Indonesia 2025: Turning the Corner on Growth

From Trade Shocks to Noodle Stocks: Can Jakarta Hit 8% Without the Chaos of Its EM Peers?

Good Morning,

At Panda Perspectives, we go beyond headlines. No seriously, we do try! Our mission is to deliver deep, data-driven insights into Asia’s most dynamic economies whil being grounded in original research, sectoral understanding, and hard macro truths. Quite often we’ve been accused of bias in favour of China or their leadership. We hasten to assure you that we are transparent, and even if we’re off the mark, at the very least you can be certain that that position has been developed without a pre-existing bias and/or favouritism.

Having established that, we reiterate our view on China - its going to do well out of the current predicament, for reasons we’ve listed before - RMB and asset prices up, as part of a multi year trend. However some people cant participate, and the question we seem to be getting quite a bit is what of those who can not for whatever reason buy China is this day and age? Well a) we’re sorry, and b) fret not, help is on the way, for here’ is a discussion of what would be out second favourite Asian market. A study in Sacrlet-and-White if you will, yes, we’re looking at Indonesia!

This report is our most comprehensive macro case study to date: At 16,000 words, it’s a full-spectrum analysis of Southeast Asia’s largest economy—unpacking what’s held it back, what’s changing under the new administration, and why Indonesia may now offer one of the most intriguing “clean growth” stories in the emerging markets universe.

This report is, as most of our macro work is fee to read, enjoy and share. It will be followed up by a paywalled review of actual stock ideas in Indonesia. Do subscribe to enjoy that.

Serious about investing in Asia? Then your process needs more Panda.

We get it, for some readers, a Substack alone isn’t enough. If you’re looking for sharper insights, personalised feedback, or just someone to help you cut through the noise in China and Asia, we also offer bespoke research calls and strategy sessions.

Right now, we’re working with clients on China’s consumer landscape, the 2Q25 macro outlook, robotics and now the broader Asian landscape including ASEAN and north Asia.

See what we offer here, and connect with us today or message us directly.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

Let’s dive in.

The Indonesia Proposition: Pro-Growth Economics Without the Complexity

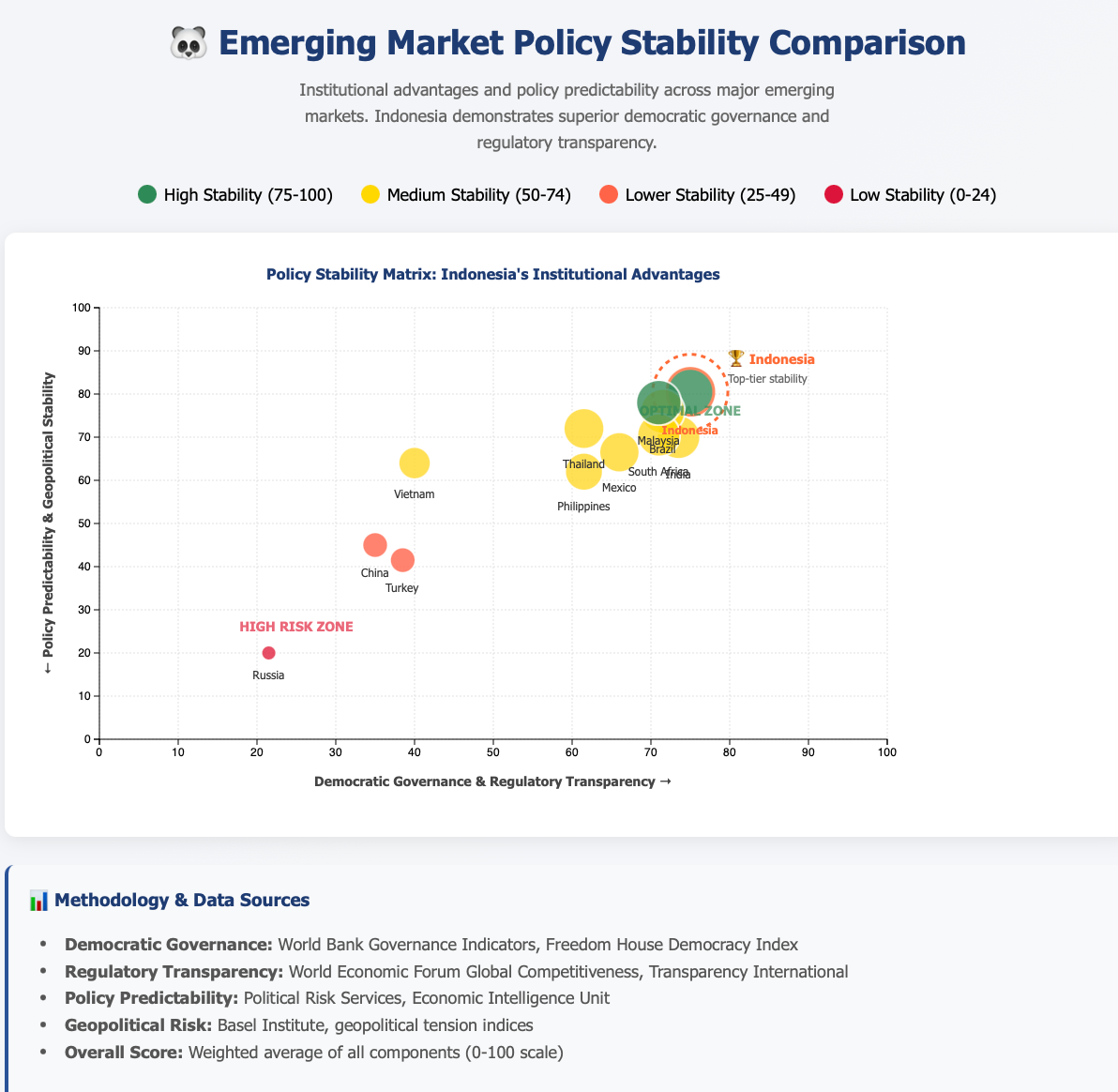

For economists and investors who appreciate the theoretical appeal of aggressive government spending programs and pro-growth fiscal policies but are concerned about the regulatory unpredictability and structural complexities that characterize other major emerging markets, Indonesia presents a compelling case study. The archipelago nation offers many of the same macroeconomic dynamics that have historically attracted attention to larger emerging economies, but within a framework of greater policy transparency, democratic governance, and reduced systemic risks.

Indonesia’s current economic moment represents a unique convergence of pro-growth policy commitment and structural stability. President Prabowo Subianto’s administration has articulated an ambitious 8% GDP growth target supported by substantial fiscal expansion—including an additional Rp300 trillion in government spending—while operating within institutional frameworks that provide greater predictability than many emerging market peers. This combination offers exposure to government-led growth dynamics without the regulatory volatility, geopolitical complications, or structural debt concerns that complicate analysis of other major emerging economies.

The macroeconomic parallels are instructive: both Indonesia and larger emerging market economies feature substantial domestic markets, government-directed infrastructure investment, and policy frameworks aimed at accelerating economic development. However, Indonesia’s democratic institutions, transparent policy-making processes, and absence of major geopolitical tensions create a more stable analytical framework for understanding long-term economic trajectories and policy sustainability.

From a macroeconomic perspective, Indonesia’s current position offers researchers and analysts an opportunity to examine pro-growth emerging market policies in an environment with reduced external complications. The country’s economic challenges and recovery dynamics provide insights into emerging market resilience, policy effectiveness, and structural transformation without the analytical complexity introduced by regulatory uncertainty or geopolitical risk factors that characterize other major emerging economies.

Executive Summary

Indonesia’s economy stands at a critical inflection point in 2025, emerging from a period of relative underperformance that has characterized much of the post-pandemic recovery. After experiencing its slowest growth in over three years with Q1 2025 GDP expansion of just 4.87%, the archipelago nation is showing early signs of economic stabilization and potential recovery. The confluence of moderating inflation, resuming monetary easing, currency stabilization, and improving consumer sentiment suggests that Indonesia may finally be approaching the “better days” that analysts have long anticipated.

The economic underperformance of recent years can be attributed to a complex web of external headwinds and domestic structural challenges. Global trade tensions, commodity price volatility, elevated interest rates, and currency pressures have constrained growth momentum. However, the fundamental strengths of Indonesia’s economy—its massive domestic market, young demographics, and resilient consumer base—remain intact and are beginning to reassert themselves as external conditions normalize.

Table of Contents

1. Introduction: The Indonesian Economic Landscape

2. The Anatomy of Underperformance: Understanding the Challenges

3. External Headwinds: Global Forces Constraining Growth

4. Domestic Structural Impediments

5. Monetary Policy Constraints and Currency Pressures

6. Signs of Recovery: Emerging from the Trough

7. Consumer Sector Resilience and Normalization

8. Policy Response and Structural Reforms

9. Investment Climate and Capital Formation

10. Regional and Global Context

11. Outlook and Recovery Trajectory

12. Conclusion: Positioning for the Next Growth Cycle

1. Introduction: The Indonesian Economic Landscape

Indonesia, Southeast Asia’s largest economy and the world’s fourth most populous nation, has long been viewed as one of the region’s most promising growth stories. With a population exceeding 285 million people, abundant natural resources, and a strategic position in global trade routes, the archipelago nation possesses the fundamental ingredients for sustained economic expansion. However, the post-pandemic period has presented a series of challenges that have tested the resilience of Indonesia’s economic model and highlighted both its strengths and vulnerabilities.

The Indonesian economy’s performance in recent years can best be characterized as a tale of unfulfilled potential. While the country successfully navigated the immediate health and economic crises of the COVID-19 pandemic, the subsequent recovery has been marked by persistent headwinds that have prevented the economy from returning to its pre-pandemic growth trajectory. The 4.87% year-over-year GDP growth recorded in the first quarter of 2025 represents the slowest expansion in more than three years, falling short of both government targets and market expectations.

This underperformance becomes particularly stark when viewed against Indonesia’s historical growth patterns, regional peer comparisons, and the government’s ambitious growth aspirations. Throughout the 2000s and early 2010s, Indonesia consistently delivered GDP growth rates in the 5-6% range, driven by robust domestic consumption, commodity exports, and infrastructure investment. The current growth trajectory, while positive, reflects a significant deceleration from these historical norms and suggests that structural and cyclical factors have combined to constrain the economy’s natural dynamism.

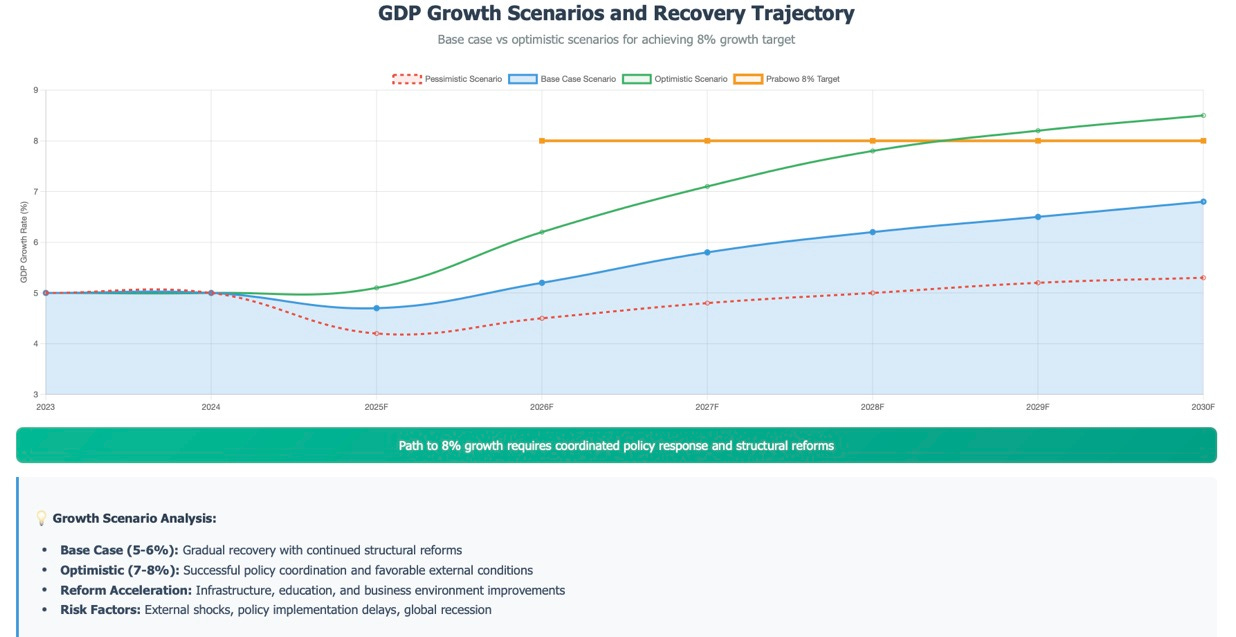

The gap between current performance and aspirations is further highlighted by President Prabowo Subianto’s stated goal of achieving 8% annual GDP growth during his administration. This ambitious target was first articulated during his presidential campaign, notably at the Qatar Economic Forum in May 2024, where he expressed confidence that Indonesia could achieve this level within two to three years of his administration. “I am very confident. I’ve discussed with experts and studied the numbers. I am sure we can easily reach 8 percent. I am determined to surpass it,” he declared at the forum.

The president has consistently reiterated this commitment throughout his campaign and early presidency. At the launch of the One 2.0 Map Policy Geoportal in July 2024, he mentioned that he had even jokingly placed a bet with ministers from a friendly country, promising them a fine dining experience if the 8% growth target is achieved. Most recently, in January 2025 at the National Meeting of the Indonesian Chamber of Commerce and Industry (Kadin), he reaffirmed his optimism, stating: “I believe and I am convinced, that we will achieve, or perhaps even exceed, eight percent growth.”

This 8% growth objective represents a substantial acceleration from current levels and underscores the government’s recognition that Indonesia’s economic potential remains significantly underutilized. The target reflects both the administration’s confidence in Indonesia’s long-term prospects and the urgency of addressing the structural and cyclical constraints that have limited economic performance in recent years. Notably, this growth rate was last achieved by Indonesia in 1996, making it a particularly ambitious benchmark.

Achieving this 8% growth target would require addressing multiple challenges simultaneously, including improving infrastructure, enhancing regulatory efficiency, boosting investment rates, and maintaining macroeconomic stability. According to experts from the Prabowo administration’s team, reaching this target would necessitate an additional budget of approximately Rp300 trillion in government spending to stimulate the economy, along with significant increases in investment and exports beyond the current consumption-driven growth model. The target also implies the need for significant productivity improvements and structural reforms that can unlock Indonesia’s demographic dividend and natural resource advantages more effectively.

The roots of this underperformance are multifaceted, encompassing both external shocks and domestic policy challenges. Global trade tensions, particularly the escalating US-China trade war and its spillover effects, have created an uncertain environment for export-dependent economies like Indonesia. The imposition of reciprocal tariffs by the United States, including a 34% tariff on Indonesian goods, has added another layer of complexity to the external environment, even though Indonesia’s direct exposure to US markets is relatively limited compared to regional peers.

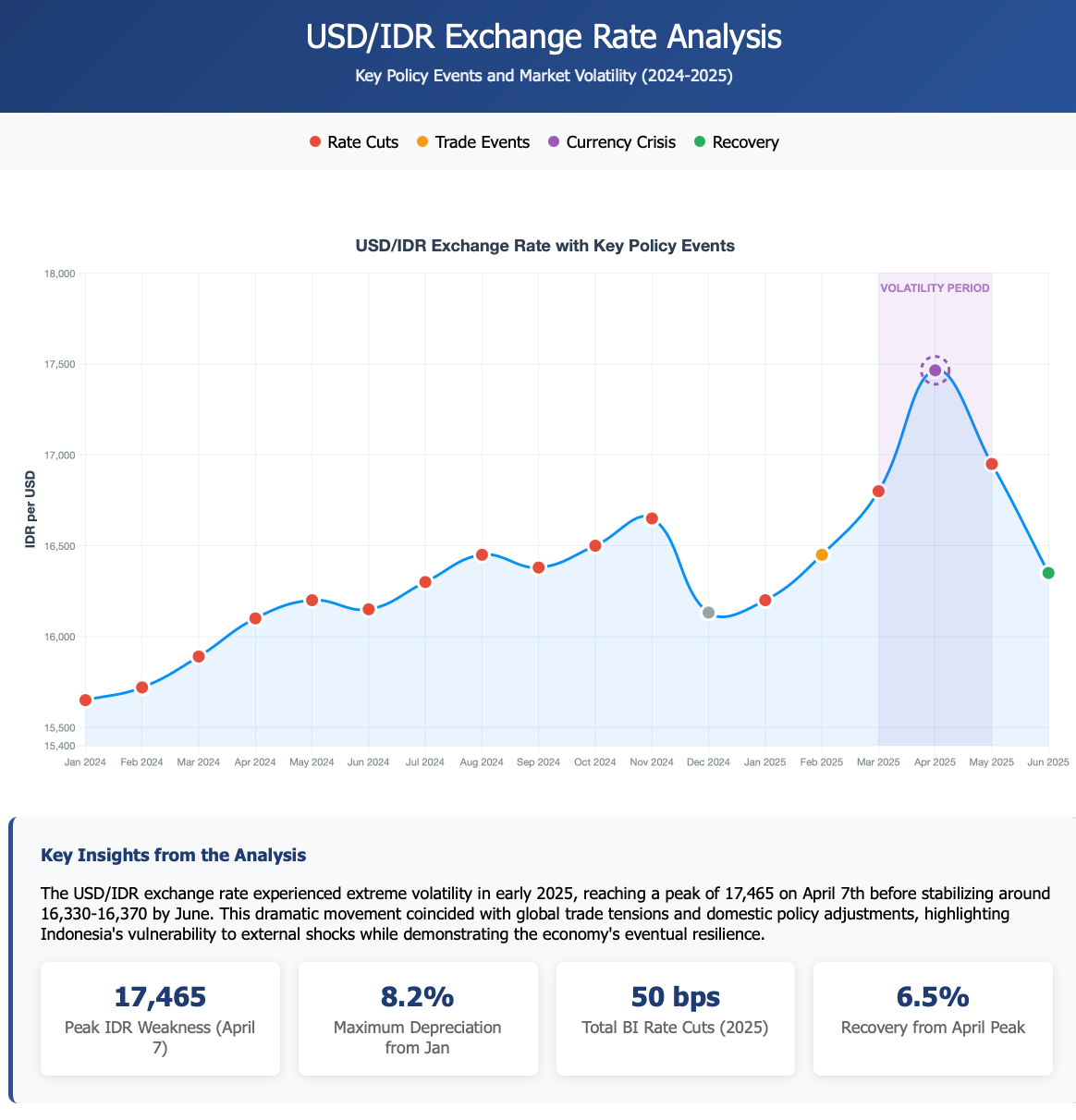

Domestically, Indonesia has grappled with the challenge of maintaining macroeconomic stability while supporting growth. The central bank’s monetary policy has been constrained by the need to defend the rupiah against external pressures, limiting the scope for aggressive easing that might otherwise support domestic demand. Currency volatility, reaching extreme levels with the rupiah touching 17,465 against the US dollar in early April 2025, has created additional headwinds for an economy heavily dependent on imported inputs across key sectors.

However, beneath these near-term challenges lies a more fundamental story of structural transformation and long-term potential. Indonesia’s economy is undergoing a gradual shift from its traditional reliance on commodity exports toward a more diversified, consumption-driven model. This transition, while creating short-term adjustment costs, positions the economy for more sustainable and resilient growth in the medium to long term.

The domestic market, with its massive scale and growing middle class, represents Indonesia’s greatest economic asset. Household consumption accounts for more than half of GDP, providing a natural buffer against external shocks and a foundation for sustained growth. The resilience of this domestic demand base has been evident even during the recent period of slower growth, with household consumption maintaining positive growth rates despite external pressures.

The demographic profile of Indonesia further reinforces its long-term growth potential. With a median age of approximately 30 years and a large working-age population, the country is well-positioned to benefit from the demographic dividend that has powered economic growth across Asia. This young, increasingly urbanized population is driving demand for consumer goods, financial services, and digital technologies, creating new growth opportunities across multiple sectors.

Infrastructure development, a key priority of successive Indonesian governments, has made significant strides in recent years. The completion of major projects, including new airports, ports, and transportation networks, has begun to address some of the logistical constraints that have historically limited economic efficiency. These investments are starting to pay dividends in terms of improved connectivity between Indonesia’s far-flung islands and reduced costs for businesses operating across the archipelago.

The financial sector, while still developing, has shown remarkable resilience and growth potential. Banking sector penetration remains relatively low, particularly in rural areas, suggesting significant room for expansion as financial inclusion initiatives gain traction. The rise of digital financial services and fintech platforms is accelerating this process, bringing banking services to previously underserved populations and supporting broader economic inclusion.

As we examine the current economic landscape, it becomes clear that Indonesia is at a critical juncture. The challenges of recent years have tested the economy’s resilience and exposed areas requiring structural reform and policy attention. However, the fundamental drivers of long-term growth remain intact, and early indicators suggest that the economy may be beginning to emerge from its period of relative underperformance.

The following sections will explore in detail the factors that have contributed to Indonesia’s recent economic challenges, analyze the emerging signs of recovery, and assess the prospects for a return to more robust growth. Through this comprehensive examination, we aim to provide a nuanced understanding of Indonesia’s economic trajectory and the opportunities and risks that lie ahead.

2. The Anatomy of Underperformance: Understanding the Challenges

Indonesia’s economic underperformance in recent years cannot be attributed to a single factor but rather represents the culmination of multiple interconnected challenges that have constrained the country’s growth potential. To understand the current economic landscape and assess the prospects for recovery, it is essential to dissect these various impediments and examine how they have interacted to create the current environment of subdued growth.

The most immediate manifestation of this underperformance is evident in the GDP growth trajectory. The 4.87% year-over-year expansion recorded in the first quarter of 2025 represents a significant deceleration from the 5.02% growth achieved in the fourth quarter of 2024 and falls well short of the government’s full-year target of 5.2%. This growth rate, while positive, is the slowest recorded in more than three years and highlights the persistent headwinds facing the Indonesian economy.

The underperformance becomes even more pronounced when viewed in historical context. Throughout the 2000s and early 2010s, Indonesia consistently delivered GDP growth rates in the 5-7% range, establishing itself as one of Asia’s most dynamic emerging economies. The current growth trajectory represents a significant departure from these historical norms and suggests that both cyclical and structural factors have combined to constrain economic momentum.

One of the most significant contributors to this underperformance has been the weakness in investment activity. Gross fixed capital formation, a critical driver of long-term economic growth, has struggled to regain momentum following the pandemic-induced disruption. The uncertainty surrounding global trade policies, regulatory changes, and currency volatility has made businesses more cautious about committing to large-scale investment projects. This investment hesitancy has created a vicious cycle, where weak investment leads to slower productivity growth, which in turn constrains the economy’s overall growth potential.

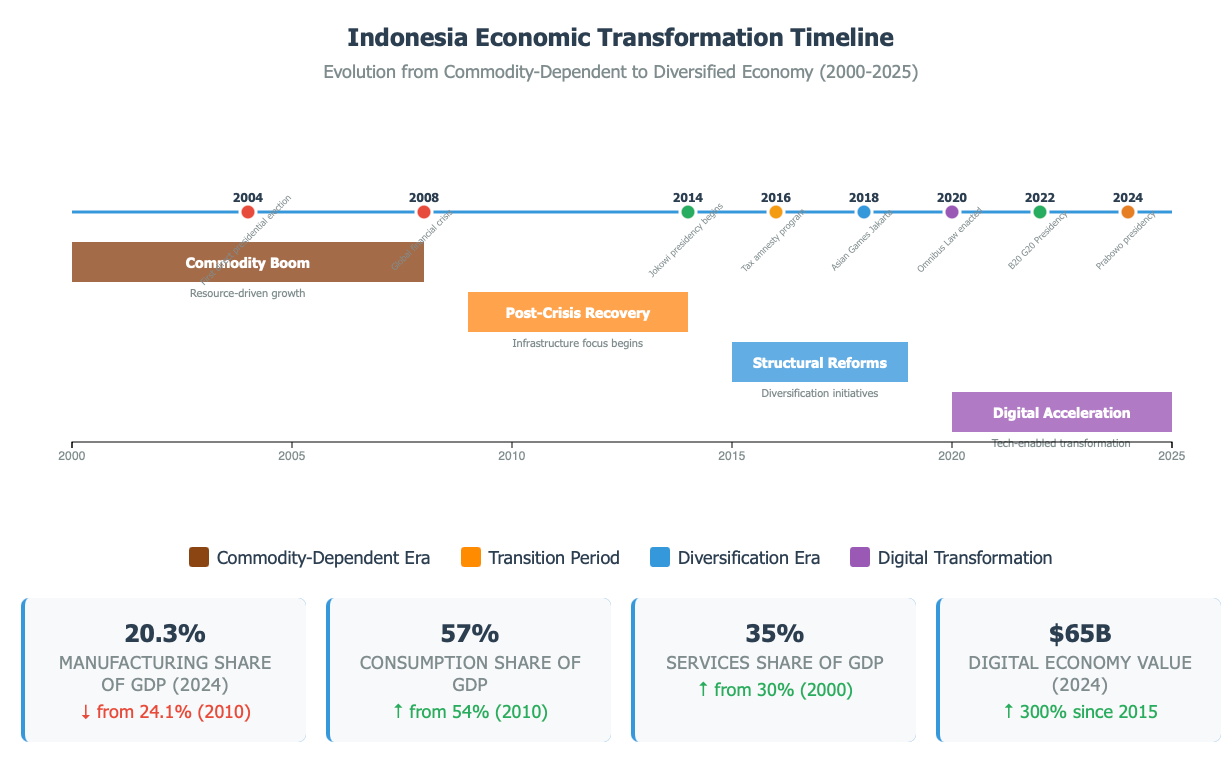

The manufacturing sector, traditionally a key engine of Indonesian economic growth, has faced particular challenges. The sector’s contribution to GDP has been on a declining trend since 2010, reaching just 20.3% in 2024. This deindustrialization trend reflects both global competitive pressures and domestic structural challenges. Rising labor costs, infrastructure constraints, and regulatory complexity have made it increasingly difficult for Indonesian manufacturers to compete with lower-cost regional alternatives, particularly in labor-intensive industries.

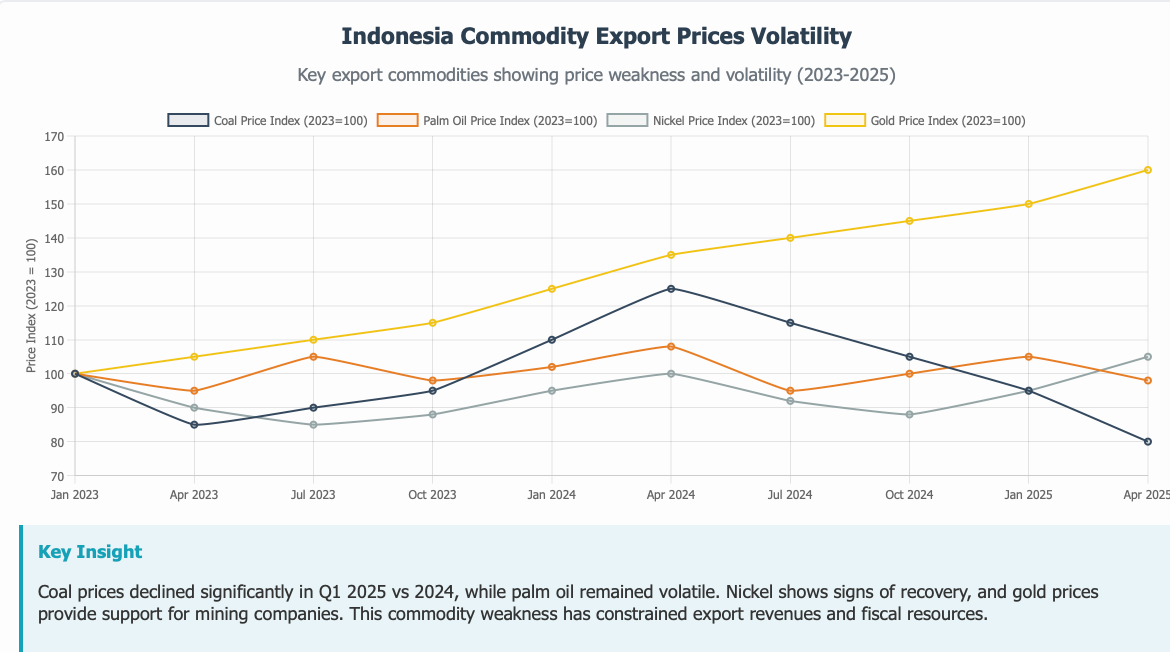

The export sector has also been a source of weakness, reflecting both global demand conditions and Indonesia’s commodity-dependent export structure. The country’s heavy reliance on coal, palm oil, and other primary commodities has made it vulnerable to global price volatility and demand fluctuations. Coal prices, in particular, were significantly lower in the first quarter of 2025 compared to the same period in 2024, directly impacting export revenues and government fiscal resources.

Palm oil, another critical export commodity, has faced its own set of challenges. Environmental concerns and sustainability requirements in key export markets have created additional compliance costs and market access barriers for Indonesian producers. While these pressures are driving necessary improvements in production practices, they have also created short-term adjustment costs that have weighed on sector performance.

The services sector, while more resilient than manufacturing and commodities, has not been immune to the broader economic challenges. Tourism, a significant contributor to services GDP and foreign exchange earnings, has struggled to fully recover from the pandemic-induced collapse. While domestic tourism has shown signs of recovery, international visitor arrivals remain well below pre-pandemic levels, constraining the sector’s contribution to overall economic growth.

Labor market dynamics have also contributed to the underperformance narrative. While unemployment rates have remained relatively stable, underemployment and informal sector employment continue to be significant challenges. The quality of employment, rather than just the quantity, has become a critical issue, with many workers trapped in low-productivity, low-wage occupations that limit their contribution to overall economic growth.

The productivity challenge extends beyond the labor market to encompass broader issues of economic efficiency and competitiveness. Total factor productivity growth, a key measure of an economy’s ability to generate output from its inputs, has been disappointing in recent years. This reflects a combination of factors, including inadequate infrastructure, regulatory inefficiencies, and limited technology adoption across many sectors of the economy.

Infrastructure constraints, while improving, continue to pose challenges for economic efficiency and growth. Despite significant government investment in infrastructure development, gaps remain in key areas such as logistics, digital connectivity, and energy supply. These constraints increase the cost of doing business and limit the economy’s ability to fully capitalize on its geographic advantages and market size.

The regulatory environment has also been a source of concern for businesses and investors. While the government has made efforts to streamline regulations and improve the ease of doing business, bureaucratic complexity and regulatory uncertainty continue to create barriers to investment and business expansion. The implementation of new regulations, while often well-intentioned, has sometimes created unintended consequences that have constrained business activity.

Financial sector development, while progressing, has not kept pace with the economy’s financing needs. Access to credit, particularly for small and medium enterprises, remains constrained by conservative lending practices and limited financial inclusion. The banking sector’s risk-averse approach, while prudent from a stability perspective, has limited the flow of credit to productive sectors of the economy.

The fiscal position, while generally stable, has also constrained the government’s ability to provide countercyclical support during periods of economic weakness. The need to maintain fiscal discipline and debt sustainability has limited the scope for aggressive fiscal stimulus, even as the economy has struggled with subdued growth.

Currency volatility has added another layer of complexity to the economic challenges. The rupiah’s weakness against major currencies, particularly the US dollar, has increased the cost of imported inputs and created inflationary pressures that have constrained both business investment and consumer spending. The extreme volatility experienced in early 2025, with the rupiah reaching 17,465 against the dollar, highlighted the economy’s vulnerability to external shocks and capital flow reversals.

These various factors have combined to create an environment where Indonesia’s natural economic dynamism has been constrained. The economy’s fundamental strengths—its large domestic market, young demographics, and abundant natural resources—remain intact, but their full potential has not been realized due to these multiple headwinds.

Understanding this complex web of challenges is crucial for assessing the prospects for economic recovery. As we will explore in subsequent sections, many of these constraints are beginning to ease, creating the conditions for a potential return to more robust growth. However, addressing the structural impediments will require sustained policy effort and continued reform momentum to unlock Indonesia’s full economic potential.

3. External Headwinds: Global Forces Constraining Growth

The Indonesian economy’s recent underperformance cannot be fully understood without examining the significant external headwinds that have shaped the global economic environment in recent years. As an open economy with substantial trade linkages and exposure to international capital flows, Indonesia has been particularly vulnerable to the series of global shocks and policy shifts that have characterized the post-pandemic period.

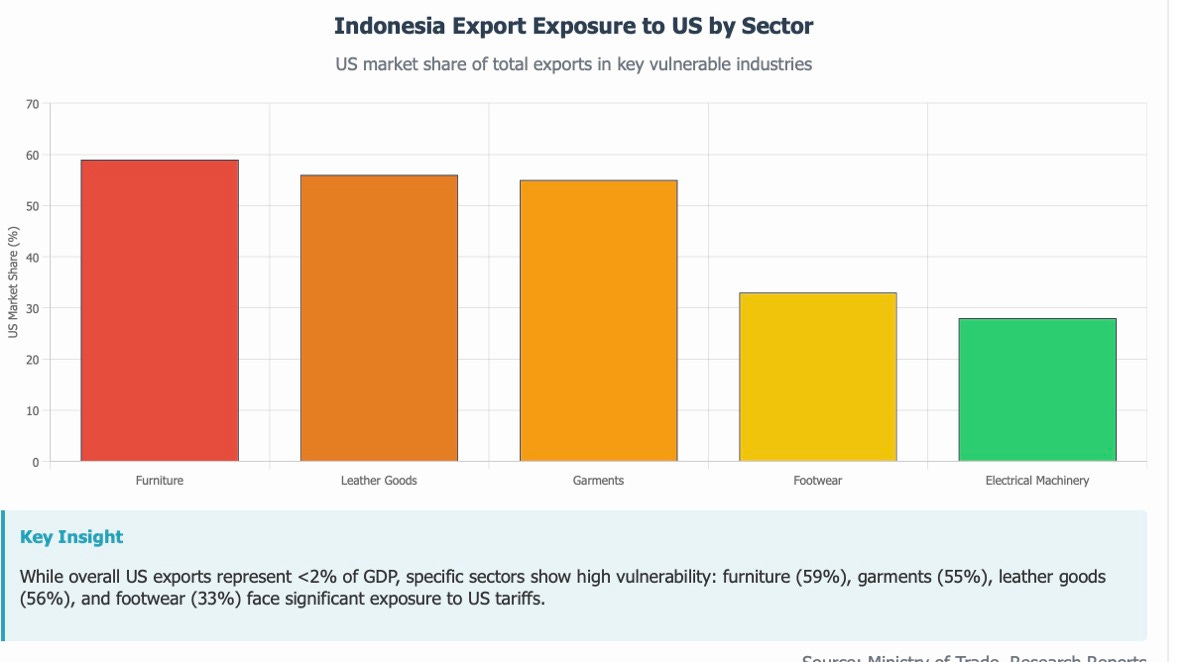

The most prominent of these external challenges has been the escalating trade tensions between the United States and China, which have created a climate of uncertainty that extends far beyond the two primary protagonists. The implementation of reciprocal tariffs, including the 34% tariff imposed on Indonesian goods by the United States, has directly impacted Indonesia’s export competitiveness in key markets. While Indonesia’s direct exposure to US markets is relatively limited—accounting for less than 2% of the country’s GDP—the indirect effects through supply chain disruptions and reduced global trade volumes have been more significant.

The trade war’s impact on Indonesia has been particularly pronounced in specific sectors where the country has substantial export exposure to the US market. Garments and clothing accessories, which account for 55% of Indonesia’s total exports in this category to the US, have faced significant headwinds. Similarly, furniture exports, where the US absorbs 59% of Indonesia’s total production in this segment, have been severely affected by the tariff regime. Footwear (33% US market share), leather goods (56%), and electrical machinery (28%) have all experienced similar pressures.

Beyond the direct tariff impacts, the trade war has created broader uncertainty that has affected investment decisions and business confidence. The prospect of further escalation and the unpredictability of trade policy have made businesses more cautious about long-term planning and capital allocation. This uncertainty has been particularly damaging for Indonesia’s manufacturing sector, which relies heavily on global supply chains and export markets.

The second-order effects of the trade war have been equally significant. China’s response to US tariffs has included efforts to redirect its exports to alternative markets, creating increased competition for Indonesian producers in third-country markets. This “trade diversion” effect has put downward pressure on prices and market share for Indonesian exporters, particularly in commodity and manufactured goods sectors.

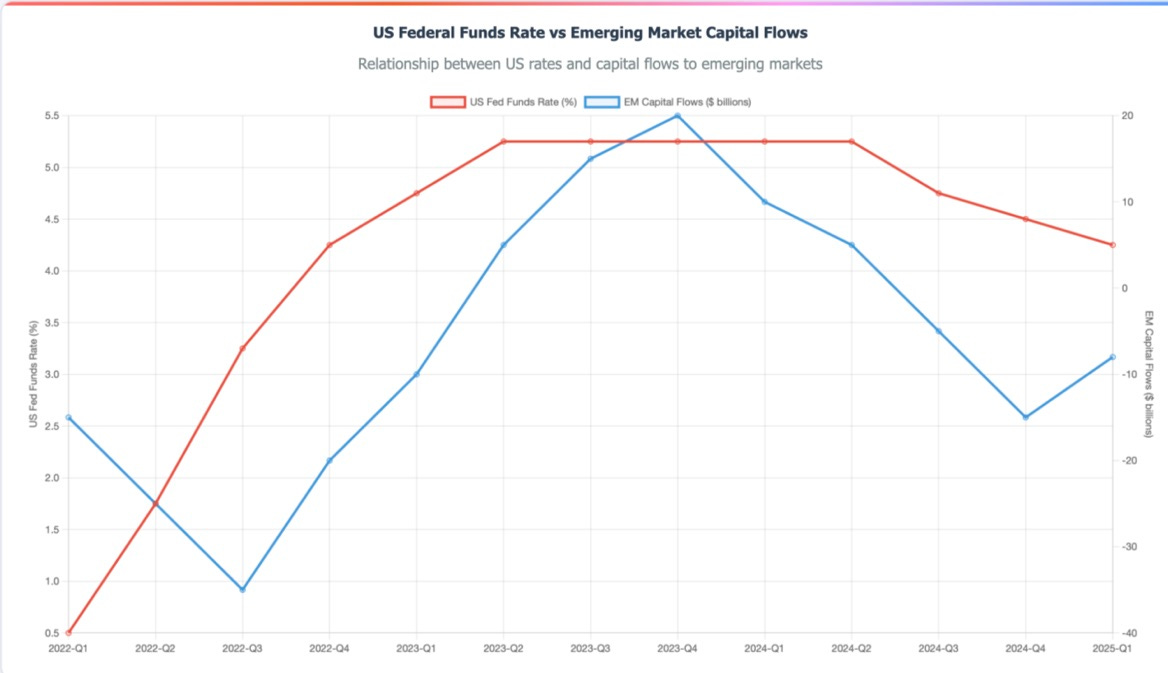

Global monetary policy shifts have created another significant external headwind for Indonesia. The US Federal Reserve’s maintenance of elevated interest rates, with the Federal Funds Rate currently at 4.25-4.50%, has created a challenging environment for emerging market economies like Indonesia. The relatively high US interest rates have attracted capital flows away from emerging markets, putting pressure on currencies and constraining domestic monetary policy flexibility.

This monetary policy divergence has forced Bank Indonesia to maintain higher interest rates than would otherwise be optimal for domestic economic conditions. The central bank’s need to defend the rupiah and maintain adequate interest rate differentials with the US has limited its ability to provide monetary stimulus during periods of economic weakness. The 25 basis point rate cut implemented in January 2025, followed by another cut in May, represents a cautious approach to easing that reflects these external constraints.

Commodity price volatility has been another significant external challenge for Indonesia’s economy. As a major exporter of coal, palm oil, nickel, and other primary commodities, Indonesia is highly sensitive to global commodity price cycles. The weakness in coal prices during the first quarter of 2025, compared to both the previous quarter and the same period in 2024, has directly impacted export revenues and government fiscal resources.

The coal sector’s challenges reflect broader global trends toward renewable energy and climate change mitigation efforts. While these transitions are necessary from an environmental perspective, they have created near-term adjustment costs for coal-dependent economies like Indonesia. The country’s heavy reliance on coal exports—both for fiscal revenues and employment—has made this transition particularly challenging to manage.

Palm oil markets have faced their own set of external pressures. Environmental concerns and sustainability requirements in key export markets, particularly the European Union, have created additional compliance costs and market access barriers. The implementation of the EU Deforestation Regulation and similar measures in other markets has forced Indonesian producers to invest in certification and traceability systems, increasing production costs and reducing competitiveness in the short term.

Geopolitical tensions beyond the US-China trade war have also contributed to global economic uncertainty. The ongoing conflicts in Ukraine and the Middle East have disrupted global supply chains, increased energy costs, and created additional volatility in commodity markets. While Indonesia is geographically removed from these conflicts, the global economic spillovers have affected trade flows, investment patterns, and risk sentiment in ways that have constrained economic growth.

The global shipping and logistics disruptions that have persisted since the pandemic have created additional costs and inefficiencies for Indonesian exporters and importers. Container shortages, port congestion, and elevated freight rates have increased the cost of international trade and reduced the competitiveness of Indonesian products in global markets. These logistical challenges have been particularly problematic for time-sensitive exports and have contributed to supply chain uncertainties that have affected business planning and investment decisions.

Climate change and extreme weather events have created another category of external challenges. Indonesia’s geographic position makes it particularly vulnerable to climate-related disruptions, including floods, droughts, and extreme weather events that can affect agricultural production, infrastructure, and economic activity. The increasing frequency and severity of these events have created additional costs and uncertainties that have constrained economic performance.

Global financial market volatility has also posed challenges for Indonesia’s economy. Periods of risk-off sentiment in international markets have led to capital outflows from emerging markets, putting pressure on the rupiah and constraining domestic financial conditions. The extreme currency volatility experienced in early 2025, with the rupiah reaching 17,465 against the US dollar, exemplified the economy’s vulnerability to sudden shifts in global risk sentiment.

The global technology sector’s challenges have had spillover effects on Indonesia’s emerging digital economy. Supply chain disruptions in semiconductor and technology hardware markets have affected the cost and availability of digital infrastructure, constraining the development of Indonesia’s digital transformation initiatives. These challenges have been particularly significant given the government’s emphasis on digitalization as a key driver of future economic growth.

International tourism, a significant source of foreign exchange earnings for Indonesia, has been severely affected by global travel restrictions, health concerns, and changed consumer behavior patterns. While domestic tourism has shown signs of recovery, international visitor arrivals remain well below pre-pandemic levels, constraining the sector’s contribution to economic growth and employment.

The cumulative impact of these external headwinds has been to create an environment where Indonesia’s natural economic dynamism has been constrained by forces largely beyond the control of domestic policymakers. The economy’s openness, while generally a source of strength, has made it vulnerable to these global shocks and policy shifts.

However, it is important to note that some of these external pressures are beginning to ease. The temporary 90-day US-China trade deal has reduced immediate tensions, though long-term uncertainties remain. Commodity prices have shown signs of stabilization in some sectors, and global supply chain disruptions are gradually normalizing. The potential for US monetary policy easing in the latter part of 2025 could also provide relief for emerging market economies like Indonesia.

Understanding these external constraints is crucial for assessing Indonesia’s economic prospects. While the country cannot control global economic conditions, it can adapt its policies and strategies to better navigate external challenges and position itself to benefit when global conditions improve. The following sections will examine how domestic factors have interacted with these external pressures and explore the emerging signs of economic recovery.

4. Domestic Structural Impediments

While external headwinds have undoubtedly contributed to Indonesia’s economic underperformance, a comprehensive analysis must also examine the domestic structural impediments that have constrained the country’s growth potential. These internal challenges, many of which predate the recent global disruptions, represent fundamental constraints on economic efficiency, productivity, and competitiveness that require sustained policy attention and structural reform efforts.

The most significant of these domestic impediments is the persistent infrastructure deficit that continues to constrain economic efficiency despite substantial government investment in recent years. While Indonesia has made remarkable progress in developing its infrastructure—including the completion of major projects such as new airports, ports, and transportation networks—significant gaps remain that limit the economy’s ability to fully capitalize on its geographic advantages and market size.

The logistics sector exemplifies these infrastructure challenges. Despite being an archipelago nation with over 17,000 islands, Indonesia’s inter-island connectivity remains suboptimal, creating high transportation costs and inefficiencies that affect business competitiveness. The cost of moving goods between major economic centers remains elevated compared to regional peers, reflecting both infrastructure constraints and regulatory inefficiencies in the transportation sector.

Digital infrastructure represents another critical area where gaps persist. While urban areas have seen significant improvements in telecommunications and internet connectivity, rural and remote areas continue to lag behind. This digital divide constrains the development of e-commerce, digital financial services, and other technology-enabled economic activities that could drive productivity growth and economic inclusion.

The energy sector faces its own set of structural challenges. Despite abundant natural resources, Indonesia continues to grapple with energy security issues, including periodic fuel shortages and electricity supply constraints in certain regions. The country’s heavy reliance on fossil fuels, while providing short-term economic benefits through export revenues, has created long-term sustainability challenges and limited the development of renewable energy alternatives.

Regulatory complexity and bureaucratic inefficiencies represent another significant domestic impediment. While the government has made efforts to streamline regulations and improve the ease of doing business, Indonesia continues to rank below regional peers in various business environment indicators. The complexity of regulatory compliance, particularly for foreign investors and businesses operating across multiple jurisdictions within Indonesia, creates additional costs and barriers to business expansion.

The implementation of new regulations, while often well-intentioned, has sometimes created unintended consequences that have constrained business activity. The lack of coordination between different levels of government—national, provincial, and local—has resulted in overlapping and sometimes conflicting regulatory requirements that increase compliance costs and create uncertainty for businesses.

Labor market rigidities have also constrained economic dynamism and productivity growth. Indonesia’s labor laws, while providing important worker protections, have created inflexibilities that make it difficult for businesses to adjust their workforce in response to changing market conditions. These rigidities have discouraged formal sector employment and contributed to the persistence of a large informal economy that operates outside the formal regulatory and tax framework.

The skills mismatch between the education system’s output and the economy’s needs represents another structural challenge. Despite improvements in educational access and attainment, the quality of education and its relevance to modern economic requirements remain areas of concern. The lack of technical and vocational skills, particularly in emerging technology sectors, has constrained productivity growth and limited Indonesia’s ability to move up the value chain in manufacturing and services.

[Suggested Visualization: Indonesia Education and Skills Gap Analysis showing mismatches between supply and demand]

Financial sector development, while progressing, has not kept pace with the economy’s financing needs. Despite the presence of a relatively stable banking system, access to credit remains constrained, particularly for small and medium enterprises that form the backbone of the Indonesian economy. The banking sector’s conservative lending practices, while prudent from a stability perspective, have limited the flow of credit to productive sectors and constrained business expansion and investment.

Financial inclusion remains a significant challenge, with large segments of the population, particularly in rural areas, lacking access to basic financial services. While digital financial services and fintech platforms are beginning to address this gap, the pace of financial inclusion has been slower than in some regional peers, limiting the economy’s ability to fully mobilize domestic savings for productive investment.

The tax system presents another area of structural weakness. Indonesia’s tax-to-GDP ratio remains below regional averages and international benchmarks for countries at similar development levels. The narrow tax base, combined with significant informal sector activity, limits the government’s fiscal resources and constrains its ability to invest in infrastructure, education, and other growth-enhancing public goods.

Tax administration and compliance remain challenging, with complex procedures and limited digitalization creating barriers to voluntary compliance. The recent efforts to modernize tax administration and expand the tax base are steps in the right direction, but significant work remains to create a more efficient and equitable tax system.

Corruption and governance challenges, while improving, continue to create costs and inefficiencies that constrain economic performance. The lack of transparency in some government processes and the persistence of rent-seeking behavior in certain sectors create additional costs for businesses and discourage investment. While Indonesia has made significant progress in improving governance and reducing corruption, these challenges remain impediments to optimal economic performance.

The judicial system’s effectiveness in enforcing contracts and protecting property rights represents another area where improvements are needed. Uncertainty about legal outcomes and the time required to resolve commercial disputes create additional risks for businesses and investors, constraining investment and business expansion.

Environmental degradation and sustainability challenges have created additional structural impediments. Deforestation, air and water pollution, and other environmental problems have created costs that are not fully reflected in market prices but nonetheless constrain long-term economic sustainability. The need to balance economic development with environmental protection has become increasingly urgent as international markets impose stricter sustainability requirements.

The healthcare system, while improving, continues to face capacity and quality constraints that affect labor productivity and economic performance. The COVID-19 pandemic highlighted many of these weaknesses, but the underlying challenges of healthcare access, quality, and affordability predate the pandemic and continue to affect economic outcomes.

Regional development imbalances represent another structural challenge. Economic activity remains heavily concentrated in Java and a few other major centers, while many regions, particularly in eastern Indonesia, lag significantly behind in terms of economic development and living standards. This geographic inequality constrains the economy’s ability to fully utilize its human and natural resources and creates social and political tensions that can affect economic stability.

The persistence of the informal economy, while providing employment and income for millions of Indonesians, also represents a structural impediment to productivity growth and tax revenue generation. The large size of the informal sector reflects both the lack of formal sector opportunities and the regulatory and tax burdens that discourage formalization.

These various structural impediments have combined to constrain Indonesia’s economic potential and contribute to the recent underperformance. Addressing these challenges requires sustained policy effort and political commitment to structural reform. However, the government’s recognition of these issues and the ongoing reform efforts provide hope that these constraints can be gradually addressed.

The following sections will examine how these domestic structural challenges have interacted with external pressures to create the current economic environment, and explore the emerging signs that some of these constraints may be beginning to ease.

5. Monetary Policy Constraints and Currency Pressures

The conduct of monetary policy in Indonesia has been significantly constrained by external pressures and currency volatility, creating a challenging environment for policymakers seeking to balance domestic growth objectives with external stability requirements. Bank Indonesia’s policy decisions throughout the recent period of economic underperformance have been shaped by the need to maintain currency stability and manage capital flow volatility, often at the expense of providing optimal domestic monetary conditions.

The fundamental challenge facing Indonesian monetary policy has been the tension between supporting domestic economic growth and maintaining external stability. With the US Federal Reserve maintaining elevated interest rates at 4.25-4.50%, Bank Indonesia has been forced to keep its policy rates higher than would be optimal for domestic conditions to prevent excessive capital outflows and currency depreciation.

This external constraint became particularly evident during the currency crisis of early 2025, when the rupiah reached an extreme level of 17,465 against the US dollar on April 7. This dramatic weakening, representing a depreciation of more than 8% from the start of the year, highlighted Indonesia’s vulnerability to sudden shifts in global risk sentiment and capital flows. The currency’s volatility during this period created additional challenges for businesses and consumers, increasing the cost of imported goods and creating inflationary pressures that further constrained monetary policy flexibility.

Bank Indonesia’s response to these currency pressures has been measured and pragmatic, reflecting the central bank’s experience in managing external shocks. The decision to cut the BI Rate by 25 basis points to 5.75% in January 2025 represented a cautious first step toward monetary easing, but the subsequent currency volatility forced the central bank to pause further easing until conditions stabilized.

The resumption of monetary easing in May 2025, with another 25 basis point cut bringing the BI Rate to 5.50%, signaled the central bank’s assessment that external conditions had sufficiently stabilized to allow for more accommodative domestic monetary policy. This decision was supported by the moderation in inflation pressures and the stabilization of the rupiah following the extreme volatility of early April.

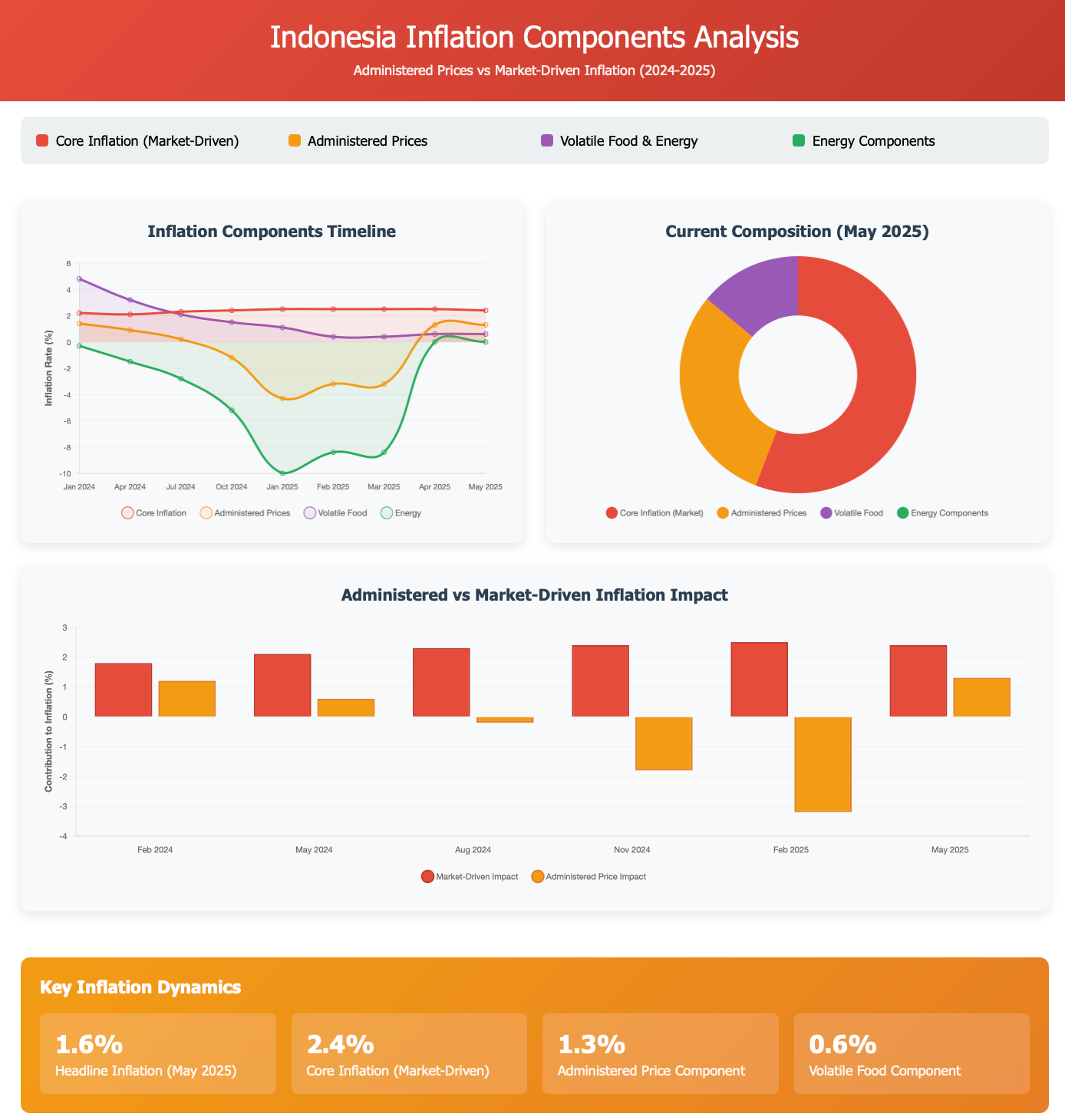

The inflation dynamics that have shaped monetary policy decisions present a complex picture of both challenges and opportunities. The return of headline inflation to the central bank’s target range of 1.5-3.5% in April 2025, reaching 2.0% year-over-year, marked an important milestone after a period of below-target inflation. However, this increase was primarily driven by the normalization of electricity tariffs rather than underlying demand pressures, highlighting the administered nature of many price movements in Indonesia.

The subsequent moderation of inflation to 1.6% in May 2025, down from the April peak of 1.95%, provided additional room for monetary policy easing. The decline was particularly notable in food prices, which rose by only 1.03% year-over-year in May compared to 2.17% in April, representing the smallest increase since August 2020. This food price moderation was attributed to the normalization of seasonal patterns following the earlier Eid festivities and improved supply conditions.

Core inflation, which excludes administered and volatile food prices, has shown a more stable pattern, edging down to 2.4% in May from a 22-month peak of 2.50% in April. This core inflation trajectory suggests that underlying demand pressures remain contained, providing additional justification for the central bank’s decision to resume monetary easing.

The monetary transmission mechanism in Indonesia has faced its own set of challenges that have limited the effectiveness of policy adjustments. The banking sector’s conservative lending practices, while prudent from a financial stability perspective, have constrained the pass-through of policy rate changes to lending rates and credit growth. This has meant that even when monetary policy has been eased, the benefits have not always been fully transmitted to the real economy

Credit growth has remained subdued despite the relatively accommodative monetary policy stance, reflecting both supply-side constraints from conservative bank lending practices and demand-side weakness from cautious business and consumer sentiment. The banking sector’s focus on maintaining asset quality and managing regulatory requirements has led to tighter lending standards that have limited credit availability, particularly for small and medium enterprises.

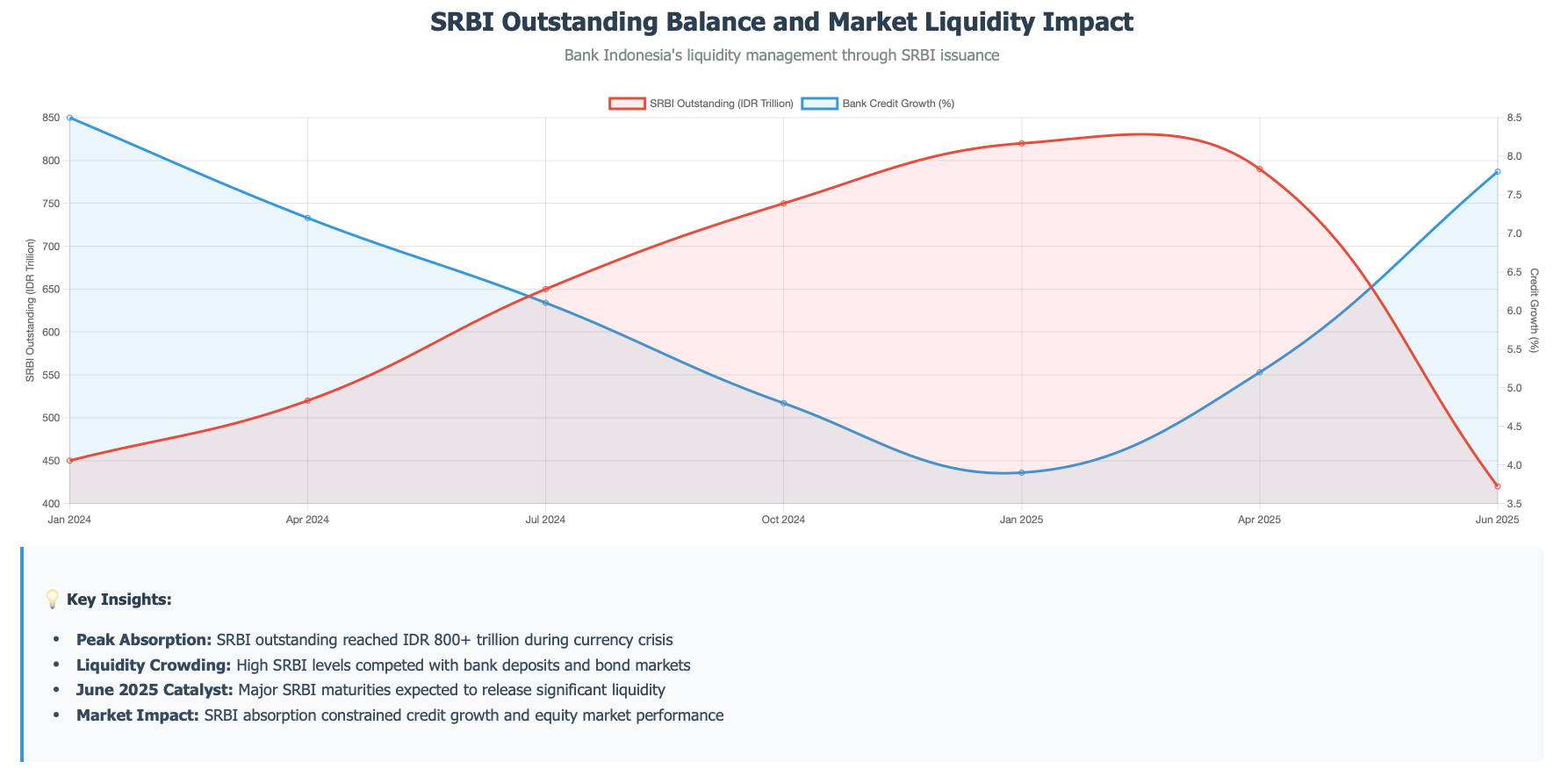

SRBI Impact on Liquidity and Banking Sector Dynamics

A critical factor affecting monetary policy transmission and banking sector liquidity has been Bank Indonesia’s extensive use of Sertifikat Bank Indonesia (SRBI) as a liquidity management tool. The SRBI program, which significantly expanded during the period of external pressures and currency volatility, has absorbed substantial liquidity from the financial system, creating important implications for bond markets, equity markets, and bank deposit dynamics.

The SRBI issuance reached elevated levels as Bank Indonesia sought to manage excess liquidity and support currency stability during periods of external stress. These instruments effectively competed with government bonds, corporate bonds, and bank deposits for investor funds, creating a crowding-out effect that constrained liquidity available for productive lending and investment activities.

The impact of SRBI on market dynamics has been particularly pronounced in the bond market, where the attractive yields offered on these central bank instruments drew funds away from government and corporate bond investments. This liquidity absorption contributed to higher borrowing costs for both the government and private sector, while simultaneously reducing the funds available to banks for lending activities.

The equity market has also been affected by the SRBI program, as institutional investors and fund managers allocated portions of their portfolios to these risk-free central bank instruments rather than equity investments. This dynamic contributed to the underperformance of Indonesian equity markets during periods of high SRBI issuance, as domestic liquidity was channeled away from risk assets.

Bank deposit dynamics have been similarly influenced, with the attractive yields on SRBI creating competition for bank deposits and affecting the cost of funding for financial institutions. Banks have had to offer competitive rates to retain deposits, putting pressure on net interest margins while simultaneously facing reduced lending opportunities due to the overall liquidity absorption.

The scheduled retirement of significant SRBI amounts in June 2025 represents a potentially important catalyst for liquidity release and banking sector recovery. As these instruments mature and are not fully rolled over, the previously absorbed liquidity is expected to flow back into the financial system, creating more favorable conditions for bank lending, bond market activity, and potentially equity market performance.

This liquidity release is expected to benefit the banking sector in multiple ways. First, it should reduce competition for deposits, allowing banks to lower funding costs and improve net interest margins. Second, the increased liquidity availability should support credit growth as banks have more funds available for lending activities. Third, the reduced competition from SRBI should make bank deposits and lending products more attractive relative to central bank instruments.

The timing of this liquidity release coincides favorably with other positive developments in the Indonesian economy, including monetary policy easing, currency stabilization, and improving economic sentiment. This convergence of factors creates the potential for a more pronounced recovery in banking sector performance and broader economic activity.

The foreign exchange intervention policies employed by Bank Indonesia have been crucial in managing currency volatility but have also created costs and constraints. The central bank’s efforts to smooth excessive currency volatility through market intervention have helped maintain confidence but have also required the use of foreign exchange reserves and created additional complexity in monetary policy implementation.

The coordination between monetary and fiscal policy has been another important factor shaping the overall macroeconomic policy stance. The government’s commitment to fiscal discipline and debt sustainability has limited the scope for aggressive fiscal stimulus, placing additional burden on monetary policy to support economic growth. This coordination challenge has been particularly evident during periods of economic weakness when both fiscal and monetary constraints have limited the policy response options.

The development of domestic financial markets has been crucial in supporting monetary policy effectiveness and reducing external vulnerabilities. The deepening of the government bond market and the expansion of local currency financing options have reduced the economy’s dependence on foreign currency funding and provided more tools for monetary policy implementation.

However, challenges remain in developing the full range of financial market instruments needed to support effective monetary policy transmission. The limited development of corporate bond markets and other capital market instruments has meant that the economy remains heavily dependent on bank financing, constraining the diversity of funding sources available to businesses and limiting monetary policy transmission channels.

The digital transformation of the financial sector has created new opportunities and challenges for monetary policy implementation. The rapid growth of digital payments and fintech services has changed the nature of money demand and payment patterns, requiring adjustments in monetary policy frameworks and implementation techniques.

Bank Indonesia’s forward guidance and communication strategy has evolved to address the challenges of managing expectations in a volatile external environment. The central bank’s efforts to provide clear communication about policy intentions and the factors driving policy decisions have been crucial in maintaining credibility and managing market expectations during periods of uncertainty.

The recent policy decisions, including the May 2025 rate cut, reflect the central bank’s assessment that external conditions have sufficiently stabilized to allow for a more growth-supportive monetary policy stance. Market expectations for additional rate cuts in 2025, with many analysts anticipating at least two more 25 basis point reductions to bring the BI Rate to 5.00%, suggest confidence in the central bank’s ability to continue the easing cycle.

The effectiveness of this monetary easing in supporting economic recovery will depend on several factors, including the continued stability of external conditions, the improvement in monetary policy transmission mechanisms, and the coordination with other policy measures to address structural constraints on growth.

Looking ahead, the monetary policy framework will need to continue evolving to address the challenges of managing an increasingly complex and interconnected economy. The balance between supporting domestic growth and maintaining external stability will remain a key challenge, particularly as global monetary policy cycles and capital flow patterns continue to evolve.

The experience of recent years has highlighted both the constraints and the importance of monetary policy in managing economic cycles in an emerging market context. While external factors have limited policy flexibility, the central bank’s careful management of these challenges has helped maintain macroeconomic stability and positioned the economy for recovery as external conditions improve.

6. Signs of Recovery: Emerging from the Trough

Despite the significant challenges that have constrained Indonesia’s economic performance in recent years, a careful analysis of current indicators reveals emerging signs that the economy may be beginning to turn the corner. These early signals of recovery, while still tentative, suggest that the combination of improving external conditions, policy adjustments, and the inherent resilience of Indonesia’s domestic economy may be starting to overcome the headwinds that have constrained growth.

The most encouraging sign of potential recovery lies in the stabilization and improvement of key macroeconomic indicators following the extreme volatility experienced in early 2025. The rupiah’s recovery from its April low of 17,465 against the US dollar to more stable levels around 16,330-16,370 in early June represents a significant improvement in external confidence and stability. This currency stabilization has been crucial in reducing uncertainty and creating more favorable conditions for business planning and investment decisions.

The resumption of monetary policy easing by Bank Indonesia, with the 25 basis point rate cut in May 2025 bringing the BI Rate to 5.50%, signals the central bank’s confidence that external conditions have sufficiently stabilized to allow for more growth-supportive policies. The market’s expectation of additional rate cuts in 2025, potentially bringing the policy rate to 5.00%, suggests that monetary conditions are likely to become increasingly supportive of economic recovery.

This monetary easing is occurring in the context of moderating inflation pressures, which provides additional room for policy support. The decline in headline inflation from 1.95% in April to 1.6% in May 2025, combined with the stabilization of core inflation at manageable levels, creates space for the central bank to prioritize growth support over inflation concerns.

The inflation moderation has been particularly notable in food prices, which have shown the smallest increase since August 2020. This food price stability is crucial for consumer confidence and spending power, as food represents a significant portion of household budgets, particularly for lower-income segments of the population. The normalization of food price pressures following the Eid festivities suggests that seasonal distortions are beginning to fade, creating more favorable conditions for consumer spending.

Consumer sector indicators are beginning to show signs of improvement that suggest the domestic demand engine may be starting to regain momentum. Consumer confidence has shown improvement in recent months, reflecting both the stabilization of macroeconomic conditions and the normalization of seasonal patterns following the earlier Eid celebrations.

The consumer goods sector, as exemplified by companies like Indofood CBP (ICBP), is reporting encouraging growth trends following the Eid period. Management expectations of stronger sales growth in the second quarter of 2025, supported by the earlier shift in Eid timing and the full impact of price increases implemented in February, suggest that consumer demand is beginning to normalize.

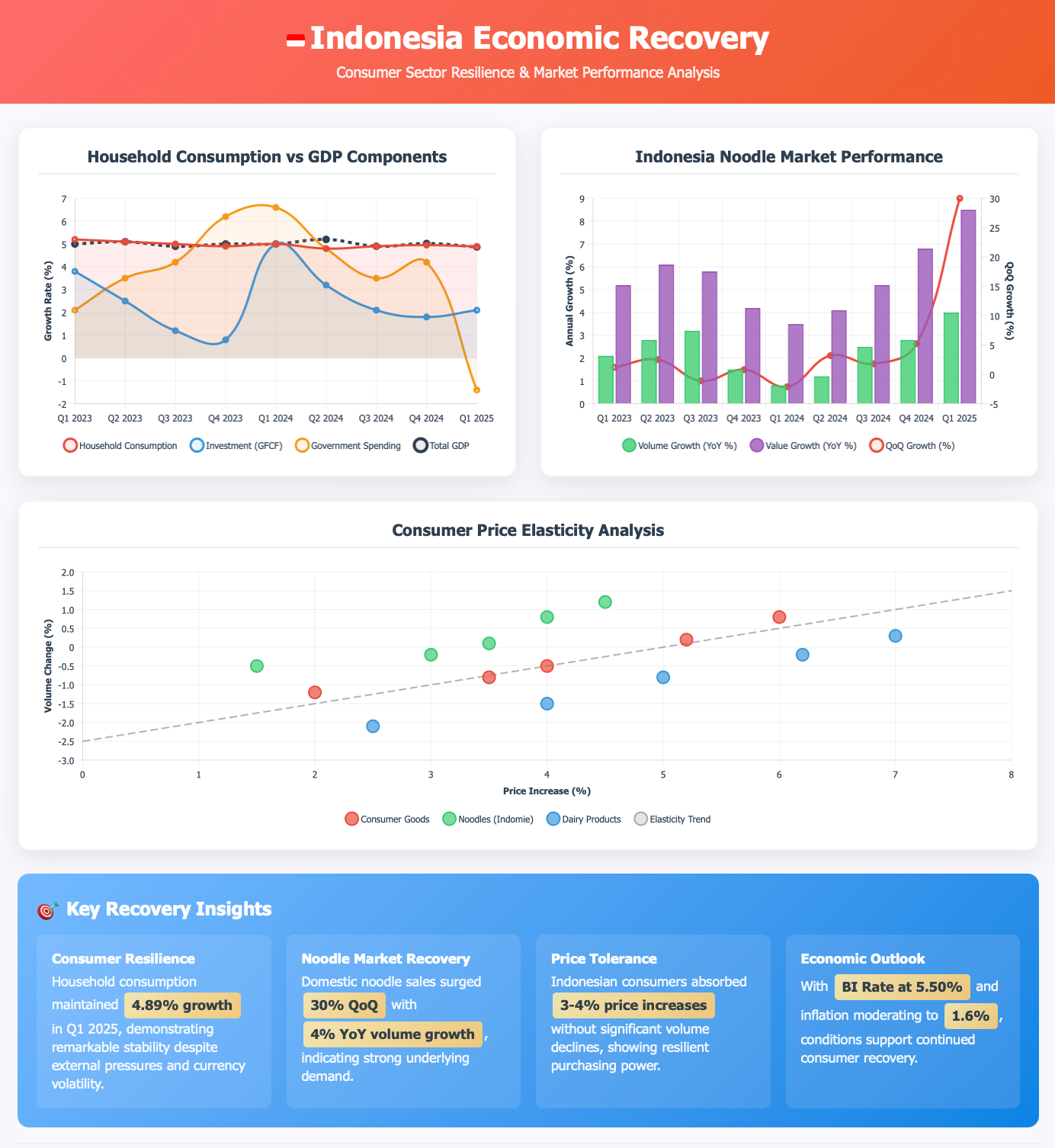

The noodle segment, a key indicator of mass market consumer demand, has shown particularly encouraging trends with domestic sales growing 30% quarter-over-quarter and aggregate volumes expanding 4% year-over-year. The absence of significant downtrading trends, with premium products like Indomie maintaining strong sales, suggests that consumer purchasing power remains resilient despite the economic challenges.

The retail sector is also showing signs of stabilization and potential recovery. Companies like Ace Hardware (ACES) are reporting solid performance despite margin pressures, with same-store sales growth of 2.2% in the first quarter of 2025. The company’s expansion strategy, particularly its focus on untapped markets in eastern Indonesia, reflects confidence in the underlying strength of domestic demand and the potential for market share gains.

The banking sector, a crucial barometer of economic health and confidence, is showing signs of stabilization following a period of cautious lending practices. Bank Mandiri’s assessment that the first quarter of 2025 likely represents the trough for net interest margins suggests that the sector may be positioned for improvement as interest rate conditions become more favorable and credit demand begins to recover.

The bank’s confidence in reaching its net interest margin guidance of 5.0% for 2025, up from the 4.8% trough recorded in the first quarter, reflects expectations of improving funding conditions and lending yield recovery. The stabilization of deposit pricing following the Lebaran period and the improvement in commercial lending yields suggest that the banking sector’s profitability pressures may be beginning to ease.

Investment sentiment is showing tentative signs of improvement, though this remains one of the more cautious areas of recovery. The stabilization of currency conditions and the improvement in policy predictability are creating more favorable conditions for investment planning, though businesses remain cautious about committing to large-scale projects given the recent volatility.

The government’s continued commitment to infrastructure development and structural reforms is providing some support for investment confidence. The completion of major infrastructure projects and the ongoing efforts to improve the business environment are creating positive signals for long-term investment attractiveness.

Foreign investment flows are beginning to show signs of stabilization following the extreme volatility of early 2025. The strong foreign fund inflows of approximately $195 million year-to-date into companies like Aneka Tambang (ANTM) suggest that international investors are beginning to recognize value opportunities in Indonesian assets following the recent market corrections.

[Suggested Visualization: Indonesia Foreign Investment Flows showing the stabilization following early 2025 volatility]

The commodity sector, while still facing challenges, is showing some signs of stabilization. Gold prices, which have remained strong at around $3,200 per ounce following the peak of $3,500 in April, continue to provide support for mining companies like ANTM. The company’s upgraded earnings forecasts and attractive dividend yield prospects reflect the sector’s potential to benefit from continued safe-haven demand and supply constraints.

Nickel markets are also showing signs of improvement, with expectations of tighter supply conditions supporting price recovery. The increase in third-party nickel ore sales and the positive outlook for demand from the electric vehicle and stainless steel sectors suggest that this important export commodity may be positioned for recovery.

The services sector is beginning to show signs of normalization following the pandemic-induced disruptions. Tourism, while still below pre-pandemic levels, is showing gradual improvement in both domestic and international segments. The normalization of travel patterns and the easing of health-related restrictions are creating more favorable conditions for the sector’s recovery.

Digital transformation initiatives are gaining momentum and creating new sources of economic dynamism. The rapid adoption of digital financial services, e-commerce platforms, and technology-enabled business models is creating new growth opportunities that are less dependent on traditional economic cycles and external conditions.

The government’s digitalization agenda and the private sector’s increasing investment in technology infrastructure are creating a foundation for more resilient and diversified economic growth. These digital economy developments represent a structural shift that could support long-term growth even as traditional sectors face cyclical challenges.

Regional economic integration initiatives, including Indonesia’s participation in the Regional Comprehensive Economic Partnership (RCEP) and other trade agreements, are beginning to create new opportunities for trade and investment. These agreements provide alternative market access options that can help offset some of the challenges created by US-China trade tensions.

The labor market, while still facing challenges, is showing some signs of stabilization. Employment levels have remained relatively stable, and there are early indications that job creation may be beginning to improve in certain sectors. The government’s focus on skills development and vocational training is beginning to address some of the structural mismatches that have constrained productivity growth.

Export performance, while still facing headwinds, is showing signs of diversification that could support long-term resilience. The development of new export markets and the gradual shift toward higher value-added products are creating a more balanced and sustainable export profile.

These various indicators, while still tentative, suggest that Indonesia’s economy may be beginning to emerge from the trough that has characterized recent performance. The combination of improving external conditions, supportive policy measures, and the inherent resilience of the domestic economy is creating conditions that could support a gradual but sustained recovery.

However, it is important to note that this recovery remains fragile and dependent on the continued improvement of external conditions and the successful implementation of structural reforms. The following sections will examine the specific sectors and policy areas that are driving this potential recovery and assess the sustainability of these positive trends.

7. Consumer Sector Resilience and Normalization

The Indonesian consumer sector has emerged as a critical pillar of economic resilience during the recent period of underperformance, demonstrating the fundamental strength of domestic demand that has long been recognized as Indonesia’s greatest economic asset. With household consumption accounting for more than half of GDP, the sector’s performance and trajectory are crucial indicators of both current economic health and future recovery prospects.

The resilience of Indonesian consumers has been particularly remarkable given the multiple challenges they have faced, including currency volatility, inflationary pressures, and employment uncertainties. Despite these headwinds, household consumption has maintained positive growth rates, providing a crucial buffer against external shocks and supporting overall economic stability during a period when other growth drivers have faltered.

The first quarter of 2025 data reveals the continued strength of this consumption base, with household spending growing 4.89% annually, representing only a slight deceleration from previous quarters. This performance is particularly impressive when viewed against the backdrop of currency volatility and external uncertainties that characterized the period, demonstrating the underlying resilience of Indonesian consumer demand.

The consumer goods sector has shown encouraging signs of normalization following the seasonal disruptions and timing shifts that affected the first quarter. The earlier Eid festivities in 2025 created temporary distortions in consumption patterns, but companies across the sector are reporting improved momentum as these seasonal effects normalize.

Indofood CBP’s experience exemplifies this normalization trend. The company’s management has expressed confidence in achieving its 7-9% sales growth guidance for 2025, supported by encouraging sales trends observed through the end of April. The expectation of stronger sales in the second quarter, following the earlier Eid shift, suggests that underlying consumer demand remains robust despite the temporary disruptions.

The noodle segment, often considered a bellwether for mass market consumer sentiment, has shown particularly strong performance. Domestic noodle sales grew 30% quarter-over-quarter in the first quarter of 2025, while aggregate volumes expanded 4% year-over-year. This volume growth is significant as it indicates real demand expansion rather than just price-driven revenue increases.

The absence of significant downtrading trends in the consumer sector provides additional evidence of consumer resilience. Management reports indicate that sales of premium products like Indomie have remained strong, suggesting that consumers have maintained their purchasing power and brand preferences despite economic pressures. This stability in consumption patterns indicates that the economic challenges have not fundamentally altered consumer behavior or forced widespread shifts to lower-quality alternatives.

The dairy segment, while facing more competitive pressures, continues to show innovation and adaptation. The launch of new products, such as less-sugar yogurt for children, demonstrates the sector’s ability to respond to changing consumer preferences and health consciousness trends. While it may be too early to assess the full impact of these innovations, they represent the kind of product development that can drive long-term growth and market expansion.

Price elasticity patterns in the consumer sector have provided important insights into the underlying strength of demand. The implementation of 3-4% price increases in mid-February 2025 by major consumer goods companies has been largely absorbed by the market without significant volume declines, suggesting that demand remains relatively inelastic and that consumers have maintained their purchasing power.

The retail sector has demonstrated similar resilience and adaptability. Ace Hardware’s performance in the first quarter of 2025, with revenue growth of 7% year-over-year and same-store sales growth of 2.2%, reflects the underlying strength of consumer demand for home improvement and lifestyle products. The company’s expansion strategy, particularly its focus on untapped markets in eastern Indonesia, demonstrates confidence in the long-term growth potential of Indonesian consumer markets.

The geographic expansion strategy being pursued by retailers like ACES highlights an important dimension of Indonesia’s consumer market potential. The company’s target of achieving a 45%/55% ex-Java/Java sales mix over the next five years reflects the significant untapped potential in Indonesia’s outer islands, where competition is less intense and operating costs are often lower.

This geographic diversification strategy is particularly important given Indonesia’s demographic and economic development patterns. The outer islands represent significant population centers with growing middle-class populations that are increasingly demanding modern retail formats and branded consumer goods. The expansion into these markets represents a structural growth opportunity that is less dependent on cyclical economic conditions.

Consumer confidence indicators have shown improvement in recent months, reflecting both the stabilization of macroeconomic conditions and the normalization of seasonal patterns. The improvement in confidence is particularly important as it tends to be a leading indicator of consumer spending patterns and can signal future consumption trends.

The digital transformation of consumer behavior has accelerated during the recent period, creating new channels and opportunities for consumer engagement. E-commerce adoption has continued to grow, supported by improved digital infrastructure and changing consumer preferences. This digital shift has created new opportunities for both traditional retailers and pure-play digital companies to reach consumers and expand their market presence.

The fintech and digital payments revolution has been particularly transformative for Indonesian consumers. The rapid adoption of digital payment platforms and mobile banking services has improved financial inclusion and created new opportunities for consumer credit and financial services. This digital financial infrastructure is supporting consumer spending by making transactions more convenient and accessible.

Consumer credit markets have shown signs of stabilization following a period of cautious lending practices by banks. While credit growth remains subdued compared to historical norms, there are early indications that lending conditions may be beginning to improve as banks gain confidence in the economic outlook and regulatory clarity improves.

The automotive sector, a significant component of consumer durables spending, has faced challenges but is showing signs of potential recovery. While vehicle sales have been constrained by economic uncertainty and financing conditions, the underlying demand for transportation solutions remains strong, particularly in urban areas where traffic congestion and infrastructure development are driving demand for personal mobility solutions.

The property sector, another important component of consumer spending, has shown resilience in certain segments. While luxury property markets have faced pressures, the affordable housing segment has continued to show demand, supported by government programs and the ongoing urbanization trend.

Food and beverage consumption patterns have shown interesting dynamics that reflect both economic pressures and changing consumer preferences. While there has been some shift toward value-oriented products, the overall consumption levels have remained stable, and premium segments have maintained their market positions in many categories.

The restaurant and food service sector has shown gradual recovery following the pandemic-induced disruptions. The normalization of social activities and the return of office-based work patterns have supported demand for food service, though the sector continues to adapt to changed consumer preferences and delivery-focused business models.

Consumer electronics and technology products have shown strong demand, reflecting both the digital transformation trend and the relatively young demographic profile of Indonesian consumers. The adoption of smartphones, laptops, and other technology products has continued to grow, supported by improving affordability and expanding digital infrastructure.

The healthcare and wellness sector has seen increased consumer focus and spending, reflecting both pandemic-related health consciousness and rising income levels. This trend toward health and wellness spending represents a structural shift that is likely to continue supporting consumption growth in these categories.

Tourism and leisure spending, while still below pre-pandemic levels, has shown gradual recovery as travel restrictions ease and consumer confidence improves. Domestic tourism has been particularly resilient, with Indonesian consumers increasingly exploring domestic destinations and supporting local tourism industries.

The consumer sector’s resilience during the recent period of economic challenges demonstrates the fundamental strength of Indonesia’s domestic market. The combination of a large population, rising income levels, and changing consumption patterns creates a foundation for sustained growth that is less dependent on external economic conditions.

Looking ahead, the consumer sector is well-positioned to drive economic recovery as external conditions improve and policy support measures take effect. The sector’s demonstrated resilience, combined with ongoing structural trends such as urbanization, digitalization, and demographic changes, suggests that consumer demand will continue to be a key pillar of Indonesian economic growth.

The normalization of seasonal patterns, the stabilization of macroeconomic conditions, and the continued adaptation to changing consumer preferences position the sector for potential acceleration in growth as the broader economic recovery takes hold.

8. Policy Response and Structural Reforms

The Indonesian government’s policy response to the economic challenges of recent years has been characterized by a careful balance between maintaining macroeconomic stability and implementing structural reforms designed to enhance long-term growth potential. This multi-faceted approach has involved coordination across monetary, fiscal, and structural policy domains, reflecting the complex nature of the challenges facing the economy.

The monetary policy response, as discussed in previous sections, has been constrained by external conditions but has shown increasing flexibility as circumstances have improved. Bank Indonesia’s decision to resume monetary easing in May 2025, following the earlier rate cut in January, demonstrates the central bank’s commitment to supporting economic recovery while maintaining price stability and external balance.

The central bank’s forward guidance has emphasized a data-dependent approach that prioritizes both domestic growth conditions and external stability considerations. The market’s expectation of additional rate cuts in 2025, potentially bringing the BI Rate to 5.00%, reflects confidence in the central bank’s ability to continue providing monetary support as conditions permit.

Fiscal policy has played a crucial supporting role, though the government’s commitment to fiscal discipline has limited the scope for aggressive stimulus measures. The maintenance of a prudent fiscal stance, with debt levels remaining well within sustainable ranges, has helped preserve Indonesia’s credibility with international investors and rating agencies.

The government’s infrastructure investment program has continued despite fiscal constraints, reflecting the recognition that infrastructure development is crucial for long-term competitiveness and growth potential. The completion of major projects, including new airports, ports, and transportation networks, has begun to address some of the logistical constraints that have historically limited economic efficiency.

The focus on digital infrastructure development has been particularly important, with government initiatives supporting the expansion of broadband connectivity and digital services across the archipelago. These investments are creating the foundation for digital transformation across multiple sectors of the economy and supporting the development of new growth industries.

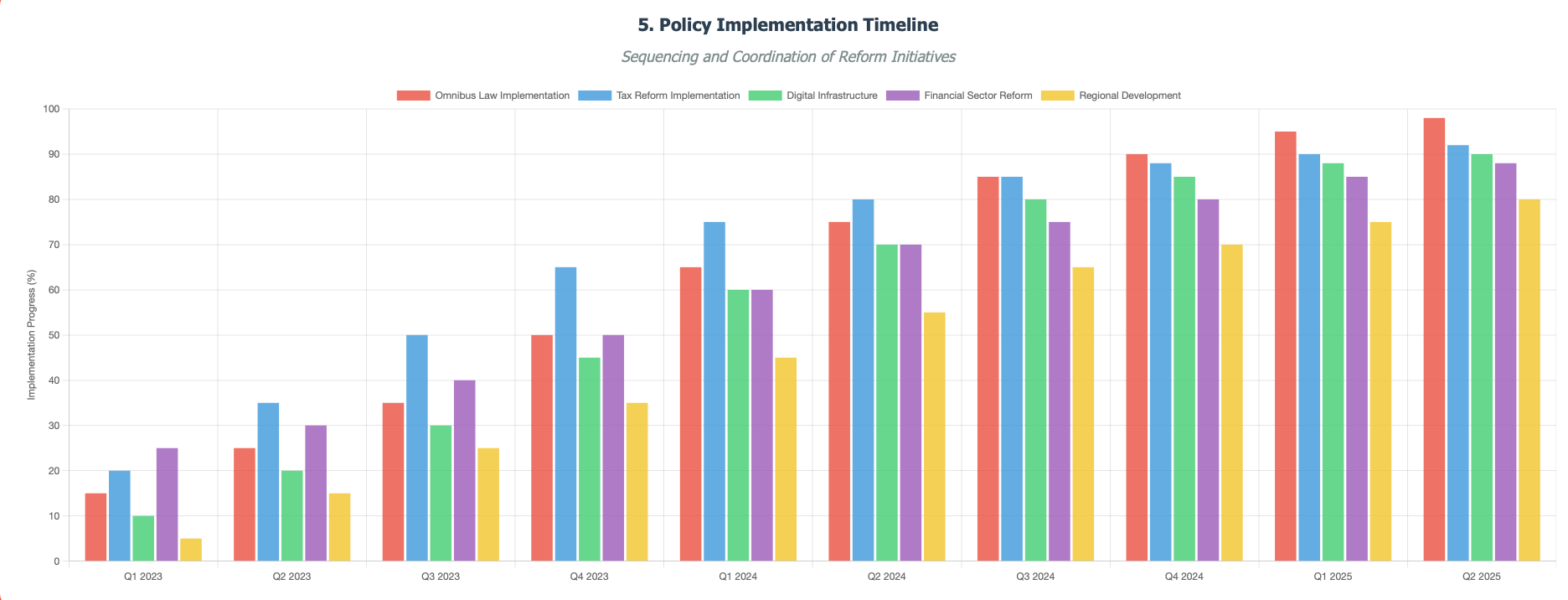

Structural reform efforts have accelerated in recent years, with the government implementing a series of measures designed to improve the business environment and enhance economic competitiveness. The omnibus law on job creation, while controversial, represents a significant effort to streamline regulations and reduce bureaucratic barriers to business expansion and investment.

The implementation of the omnibus law has involved extensive coordination between different levels of government and has required significant administrative capacity building. While the full impact of these reforms will take time to materialize, early indicators suggest that they are beginning to improve the ease of doing business and reduce regulatory compliance costs.

Tax reform initiatives have focused on expanding the tax base and improving tax administration efficiency. The digitalization of tax processes and the implementation of new compliance systems are designed to reduce the burden on taxpayers while improving revenue collection. These reforms are particularly important given Indonesia’s relatively low tax-to-GDP ratio compared to regional peers.

Indonesia Tax Reform Progress

Financial sector development has been another key area of policy focus. The government has implemented measures to improve financial inclusion, support the development of capital markets, and enhance the stability and efficiency of the banking system. The rapid growth of digital financial services has been supported by regulatory frameworks that balance innovation with consumer protection and systemic stability.

The development of Islamic finance has been a particular area of emphasis, reflecting both the religious composition of Indonesia’s population and the potential for Sharia-compliant financial products to serve underbanked segments of the market. The growth of Islamic banking and sukuk markets has created additional financing options for both businesses and consumers.

Trade policy has focused on diversifying export markets and reducing dependence on traditional commodity exports. The government’s participation in regional trade agreements, including the Regional Comprehensive Economic Partnership (RCEP), is designed to create new market access opportunities and support the development of more sophisticated export industries.