Indexing in China

Not as easy as it sounds

Major Chinese Indices - basic facts you wanted to know but were afraid to ask.

As we are on the preface of a relaunch of this column as Panda Perspectives, with a focus on deeper thought and guidance on investing in China, I wanted to continue from where the previous post left off.

We have established that China’s financial markets are diverse and expansive, that trade across a number of different exchanges. This has implications for indexing as you can imagine. The holy grail for any country is to create an S&P500 - an index broad enough to cover a large part of the market, easy to follow and replicate. This unfortunately isnt that easy in China, as different indices find it hard to go cross border. Tencent, with its main listing in Hong Kong for example is not included in the A-share indices. Nor are any of the US lists ones. At the same time, HK-based indices such as the HSI or the HSCEI are run by Hang Seng, who are very trigger happy and change the index composition surprisingly frequently. Not that thats necessarily a bad thing, but medium-term momentum becomes a feature of stock selection, which isn’t always welcome.

I wanted to prove a starting point for anyone interested in this, but feels uncomfortable asking basic question. This post explores the representative sector breakdown and list of top holdings of these major Chinese indices, along with key observations on their economic and sectoral focuses.

Hang Seng Index (HSI)

The Hang Seng Index (HSI) is a key measure of the Hong Kong stock market, composed of around 80 (currently 82, but this varies - see what I mean about momentum and being trigger happy!) large companies, including both Hong Kong and mainland Chinese firms. The HSI is highly weighted towards Financial Services (37.8%), followed by Consumer Discretionary (15.6%) and Technology (12.4%). Its top holdings, such as AIA Group (8.9%), HSBC Holdings (8.2%), and Tencent Holdings (7.8%), underscore the strong influence of both global and Chinese finance within the Hong Kong economy. With a broader sector diversity and a balanced array of industries, the HSI reflects the economic interplay between Hong Kong and mainland China.

Top 5 Holdings (representative over 5 years)

AIA Group (8.9%)

HSBC Holdings (8.2%)

Tencent Holdings (7.8%)

Alibaba Group (6.4%)

China Construction Bank (5.8%)

Hang Seng China Enterprises Index (HSCEI)

What if you dont want the HK financial sector to dominate you china holdings, but still like the HK valuations? This is where HSCEI comes in. It is the Hang Seng China Enterprises Index (HSCEI) and it represents the 50 largest H-share companies from mainland China listed on the Hong Kong Stock Exchange. Its sector composition shows a notable concentration in Financial Services (32.5%), Consumer Discretionary (17.8%), and Technology (15.4%), reflecting the growth sectors within the Chinese economy. Notably, Tencent Holdings (8.2%) and Meituan (7.4%) hold the top spots, with a mix of financial institutions like China Construction Bank and Industrial & Commercial Bank of China also represented. This index provides a robust snapshot of the Chinese corporate presence in Hong Kong, appealing to investors who seek exposure to key economic players within mainland China.

Top 5 Holdings

Tencent Holdings (8.2%)

Meituan (7.4%)

China Construction Bank (6.8%)

Alibaba Group (6.5%)

Industrial & Commercial Bank of China (5.9%)

CSI 300

The CSI 300 Index is a primary institutional benchmark for the mainland Chinese market, composed of the largest 300 A-shares on the Shanghai and Shenzhen exchanges. The index favors Financial Services (28.4%) but also features a significant allocation to Consumer Staples (14.6%) and Industrials (13.8%), reflecting China’s core industries. The top holdings include Kweichow Moutai (5.8%) and Contemporary Amperex Technology (CATL) (4.2%), emphasizing the influence of high-demand consumer goods, especially in sectors like liquor, which is traditionally valued by Chinese investors. The CSI 300 serves as a representative measure for institutional investors seeking broad exposure to China’s established economic base.

Top 5 Holdings

Kweichow Moutai (5.8%)

Contemporary Amperex Technology (4.2%)

China Merchants Bank (3.1%)

Wuliangye Yibin (2.8%)

Ping An Insurance (2.4%)

Shanghai Composite Index (SHCOMP)

The Shanghai Composite Index (SHCOMP) captures the entirety of the Shanghai Stock Exchange, including over 2,000 companies. Financial Services constitute the largest sector (31.2%), with Industrials (16.4%) and Materials (11.8%) also making up substantial portions. Kweichow Moutai (4.2%) is a key holding, and major financial institutions like Industrial & Commercial Bank of China and China Merchants Bank are also prominent. The SHCOMP reflects the traditional economic foundation of China, with financial and industrial sectors forming its core, giving it an appeal for those interested in the broader Chinese economy.

Top 5 Holdings

Kweichow Moutai (4.2%)

Industrial & Commercial Bank of China (3.1%)

China Merchants Bank (2.8%)

Agricultural Bank of China (2.6%)

Bank of China (2.4%)

Shenzhen Component Index

Known for its growth-oriented composition, the Shenzhen Component Index focuses on technology-driven and innovative companies. The index’s heaviest sector is Technology (24.6%), followed by Industrials (18.2%) and Healthcare (12.4%). Leading companies include Contemporary Amperex Technology (CATL) (5.6%) and Ping An Bank (3.2%), reflecting Shenzhen’s role as China’s innovation and tech hub. The Shenzhen Component Index offers an ideal lens into the rapidly evolving and growth-oriented sectors of China’s economy, catering to investors with an interest in China’s technology and industrial advancements.

Top 5 Holdings

Contemporary Amperex Technology (5.6%)

Ping An Bank (3.2%)

Midea Group (2.8%)

BYD Company (2.6%)

Wuxi Apptec (2.4%)

ChiNext

The ChiNext board, also listed on the Shenzhen Stock Exchange, is often compared to the NASDAQ as it focuses on high-growth companies within technology and innovation. Technology constitutes the largest sector (32.8%), followed by Healthcare (18.6%) and Industrials (15.4%). Its top holdings include Contemporary Amperex Technology (CATL) , East Money Information and Wuxi Apptec. ChiNext is a major attraction for investors interested in China’s emerging tech landscape and innovative enterprises, as it reflects the country’s growing focus on tech and high-value industries. Ironically you also get WENS the pork farmers in it, but thats Chinese indexing for you.

Top 5 Holdings on average.

Contemporary Amperex Technology (8.4%)

East Money Information (3.2%)

Wuxi Apptec (2.8%)

Mindray Bio-Medical (2.6%)

Shenzhen Inovance Technology (2.4%)

KWEB (KraneShares CSI China Internet ETF)

The KraneShares CSI China Internet ETF (KWEB) is a U.S.-listed ETF designed to track leading Chinese internet companies. Its sector composition is dominated by Consumer Discretionary (45.2%) and Communication Services (32.6%), a breakdown that underscores the ETF’s focus on the Chinese internet and e-commerce sector. The top holdings—PDD Holdings (12.4%), Tencent Holdings (11.2%), and Alibaba Group (9.8%)—illustrate KWEB’s high concentration in digital giants that are central to China’s tech-driven consumer economy. This is obviously an ETF ragtag than an index, but it is a popular choice for those wanting exposure to the Chinese digital landscape without navigating mainland or Hong Kong markets directly, so I feel compelled to include it.

Top 5 Holdings

Meutian (10.8%)

Tencent Holdings (10.2%)

Alibaba Group (9.83%)

JD.com (7.26%)

PDD holdings (6.82%)

Some of the main takeaways for me:

1. High Concentration in KWEB: The KWEB ETF’s top holdings represent a significant share of the fund, creating a highly concentrated exposure to China’s internet sector. This can appeal to investors focused on digital growth but also introduces higher risk due to limited diversification.

2. Dominance of Financials in Traditional Indices: Both the SHCOMP and CSI 300 indices show a strong weighting in traditional financial stocks, highlighting the role of financial institutions in stabilizing China’s broader economy.

3. Consumer Staples Influence in CSI 300: The CSI 300’s notable allocation to consumer staples, particularly liquor companies like Kweichow Moutai, illustrates the demand for established brands in China’s domestic market.

4. Tech-Heavy Focus in Shenzhen and ChiNext: Both the Shenzhen Component Index and ChiNext lean heavily towards technology companies, catering to investors interested in China’s innovation economy. These indices represent some of China’s fastest-growing sectors.

5. Diverse Sector Representation in Hong Kong Indices: The HSCEI and HSI indices are more diversified across sectors compared to mainland indices, reflecting Hong Kong’s unique position as a global financial centre with exposure to both international and mainland Chinese companies.

Once you consider performance, you’ll see that directionally the indices diverge quite dramatically. Clearly the ChiNext has stood out from the others, and perhaps wiht good reason. Is this the QQQ for China going forward? Well QQQs but with pork farming… Lets look at the valuations:

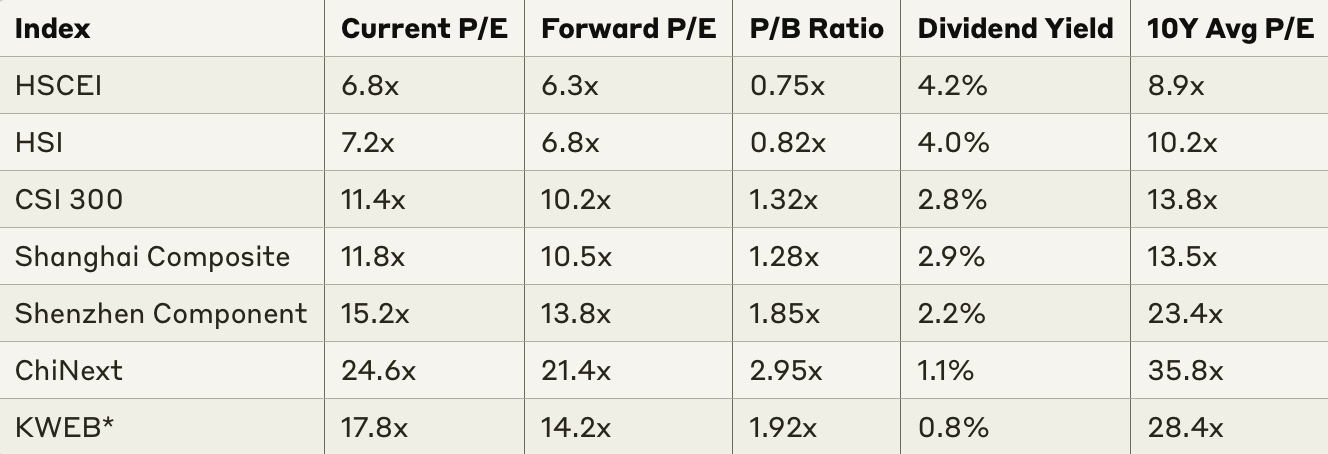

The current valuation landscape of Chinese indices reveals a clear gradient, where traditional indices such as the Hang Seng China Enterprises Index (HSCEI) and the Hang Seng Index (HSI) generally carry lower valuations than growth-oriented indices like ChiNext. This valuation disparity aligns with the nature of these indices, as traditional indices tend to include more established sectors such as financial services, whereas growth indices are heavily weighted towards technology and innovation, which often command higher valuations.

Another notable feature of Hong Kong-listed shares is their higher dividend yields compared to mainland counterparts. This is particularly evident in indices like the HSCEI and HSI, which include more mature, dividend-paying companies that attract income-focused investors. This dividend appeal differentiates these Hong Kong indices from mainland Chinese indices, which are typically more growth-focused with lower dividend distributions.

Moreover, growth and tech-focused indices such as ChiNext and the Shenzhen Component Index are currently trading at larger discounts to their historical averages. an aftermath of a significant market correction within China’s technology sector.

Across the board, all major Chinese indices are trading at valuation multiples lower than those of global developed markets. When people talk about China being very cheap, they are referencing being both cheap historically and cheap relatively to other places around the world. This is another pillar of why I believe in the ability of the Chinese market other outperform the rest of the world, and in turn the reason for me writing this column at all.

So what’s an investor to do? Where is the alpha? is there alpha? with so many indices what is even Beta? Those are complicated questions and many people have been trying to figure out the right answer. To me the lack of a 1 size fits all index makes it a great market to run DIY portfolios. Doing best ideas, or at the very least kicking out clear losers would be my choice.

Going forward I shall be providing the subscribers of this column my view of best opportunities in China, themes to be exposed to and best plays both large and small cap. I am very excited for it, and as previously teased teh CATL piece is dropping on Tuesday the 29th!

This overview of the indices is incredibly helpful. Thanks. Do you think you could also include their closest ETF equivalents in future pieces?

Is the Star 50 similar to Chinext but a little more pure tech play?