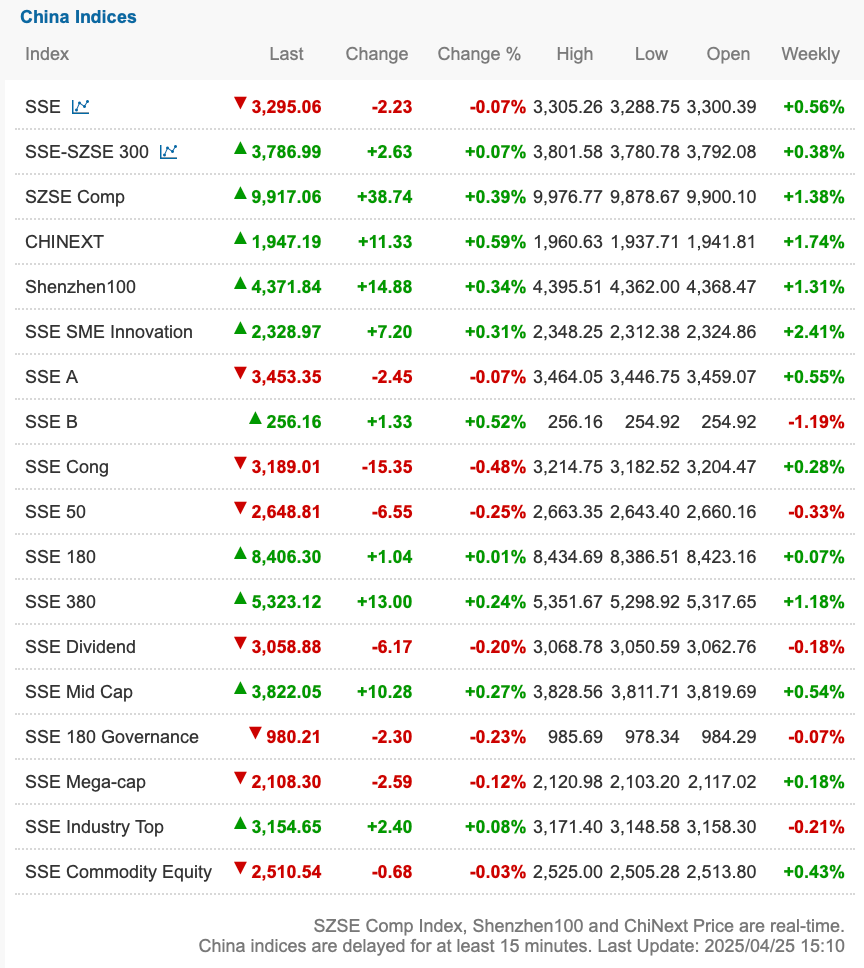

Chinese equity markets saw a broad-based rebound this week, with both mainland and Hong Kong indices closing solidly higher. The recovery was supported by stronger-than-expected macro data (retail sales, industrial production), tentative signs of stabilization in U.S.-China trade rhetoric, and targeted policy initiatives like the consumer goods trade-in program and FTZ reforms.

The Shanghai Composite Index (SSE) rose +0.56% to 3,295.06, helped by improving domestic indicators and moderately stabilizing policy expectations.

The CSI 300 Index (SHSZ300) edged up +0.38% to 3,786.99, led by financials and infrastructure-linked SOEs, although gains were modest relative to Hong Kong peers.

The ChiNext Index climbed +1.74% to 1,947.19, outperforming on the back of selective rotation into innovation and clean tech names.

In Hong Kong:

The Hang Seng Index (HSI) surged +2.74%, benefiting from foreign inflows, a softer dollar, and rising confidence in diplomatic stabilization efforts.

The Hang Seng Tech Index (HS TECH) rose +1.96%, while the Hang Seng China Enterprises Index (HSCEI)advanced +2.32%, both supported by better risk appetite.

Sector and Style Trends

Financials and SOEs Strengthened

Financial sectors (HSI FIN +2.80%) and SOE-heavy indices outperformed as investors positioned for easier liquidity conditions and a more stable regulatory environment.

Selective Growth Rebound

Innovation-linked indices like ChiNext (+1.74%) and SME Innovation (+2.41%) rose, fueled by recovering risk appetite and supportive language around technology and green industries — although fundamental earnings concerns remain.

Defensive Rotations Persisted

Utilities (HSI UTI +2.10%) and high-dividend plays attracted flows as volatility moderated but did not disappear entirely, reflecting underlying caution.

Hong Kong Led Regionally

The HSI (+2.74%) outpaced major regional peers, driven by foreign buying, lower volatility (VHSI -21.65%), and improving perceptions around capital account stability.

Key Takeaways

Macro Data Provided a Floor, but Not a Breakout

Retail sales (+4.5% YoY), industrial production (+6.1% YoY), and auto sector strength (NEV sales +36% YoY) confirmed that parts of the domestic economy are responding to stimulus. However, weak fiscal revenues (-0.7% YoY) and declining industrial profits (-0.3% YTD) suggest the foundation remains fragile. This week’s rally largely priced in resilience — not acceleration.

Trade Tensions Eased at the Margin, Improving Sentiment

Announcements of potential tariff exemptions, discussions about healthcare sector relief, and the Trump administration’s signals about halving tariffs introduced genuine albeit cautious optimism. Capital flows into Hong Kong reflected improving external confidence, though both sides remain wary.

Policy Messaging Stabilized Markets — Action Still Needed

State Council and MOFCOM measures (Trade-In program, FTZ upgrades, youth employment plans) demonstrated a more coherent policy front. Premier Li’s call for “clearer market communication” further reassured investors. Yet without new fiscal stimulus or monetary easing, follow-through risk remains high.

Capital Rotation Reflects a Defensive But Hopeful Stance

Flows concentrated in banks, insurers, SOEs, utilities, and selective tech, indicating that investors are willing to re-risk — but are still hedging against policy disappointment, external shocks, and fragile profitability.

Structure of the Rebound Matters

This was not a pure risk-on surge. The rally favored yield, infrastructure, and “policy-backed” sectors rather than broad-based speculative buying. Growthier indices (like ChiNext) outperformed mainly in quality subsectors (EVs, green tech), not speculative software or platform tech.

Final Thoughts

This week showed that China’s macroeconomic foundation is holding — just — and that policy coordination is improving compared to Q4 2024–Q1 2025.

But it also underscored the limits of sentiment-driven rallies in the absence of concrete fiscal, monetary, or regulatory action.

Investors should view the bounce as a stabilisation phase, not yet the beginning of a new bull cycle.

Top 20 Index Constituents:

Bottom 20 Index Constituents:

China’s corporate reporting season highlighted a split: innovation-driven companies (battery, travel, cloud) outperformed, while financials, commodities, and e-commerce faced persistent skepticism. Global expansion and shareholder returns emerged as key strategic themes across sectors.

Corporate News and Results this week:

CATL Unveils New High-Energy Battery Platform at Tech Day

Announced by: Contemporary Amperex Technology Co. Ltd. (CATL)

Date: April 23, 2025

Details: At its 2025 Tech Day, CATL unveiled the “Condensed Battery 2.0” platform, offering 30% higher energy density compared to current lithium-ion models. The company also announced plans to start mass production by early 2026 and revealed partnerships with leading automakers for aviation-grade battery applications.

This Indicates: CATL is reinforcing its global technology leadership in batteries, positioning itself ahead of potential domestic overcapacity concerns and intensifying international competition.

BYD Reports Record Q1 2025 Results, Confirms Global Expansion Plans

Announced by: BYD Company Limited

Date: April 25, 2025

Details: BYD posted Q1 revenue growth of +18% YoY and net profit growth of +15%, driven by surging domestic NEV sales and strong contributions from new overseas markets like Thailand and Brazil. Management reaffirmed plans to expand the “Fang Cheng Bao” and “Yangwang” brands globally, targeting higher margins through premium models.

This Indicates: BYD remains the dominant force in China’s NEV sector and is successfully executing a two-tier global expansion strategy, moving beyond volume into premiumization.

Tencent Authorizes $5 Billion Share Buyback Amidst Stable Cash Flow

Announced by: Tencent Holdings

Date: April 22, 2025

Details: Tencent’s board approved an expanded share buyback program, citing undervaluation and continued strength in its gaming and cloud businesses. The company also hinted at expanding its AI investment initiatives in H2 2025.

This Indicates: Chinese platform companies are increasingly prioritizing shareholder returns to bolster valuation and signal operational resilience despite regulatory and macro challenges.

Li Auto Q1 2025 Deliveries Rise, Export Strategy Underway

Announced by: Li Auto Inc.

Date: April 24, 2025

Details: Li Auto delivered 80,400 vehicles in Q1, up +36% YoY, and previewed plans to begin exports of the L7 and L9 models to Southeast Asia starting Q4 2025.

This Indicates: China’s premium NEV segment remains highly competitive, pushing leading players to seek growth outside the saturated domestic market.

Trip.com Posts Strong Travel Rebound in Q1 2025

Announced by: Trip.com Group

Date: April 25, 2025

Details: Trip.com reported robust recovery metrics, with domestic travel bookings up +22% YoY and outbound travel up +40% YoY, led by demand for Southeast Asian destinations.

This Indicates: China’s services recovery continues, with tourism playing an outsized role in the post-pandemic consumption rebound.

Ping An Insurance Posts Weak Q1 2025 Earnings, Flat YoY

Announced by: Ping An Insurance

Date: April 24, 2025

Details: Ping An reported Q1 EPS of 1.44 yuan, missing expectations, and flat compared to last year. Revenue rose to 256.6 billion yuan (+17% YoY), but margins remained under pressure amid a competitive life insurance market and ongoing health claims volatility.

This Indicates: China’s insurance majors continue to struggle with margin compression and slow underwriting growth, even as premium collection recovers modestly.

JD.com Faces Investor Skepticism Despite Publicity Campaign

Announced by: JD.com (founder Richard Liu personally publicized)

Date: April 24–25, 2025

Details: JD.com’s founder Richard Liu was photographed personally delivering packages as part of a morale and brand campaign during JD’s 321 Anniversary Sale event. Despite the publicity effort, JD’s stock underperformed this week amid continued concerns over competitive pressures, slowing e-commerce growth, and muted consumption sentiment.

This Indicates: Investor skepticism toward Chinese platform companies remains high, even as firms deploy aggressive branding and founder engagement efforts. Without visible margin recovery or accelerating GMV (Gross Merchandise Volume), sentiment around large-cap e-commerce remains cautious.

China Telecom Q1 Revenue Rises on Cloud and 5G Expansion

Announced by: China Telecom

Date: April 24, 2025

Details: China Telecom reported stable revenue growth driven by its cloud services division and 5G network expansion. Specific EPS and detailed figures were not highlighted, but commentary pointed to strong enterprise demand offsetting mobile ARPU softness.

This Indicates: Telecom SOEs are successfully pivoting toward cloud and enterprise services as traditional mobile revenues plateau, aligning with broader “new infrastructure” policy initiatives.

New Oriental Education Beats Expectations Amid Online Pivot

Announced by: New Oriental Education

Date: April 23, 2025

Details: New Oriental reported EPS of 0.70 yuan, slightly below consensus, but showed stronger-than-expected online education revenues and improving profitability metrics.

This Indicates: Education companies that pivoted early to online/hybrid models are stabilizing faster post-regulatory overhaul, though headwinds remain for traditional offline tutoring.

China Coal Energy Revenue Misses Expectations Despite Higher Volumes

Announced by: China Coal Energy

Date: April 21, 2025

Details: China Coal posted Q1 EPS of 0.23 yuan, missing consensus (0.53), and reported revenues of 48.99 billion yuan — well below expectations. Higher production volumes failed to offset weaker realized coal prices.

This Indicates: Commodities sectors remain under pressure from price volatility, despite strong export and production metrics early in 2025.

This week’s data, market action, and corporate results all point to a China that is stabilising, but still searching for momentum.

Macro indicators showed resilience; diplomatic signals thawed slightly; and innovation-driven sectors like batteries, NEVs, and cloud services continued to push forward.

But corporate earnings, especially in insurance, coal, and e-commerce, reminded investors that structural headwinds remain — from squeezed profitability to muted consumption sentiment.

As we move into May, the key questions remain:

Will policy follow rhetoric with real fiscal and monetary support?

Can external relations, especially with the U.S., stabilize enough to support business confidence?

And will domestic consumption broaden beyond the sectors already receiving heavy policy backing?

At Panda Perspectives, we’ll continue to track both the signals and the gaps — bringing you real-time insights into what’s working, what’s not, and where the next opportunities (or risks) are forming.

Thanks as always for reading — and stay tuned next week as we shift focus from Macro Week to practical investment ideas emerging from this evolving landscape.

Have a great weekend, it’s off to the races for us.

Regards,

Leonid

Notes:

Shanghai Composite Index (SHCOMP): Tracks all stocks (A and B shares) traded on the Shanghai Stock Exchange.

CSI 300 Index (SHSZ300): Represents the top 300 stocks traded on the Shanghai and Shenzhen Stock Exchanges.

China A50 Index (512150 CH): Comprises the top 50 A-share companies listed on the Shanghai and Shenzhen Stock Exchanges.

ChiNext Price Index (159954 CH): Focuses on innovative and high-growth enterprises listed on the Shenzhen Stock Exchange.

SSE STAR 50 Index (83151 HK): Represents the top 50 companies listed on the Shanghai Stock Exchange’s STAR Market, emphasising science and technology innovation.

Hang Seng Index (HSI): Measures the performance of the largest companies listed on the Hong Kong Stock Exchange.

Hang Seng China Enterprises Index (2828 HK): Includes major H-share companies listed in Hong Kong.

Currency Considerations:

Chinese Indices (SSEC, CSI300, China A50, CNT, STAR50): These indices are denominated in Chinese Yuan (CNY). To present their performance in USD terms, currency exchange rate fluctuations between the CNY and USD have been considered.

Hong Kong Indices (HSI, HSCEI): Denominated in Hong Kong Dollars (HKD). Their performance in USD terms reflects the HKD/USD exchange rate stability, as the HKD is pegged to the USD.