China Weekly Wrap: Markets, Macro & Tech – Key Developments This Week

a week that was 5 - 9 May 2025

Good Morning,

It’s been a tricky week—markets kept us on our toes with a mix of policy fireworks, fragile macro data, and some sharp moves in key sectors. But we’re still here, keeping pace and connecting the dots as always.

A quick personal note: I’m heading back to Hong Kong starting this week. This won’t change much in terms of coverage, but it may slightly shift the timing of posts as I settle back into the timezone and routine. Thanks in advance for your understanding—and rest assured, the flow of analysis and updates will continue as usual.

Now, on to the key developments shaping China’s markets this week.

Over the past week, we’ve zoomed in on the developers themselves—digging into balance sheets, sales trends, and what’s really happening on the ground. If you missed it, you can catch up on that work here. Its paywalled, so subscribe if you haunt already!

Looking ahead, we’re turning our attention to the next piece of the puzzle: property managers, as well as Hong Kong-listed developers and conglomerates. There’s a lot to unpack, and I’m genuinely excited about what’s coming up—stay tuned for deeper dives in the days ahead.

Serious about Asia investing? Your process needs more Panda. We full appreciate that for some this is not enough and you’d like a more personalised service that will help get results in China and Asia. Currently we’re doing calls on China consumer, 2Q25 Outlook and yes, Robotics. See what we offer here, and connect with us today or message us directly.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

Weekly Relative Performance Observations

As of April 18, 2025 close of business, here’s a summary of the weekly, month-to-date (MTD), and year-to-date (YTD) performances of major Chinese and Hong Kong stock indices that we follow. We will do an end of the month reconciliation at the end of April to see whats what across a few weeks. (*see notes at the end of the post).

Performance in Chinese Equities

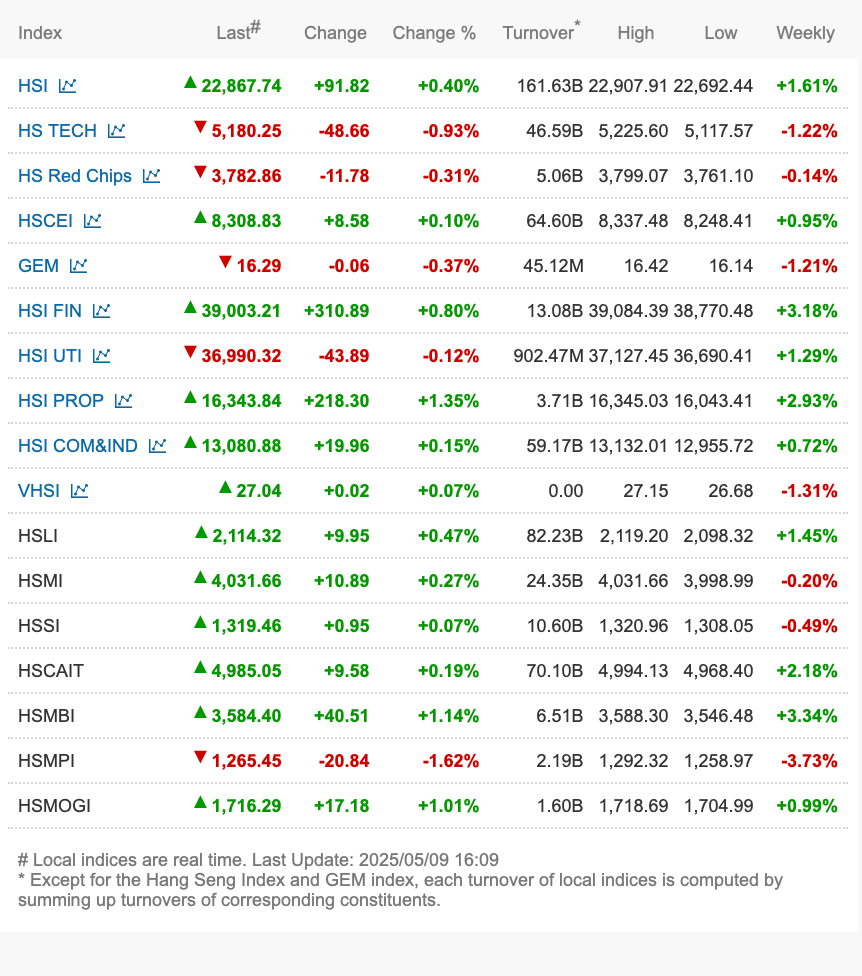

HSI (Hang Seng Index) (+1.61%)

Highlights: The Hang Seng Index gained +1.61% this week, marking its third consecutive weekly advance and continuing the rebound theme that began in April.

Context: Gains were relatively broad-based, with particular strength in property (HSI Prop +2.93%) and financials (HSI Fin +3.18%). However, tech lagged (HS Tech -1.22%), tempering overall momentum. Southbound Connect inflows remained supportive, signaling persistent offshore interest despite choppy global risk sentiment.

HSCEI ETF (2828) (+0.95%)

Highlights: The HSCEI ETF rose +0.95% this week, in line with the Hang Seng’s offshore trend.

Context: SOEs and financials were the key drivers, echoing policy optimism around dividend reforms. While gains were more muted compared to April’s strong finish, the ETF’s steady performance reflects improving confidence in offshore China plays, particularly among institutional buyers.

Shanghai Composite (SHCOMP) (+1.92%)

Highlights: The SHCOMP outperformed this week with a +1.92% gain, reversing last week’s sluggish tone.

Context: Sentiment improved as the market digested modestly positive credit data and fresh signals of policy support. Gains were led by industrials and commodity-linked plays (SSE Commodity Equity +1.81%), with broader participation lifting turnover. The move suggests tentative re-engagement by domestic investors, though conviction remains uneven.

CSI 300 (SHSZ300) (+2.00%)

Highlights: The CSI 300 rose +2.00% this week, its best showing in over a month.

Context: Financials and mega-caps helped lift the index, supported by stabilizing credit conditions and improving forward earnings revisions. The index’s rebound narrowed the year-to-date gap vs. offshore peers, but investors remain watchful for follow-through policy clarity, especially around housing.

ChiNext ETF (159964) (+2.64%)

Highlights: The ChiNext ETF outperformed with a +2.64% weekly gain, marking a sharp improvement from its recent range-bound trading.

Context: Growth and innovation sectors staged a recovery, led by healthcare and clean tech, while speculative small caps lagged. The ETF’s strength reflects a rotation back into higher-beta names as market risk appetite perked up, though pockets of fragility remain visible.

Regional Peers’ Performance

FTSE TWSE Taiwan 50 (+0.42%): Taiwan posted modest gains this week, with tech strength tempered by profit-taking after a stellar April. AI hardware names held their ground, but market turnover cooled.

TOPIX (+1.70%): Japan continued its uptrend, buoyed by industrials and exporters amid ongoing yen weakness.

BIST 100 (+2.40%): Turkey led the region this week, catching a bid on the back of easing inflation expectations and strong domestic flows.

Key Takeaways for Chinese Markets

✅ Offshore rally moderates but stays constructive: Hong Kong’s advance slowed vs. prior weeks, but the leadership baton passed to property and financials, broadening the rally’s base. Southbound Connect remains a key support pillar.

✅ Onshore sentiment improving: Both the SHCOMP and CSI 300 posted solid gains, reflecting tentative confidence returning amid better credit signals and stabilizing economic data.

✅ Growth stocks rebound: ChiNext’s sharp move higher suggests renewed risk appetite for innovation plays, though investors remain selective and focused on quality names.

✅ Property focus intensifies: With housing still at the center of policy debate, the outperformance of property indices (HSI Prop +2.93%, SSE B +2.38%) signals that investors are increasingly betting on a turnaround—though skepticism remains.

✅ Cautious optimism: The week’s gains were constructive across the board, but the market remains tightly tethered to policy expectations. Sustained momentum will likely hinge on clear evidence of housing stabilisation and further macro easing steps.

In The News This Week

Macro Economy & Policy

PBOC Rolls Out Major Monetary Policy Easing Measures

Announced by: People’s Bank of China (PBOC)

Date: May 6–7, 2025

Details:

Lowering the Reserve Requirement Ratio (RRR) by 0.5 percentage points (releasing ~1T yuan liquidity)

Structural rate cut of 25bps; 7-day reverse repo cut to 1.4%

RMB 300B re-lending for tech innovation; RMB 500B for elderly care/services

Increased capital market support tools quota to RMB 800B

Measures to reduce risk weightings for insurance company investments and support SMEs, private firms, and property-related financing.

This Indicates: A decisive shift toward monetary easing and market stabilization. Beijing appears focused on supporting credit-sensitive sectors (property, tech, SMEs) while keeping financial markets buoyed—likely in response to lingering economic softness and fragile investor confidence.

China’s Central Bank Pushes Gold Strategy: Yuan-Based Trade & Reserves

Announced by: Shanghai Gold Exchange / PBOC

Date: May 6–8, 2025

Details:

Shanghai Gold Exchange to open a Hong Kong vault to boost offshore yuan-denominated bullion trade.

China’s state gold reserves rose to $243.6B at end-April, up from $229.6B in March—the sixth straight monthly increase.

PBOC allows local banks to buy more USD to fund increased gold import quotas.

This Indicates: Clear intent to strengthen yuan’s role in commodity pricing and enhance monetary reserves amid global de-dollarization trends. Expansion of gold facilities and buying reinforces China’s hedging strategy against external shocks and currency risks.

CSRC Launches Capital Market Stabilization and Reform Measures

Announced by: China Securities Regulatory Commission (CSRC Chief)

Date: May 7, 2025

Details:

At a joint press conference with the PBOC, the CSRC unveiled a package of measures aimed at strengthening capital markets and investor confidence, including:

Supporting Central Huijin (the sovereign wealth fund arm) and the PBOC as quasi-stabilization funds to intervene if needed.

Promoting mergers and acquisitions (M&A) among listed companies to enhance corporate resilience.

Encouraging overseas listings of eligible Chinese firms and supporting high-quality companies to return to China’s mainland and Hong Kong markets.

Rolling out reform measures for tech boards and pushing new initiatives to strengthen governance and listing standards.

Vowing to forcefully promote long-term capital inflows into the A-share market, with a clear message that current market valuations are considered low by regulators.

This Indicates: A concerted effort to stabilize and deepen China’s capital markets alongside monetary easing. The CSRC’s emphasis on structural reforms (like M&A and tech board upgrades) signals that Beijing is trying to balance short-term market stabilization with longer-term capital market modernization. This also reflects sensitivity to investor sentiment and an awareness that liquidity alone won’t solve deeper confidence issues—structural credibility is key.

Beijing Accelerates Nvidia-Free AI Ecosystem Development

Announced by: Yizhuang Development Zone

Date: May 8, 2025

Details: Tens of millions of USD in subsidies announced to boost domestic AI hardware and software, targeting a fully self-reliant ecosystem worth ~80B yuan (~US$11B) by year-end.

This Indicates: Persistent focus on technological self-sufficiency, especially in semiconductors and AI, as U.S.-China tech decoupling deepens. Positive long-term for domestic chipmakers, servers, and software players, though execution risk remains.

ASEAN+3 Reinforce Financial Cooperation via Chiang Mai Initiative

Announced by: ASEAN+3 Finance Ministers and Central Bank Governors

Date: May 4, 2025

Details:

At the 28th ASEAN+3 Finance Ministers’ and Central Bank Governors’ Meeting in Milan, regional leaders reaffirmed their commitment to strengthening financial stability mechanisms. Key takeaways include:

A pledge to bolster the Chiang Mai Initiative Multilateralisation (CMIM)—the region’s multilateral currency swap arrangement designed for rapid liquidity support during crises.

Expanded cooperation with AMRO (Macroeconomic Research Office), Asian Bond Markets Initiative (ABMI), and Disaster Risk Financing Initiative (DRFI).

Introduction of new priorities for 2025, such as Promoting Fiscal Exchange, Updating Strategic Directions, and Exploring Policy Adjustment Instruments (PAI).

This Indicates: While no emergency activation of the CMIM was announced, the emphasis on enhancing rapid-response financial tools reflects regional caution amid a challenging global backdrop. The ASEAN+3 bloc is signaling its preparedness to deploy swift liquidity support if external shocks intensify—providing a confidence backstop for regional currencies and capital markets.

Diplomacy & External Relations

China–EU Relations: Dialogue and Lifting of Restrictions

Announced by: China Foreign Ministry

Date: May 7, 2025

Details:

Invitation to EU leadership for a new China-EU leaders’ meeting.

Agreement to fully lift mutual exchange restrictions between China and the European Parliament.

This Indicates: A thawing in EU-China ties, with efforts to stabilize relations despite broader geopolitical tensions. Positive signaling for trade, investment, and diplomatic normalization.

China Signals Retaliatory Action on U.S. CIA Espionage Allegations

Announced by: China Foreign Ministry

Date: May 7, 2025

Details: Beijing vowed countermeasures following reports of U.S. infiltration and sabotage.

This Indicates: Geopolitical friction remains elevated. While largely rhetorical for now, underlines risks of further deterioration in U.S.-China relations—an overhang for sensitive sectors like tech.

China–U.S. Trade Tensions: Talks Continue Amid Rising Frictions

Announced by: Multiple sources (China MOFCOM, U.S. officials)

Date: Week of May 6–10, 2025

Details:

China’s Ministry of Commerce reiterated its call for the removal of unilateral U.S. tariffs as a precondition for meaningful progress in trade negotiations.

Despite tough rhetoric, senior Chinese and U.S. officials are meeting this weekend in Switzerland to maintain a dialogue channel. Notably, the U.S. delegation does not include Peter Navarro, a figure associated with hardline China policy.

On the ground, trade flows remain resilient—Chinese exporters report continued shipments to U.S. buyers,even as tariffs bite.

This Indicates:

Tensions remain high, but the absence of Navarro from the Switzerland talks could be seen as a slight softening of tonefrom the U.S. side—possibly aiming to preserve room for compromise. China’s messaging remains firm, positioning tariff removal as non-negotiable, yet both sides appear keen to avoid a total breakdown in talks.

Markets will likely interpret these developments as keeping the status quo intact: ongoing trade frictions with no immediate breakthrough, but also no sharp escalation in the near term.

Data Released This Week

China’s latest economic data delivered a mixed picture: external strength remained a bright spot, while domestic inflation stayed soft, underscoring continued challenges in reviving consumption and private-sector vitality. The trade sector once again did much of the heavy lifting, but lingering deflationary pressures highlight persistent demand weakness at home.

Trade Balance (April 2025)

Exports YoY: +8.1%

Imports YoY: -0.2%

Trade Surplus: $96.18B (vs. $102.64B previous)

This Indicates: Exports outperformed expectations (consensus: +1.9%), fueled by front-loaded orders—particularly to ASEAN and Latin America—as buyers raced to lock in shipments ahead of looming tariffs. Imports continued to contract, albeit at a slower pace than March’s -4.3% reading, reflecting sluggish domestic demand. The narrower trade surplus points to some pressure on the external cushion, but overall, exports remain a vital growth engine.

Foreign Exchange Reserves (April 2025)

Actual: $3.282T

Previous: $3.241T

Consensus: $3.2T

This Indicates: China’s FX reserves rose more than expected, marking a continuation of cautious reserve building. The increase reflects a combination of valuation effects (stronger gold prices, FX dynamics) and ongoing efforts to fortify financial buffers amid global uncertainties.

CPI (April 2025)

YoY: -0.1% (unchanged from March)

MoM: +0.1% (vs. -0.4% in March)

This Indicates: China remains in mild deflation on a year-over-year basis, with headline CPI down 0.1% YoY for the second consecutive month. However, the +0.1% month-on-month increase marks a meaningful turnaround after March’s -0.4% drop—suggesting that price pressures may be starting to bottom out. Core CPI (excluding food and energy) rose 0.5% YoY, indicating tentative stabilization in underlying demand.

While the overall picture still reflects weak domestic demand, the April CPI rebound is an encouraging early sign that monetary easing and fiscal stimulus may be gaining traction at the margins. A few more months of positive sequential gains would help confirm that deflationary pressures are easing and that China’s consumption engine is slowly regaining momentum.

PPI (April 2025)

YoY: -2.7% (vs. -2.5% in March)

Consensus: -2.6%

This Indicates: Factory-gate deflation deepened slightly, pointing to persistent margin pressures in upstream sectors. This underlines the challenges facing China’s industrial core, particularly as global commodity prices moderate and domestic construction/infrastructure demand remains patchy.

Current Account (Q1 2025 Preliminary)

Actual: $165.6B

Previous: $163.8B

Consensus: $110.0B

This Indicates: China’s current account surplus stayed robust in Q1, thanks to resilient goods trade and solid services exports. The stronger-than-expected figure provides a financial cushion that can help offset capital outflows or FX volatility, supporting broader macro stability.

SHFE Warehouse Stocks (Weekly to May 9, 2025)

Copper: -8,602T (-9.63%)

Aluminum: -6,192T (-3.52%)

Zinc: -1,375T (-2.84%)

Lead: +2,718T (+5.81%)

Nickel: -867T (-3.02%)

Tin: -190T (-2.13%)

Rubber: -170T (-0.08%)

This Indicates: A significant drawdown in copper and aluminum inventories suggests firm physical demand in key industrial metals, likely linked to pre-tariff restocking and infrastructure-linked consumption. The rise in lead stockpiles is an outlier, possibly reflecting short-term shifts in battery-sector demand.

Jan–April Goods Trade (Yuan-Denominated)

Total trade: +2.4% YoY

Exports: +7.5% YoY

Imports: -4.2% YoY

This Indicates:

Cumulative trade figures reinforce April’s picture: exports continue to outperform, but the import contraction deepens the narrative of weak domestic appetite. ASEAN remains China’s largest trading partner, with trade volume up 9.2% YoY—highlighting regional diversification away from U.S.-centric flows.

Summary:

April’s data confirmed external demand as China’s main growth lever, with exports continuing to beat expectations despite tariff headwinds. However, deflationary signals from CPI and PPI—paired with soft imports—underscore the fragility of domestic recovery. With both monetary easing and capital market reforms now rolling out, policymakers are clearly attempting to re-anchor expectations, but durable improvement will hinge on reviving consumer and private-sector sentiment.

Complete Index Performance List:

Performance Analysis

General Trends

Chinese equity markets posted a broadly stabilizing performance this week, with offshore indices leading and onshore sentiment showing cautious improvement. Investors digested a flood of policy measures—headlined by the PBOC’s major easing package and CSRC’s capital market stabilization push—while also watching inflation data and global trade dynamics.

The divergence between Hong Kong and mainland indices narrowed modestly this week, as onshore indices benefited from fresh liquidity injections and offshore markets extended gains on improving sentiment.

Shanghai Composite Index (SSE): +1.92% to 3,342.00

CSI 300 Index (SHSZ300): +2.00% to 3,846.16

ChiNext Index: +3.27% to 2,011.77

Notably, the ChiNext outperformed, reflecting stronger risk appetite for tech and healthcare plays as policy focused on innovation and capital market support.

In Hong Kong:

Hang Seng Index (HSI): +1.61% to 22,867.74

HS Tech Index (HS TECH): -1.22% to 5,180.25

HSCEI Index: +0.95% to 8,308.83

The Hang Seng built on its recent rebound, but the Tech Index lagged, as investors rotated from speculative internet names into more defensive and policy-favored sectors like property and financials.

Sector and Style Trends

Financials & Property Outperformed

Financials were strong across the board, supported by PBOC’s credit easing and CSRC’s push for market stabilization. Property indices also gained ground:

HSI PROP: +2.93%

HSI FIN: +3.18%

For instance, China Resources Land (1109.HK) rallied +2.62% for the week, and Longfor Group (0960.HK) gained +2.04%, reflecting growing optimism around property sector backstops.

Selective Growth Strength

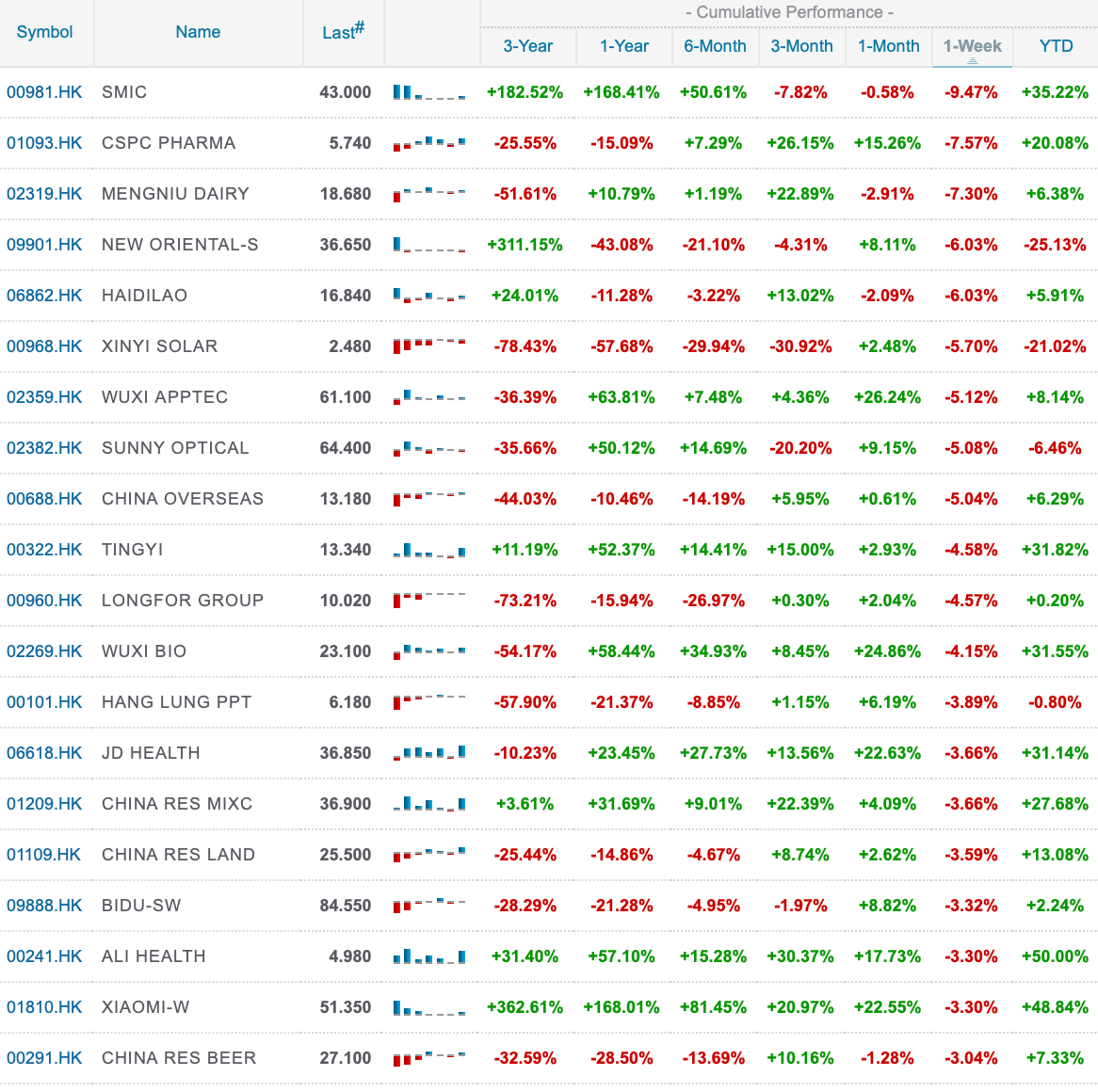

The ChiNext (+3.27%) and SME Innovation Index (+3.31%) outshone mainland peers, bolstered by tech and healthcare plays. Names like Wuxi AppTec (2359.HK) (+7.48%) and JD Health (6618.HK) (+5.22%) highlighted selective risk-taking in innovation sectors, spurred by government messaging around tech self-sufficiency.

Defensive Rotations Persisted

Utilities and consumer staples saw steady interest, as caution lingered after weak inflation data. Nongfu Spring (9633.HK) rose +5.96%, and Hengan Intl (1044.HK) gained +5.42%—a reflection of investors maintaining exposure to stable cash flow generators.

Top & Bottom Performers (Select Highlights)

Strong Weekly Performers (among major HK names):

Techtronic Industries (0669.HK): +5.89%

Nongfu Spring (09633.HK): +5.96%

Wuxi AppTec (2359.HK): +7.48%

JD Health (6618.HK): +5.22%

China Resources Beer (291.HK): +7.33%

These gains underline interest in high-quality growth and defensive consumption.

Weak Weekly Performers:

Sunny Optical (2382.HK): -6.46%

Meituan (3690.HK): -7.05%

Haidilao (6862.HK): -6.03%

Xinyi Solar (968.HK): -5.08%

Hengan Intl (1044.HK): -0.45% (despite a weekly gain, it lagged sector peers)

These moves reflect profit-taking and selective risk-off trades in names that had rallied previously or remain exposed to external volatility.

Key Takeaways

✅ Policy Support Drove Sentiment:

The combined monetary and capital market measures were the clear drivers of market confidence. PBOC’s easing cycle and CSRC’s stabilization messaging reinforced the idea that Beijing is determined to backstop market stability.

✅ Selective Risk-On in Growth:

While tech names in Hong Kong saw mixed performance, A-share growth indices like ChiNext showed signs of leadership, with healthcare and green tech catching bids—especially following Xi’s AI ecosystem push.

✅ SOE & Property Focus Strengthened:

Banks, insurers, and property developers outperformed as dividend reform and capital support measures encouraged rotational flows into these state-backed sectors.

✅ Hong Kong Remained the Offshore Sweet Spot:

Even with tech headwinds, the HSI and HSCEI held gains thanks to resilient foreign inflows and optimism around ADR repatriation and governance reforms.

Final Thoughts

This week marked a subtle but important shift in tone: from defensive stabilization to cautious optimism, as investors began to reward policy-aligned sectors and quality growth stories. While breadth remains a challenge—evidenced by lagging cyclicals and tech beta—there are clearer signs of capital creeping back into risk assets, especially offshore.

For investors, the roadmap remains clear: favor policy-favored sectors (banks, property, SOEs), maintain exposure to selective growth (healthcare, green tech), and be mindful of the onshore-offshore divergence as liquidity and sentiment continue to evolve.

Corporate News and Results this week:

SMIC Delivers Blowout Q1 Profit, But Shares Slide on Revenue Miss and Cautious Outlook

Announced by: Semiconductor Manufacturing International Corp (SMIC)

Date: May 8, 2025

Details: SMIC posted explosive Q1 2025 results, with net profit rocketing 12,766% YoY to US$396 million and revenue up 28.4% YoY to US$2.25 billion. Mobile chips (24.2% of sales) and consumer/home appliances (40.6%) led growth, while wafer output reached a record 2.29 million units. Gross margin stayed robust at ~22.5%. However, revenue came in below analyst estimates (US$2.25B vs. US$2.35B consensus), and Q2 guidance flagged a 4–6% sequential revenue dip with margin compression to 18–20%.

Market Reaction: The market responded sharply negatively—SMIC shares fell nearly 7% in Hong Kong trading, as investors digested the revenue miss and management’s tepid near-term outlook. OnCNBC analysts and traders noted that while profit figures were headline-grabbing, they reflected favourable base effects, and the guidance suggested peak cycle risks and ongoing headwinds from export restrictions.

Implications: SMIC’s results highlight its pivotal role in China’s semiconductor ambitions, but the stock reaction underscores market skepticism over sustainability. Investors appear increasingly focused on structural growth clarity, margin durability, and geopolitical risks, rather than headline profits alone. The revenue miss also signals that even domestic champions are not immune to broader macro and cyclical challenges.

Nvidia to Release Downgraded H20 AI Chip in China

Announced by: Nvidia

Date: May 9, 2025

Details: Nvidia will launch a downgraded version of its H20 AI chip for China by July, following U.S. export restrictions on the original model. The new chip features reduced memory capacity to comply with export controls.

Implications: This shows Nvidia’s commitment to retaining China market share despite tightening U.S. export curbs. The move also highlights Beijing’s continued vulnerability in high-end AI hardware, reinforcing the strategic push for domestic semiconductor independence.

Huawei to Launch HarmonyOS Laptop on May 19

Announced by: Huawei

Date: May 8, 2025

Details: Huawei will unveil its first laptop powered by its self-developed HarmonyOS on May 19. This is part of its broader strategy to reduce reliance on U.S. software ecosystems.

Implications: The launch marks a key milestone in Huawei’s localization drive and signals deepening decoupling trendsin tech, though HarmonyOS adoption beyond Huawei’s own ecosystem remains limited.

Apollo and CAR Inc. Partner for Autonomous Car Rentals

Announced by: Apollo (Baidu) & CAR Inc.

Date: May 8, 2025

Details: Baidu’s Apollo unit and CAR Inc. announced a pioneering autonomous car rental service, allowing users to book self-driving vehicles for cultural sites and tourist spots.

Implications: This collaboration strengthens Apollo’s push into commercial autonomous mobility and broadens Baidu’s footprint beyond robotaxis, targeting mass-market adoption.

Bank of China HK Tops Expectations in Q1

Announced by: Bank of China HK (3988.HK)

Date: May 5, 2025

Details: The bank posted Q1 EPS of 0.21 (vs. 0.19 consensus) on revenue of HK$145.04B, beating forecasts. Net interest income was robust, reflecting rate tailwinds.

Implications: Results reinforce SOE financial strength amid credit easing policies and confirm the bank’s defensive appeal for investors seeking yield and policy alignment.

Mixed Results for Semiconductor Players: GigaDevice & Goodix

Announced by: GigaDevice Semiconductor (603986.CH), Shenzhen Goodix (603160.CH)

Date: May 6, 2025

Details: GigaDevice missed Q1 EPS estimates (0.35 vs. 0.44 consensus), while Goodix beat expectations with 0.42 EPS (vs. 0.37 consensus), signaling mixed momentum across China’s fabless chip landscape.

Implications: Highlights the uneven nature of recovery in China’s semiconductor sector, with market leadership increasingly determined by innovation and downstream positioning.

Wanhua Chemical Beats on Profit, Showcases Resilience in Specialty Chemicals

Announced by: Wanhua Chemical (600309.CH)

Date: May 5, 2025

Details: Wanhua Chemical delivered solid Q1 results, with EPS of 0.98 beating the consensus of 0.95 and showing strength in core MDI (methylene diphenyl diisocyanate) operations. Revenue came in at RMB 43.07 billion, slightly below expectations but offset by disciplined cost control and stable margins.

Implications: The performance highlights Wanhua’s market leadership in specialty chemicals, with robust domestic demand and diversification into downstream polyurethane products cushioning external pressures. Analysts pointed to its resilient earnings model, even as global demand remains uneven. Investors are watching closely for signals on expansion projects and international pricing power.

Hengli Petrochemical Posts Stable Results, Balancing Revenue Dip with Margin Strength

Announced by: Hengli Petrochemical (600346.CH)

Date: May 5, 2025

Details: Hengli reported Q1 revenue of RMB 57.04 billion, modestly below the RMB 59.37 billion consensus, reflecting softer-than-expected output from its refining segment. EPS came in at 0.29 (vs. 0.35 consensus), as downstream polyester and chemical fibers held up better than refining and petrochemical margins.

Implications: The results underscore Hengli’s integrated business model, which helps absorb shocks in any single segment. While its refining margins face headwinds from fluctuating crude spreads and export pressures, the company continues to benefit from vertical integration and steady domestic polyester demand. Going forward, Hengli’s capital allocation toward high-value-added materials and its flexibility to pivot in volatile markets will be key themes to monitor.

This week’s market action, data releases, and corporate updates painted a familiar picture: China remains on a fragile path of stabilization, with promising signals but still lacking the breakout momentum that investors are hoping for.

We saw policymakers step up their efforts — from the PBOC’s major monetary easing package to the CSRC’s new measures aimed at bolstering capital markets. These moves sent a strong message of intent, and offshore markets in particular responded positively, with Hong Kong extending its outperformance over mainland peers for yet another week.

Innovation-linked sectors — semiconductors, clean energy, and AI-adjacent tech — continued to capture the imagination (and capital) of investors, boosted by both SMIC’s blowout profit (despite the market’s sobering reaction) and high-profile product news from Huawei and Baidu. Yet, core macro data — like trade and inflation — reminded us that the recovery remains uneven, with consumer demand and manufacturing momentum still facing headwinds.

Corporate earnings across sectors like chemicals (Wanhua, Hengli), banks, and tech reinforced a key theme: while operational resilience is evident, visibility on sustained growth is less certain, and cautious forward guidance is tempering enthusiasm.

As we move deeper into May, a few pivotal questions remain:

Will China’s latest easing measures translate into real economy traction, or are they more about shoring up market sentiment?

Can Hong Kong’s offshore rally maintain its momentum, especially as global headwinds (tariffs, geopolitics) loom?

And is this selective rebound in growth sectors the start of a broader rotation, or just a policy-driven flash in the pan?

At Panda Perspectives, we’re keeping a close eye on these shifts — not just the headlines, but the underlying market dynamics that will shape risk and opportunity through mid-year and beyond.

Thanks as always for reading and for your continued trust. Stay tuned next week as we dive deeper into property managers, Hong Kong conglomerates, and the evolving landscape of China’s post-COVID capital markets.

Have a great weekend — and here’s to keeping the stamina up for the next stretch.

Best,

Leonid

Notes:

Shanghai Composite Index (SHCOMP): Tracks all stocks (A and B shares) traded on the Shanghai Stock Exchange.

CSI 300 Index (SHSZ300): Represents the top 300 stocks traded on the Shanghai and Shenzhen Stock Exchanges.

China A50 Index (512150 CH): Comprises the top 50 A-share companies listed on the Shanghai and Shenzhen Stock Exchanges.

ChiNext Price Index (159954 CH): Focuses on innovative and high-growth enterprises listed on the Shenzhen Stock Exchange.

SSE STAR 50 Index (83151 HK): Represents the top 50 companies listed on the Shanghai Stock Exchange’s STAR Market, emphasising science and technology innovation.

Hang Seng Index (HSI): Measures the performance of the largest companies listed on the Hong Kong Stock Exchange.

Hang Seng China Enterprises Index (2828 HK): Includes major H-share companies listed in Hong Kong.

Currency Considerations:

Chinese Indices (SSEC, CSI300, China A50, CNT, STAR50): These indices are denominated in Chinese Yuan (CNY). To present their performance in USD terms, currency exchange rate fluctuations between the CNY and USD have been considered.

Hong Kong Indices (HSI, HSCEI): Denominated in Hong Kong Dollars (HKD). Their performance in USD terms reflects the HKD/USD exchange rate stability, as the HKD is pegged to the USD.