Lithium's Bumpy Ride

Navigating Oversupply, Innovations, and the Road to a Greener Future

Good day! I have made it safely to the beautiful Caribbean, but I am not letting the sea distract me too much (just a big Brine pool anyway). We’re kicking off the Lithium and Copper month with a review of the lithium market - where we are, how we got here and where we are going form here. I have also added a short “house view” essay at the end to bring it all together. Later in the week we’ll do a deep dive in to chinese companies in the Lithium space and which ones look good here.

**Important Reminder: Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.**

Lithium Market Analysis: Navigating Volatility and Preparing for Growth

The lithium market is experiencing a challenging period, marked by falling prices, oversupply, production adjustments, and strategic realignments. Despite near-term headwinds, long-term prospects remain robust, driven by the global transition to electric vehicles (EVs) and renewable energy solutions. This analysis integrates recent trends, cost dynamics, and supply-demand factors to provide a comprehensive outlook.

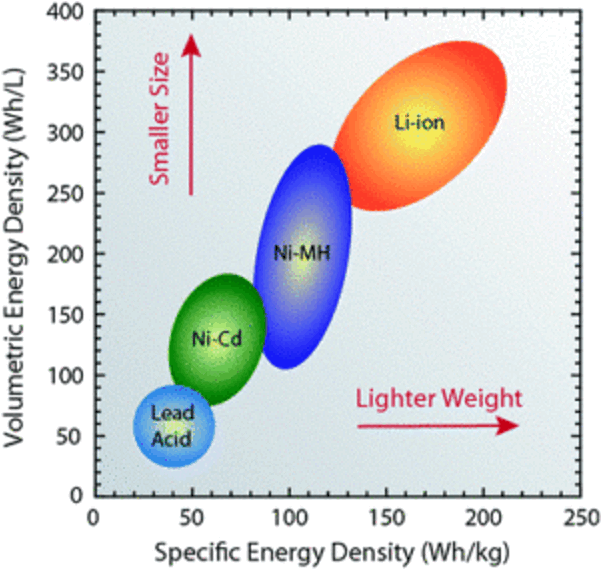

Lithium, a lightweight metal, is indispensable in the global shift toward sustainable energy, serving as a critical component in lithium-ion batteries that power electric vehicles (EVs) and store renewable energy. Its high energy density and electrochemical properties make it ideal for these applications, positioning lithium at the forefront of efforts to decarbonize transportation and energy sectors.

Recent technological advancements are reshaping lithium extraction and processing, aiming to enhance efficiency and reduce environmental impact. Direct Lithium Extraction (DLE) is a notable innovation, offering higher recovery rates and faster processing times compared to traditional methods. DLE is particularly beneficial in arid regions like Chile’s Atacama Desert, as it minimizes water usage. For instance, ElectraLith, a startup backed by Rio Tinto, is developing a DLE technology that extracts lithium from brine deposits without using water or chemicals, potentially producing lithium hydroxide at approximately half the cost of conventional methods.

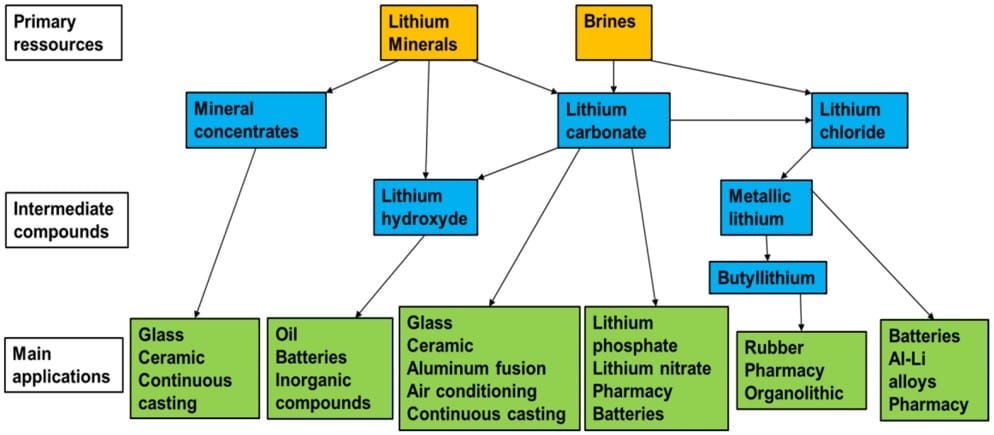

Lithium is sourced primarily from two types of deposits: hard-rock spodumene and brine resources, with the global supply chain heavily concentrated in a few regions. Australia leads lithium production, accounting for over 50% of global output, primarily through hard-rock mining, including the Greenbushes mine—the largest spodumene deposit globally.

Chile and Argentina, part of the “Lithium Triangle,” extract lithium from high-altitude brine resources, using evaporation ponds to concentrate lithium salts. Together, these countries dominate global lithium production. Additionally, China is an emerging player in lithium extraction, relying on lepidolite, a lithium-bearing mica, despite its higher costs. While China produces less lithium domestically, it plays a crucial role in refining and processing, handling over 60% of the world’s lithium for battery applications. Beyond primary sources, recycling is gaining traction as an alternative supply, with companies like Li-Cycle recovering lithium from used batteries.

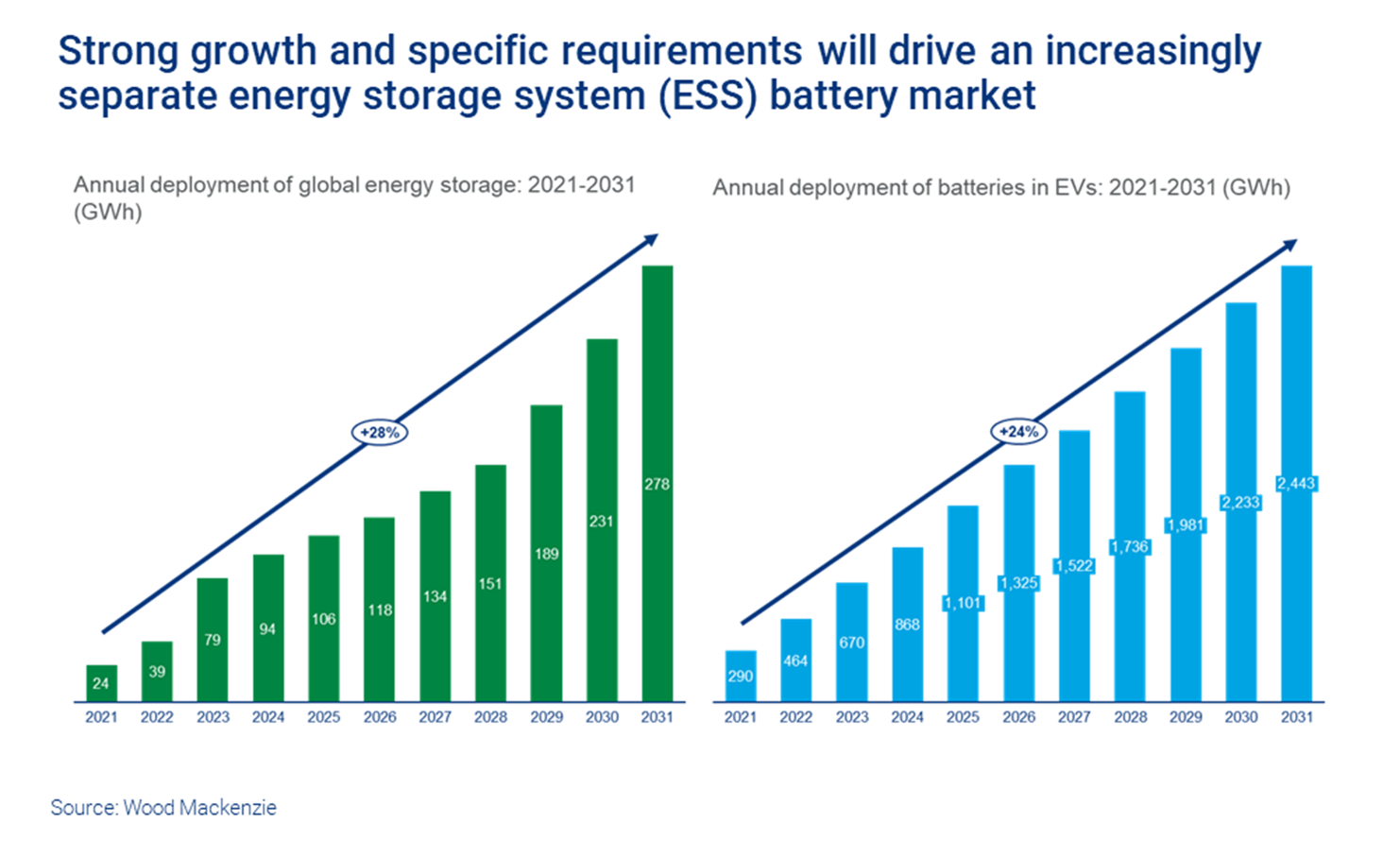

Lithium’s key applications include powering electric vehicles (EVs), forming the backbone of lithium-ion batteries, and energy storage systems (ESS), which stabilise renewable energy grids.

It is also used in smaller volumes for ceramics, glass, and lubricants. As EV adoption accelerates and renewable energy capacities expand, lithium’s demand continues to rise, cementing its role as the “white gold” of the energy revolution. However, the geographical concentration of lithium production and refining poses challenges, as geopolitical factors and trade policies could significantly impact the stability of the supply chain.

Efforts are underway to diversify and strengthen lithium supply chains. For example, Bolivia has signed an agreement with China’s CBC to invest $1 billion in building two direct lithium extraction plants, aiming to produce 35,000 metric tons of lithium annually. Additionally, countries like the United States and Canada are investing in domestic lithium projects to reduce reliance on foreign sources and enhance supply chain resilience.

Lithium’s pivotal role in the energy transition is underscored by ongoing technological innovations and strategic efforts to diversify its supply chain. As demand for EVs and renewable energy storage continues to rise, ensuring a stable and sustainable lithium supply will be crucial in achieving global decarbonization goals. However, the past few years have been anything but straightforward for the lithium market.

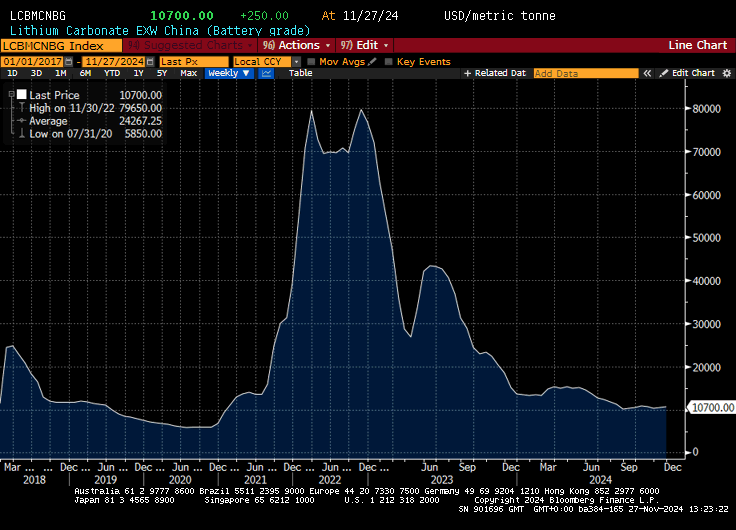

Lithium prices have experienced significant volatility since 2018, reflecting shifts in supply-demand dynamics, technological advancements, and market sentiment.

From 2018 to early 2021, lithium prices experienced a prolonged downturn. This was primarily due to an oversupply driven by aggressive production expansions, particularly in Australia and Latin America, as producers ramped up capacity to meet anticipated EV growth. However, demand failed to keep pace with the increased supply, leading to a glut in the market. Lithium carbonate prices fell below ¥50,000 per metric ton (~$7,000) during this period, placing significant financial pressure on higher-cost producers.

The market began to rebound in 2021, fueled by a surge in EV adoption and energy storage systems (ESS) demand, spurred by government incentives for decarbonization. Lithium carbonate prices surged, reaching ¥500,000 per metric ton (~$70,000) by late 2022, a nearly tenfold increase from their lows, driven by tight supply and robust demand from battery manufacturers. The rally was further supported by supply chain disruptions during the COVID-19 pandemic and delayed production from new projects.

In 2023, prices peaked at over ¥570,000 per metric ton (~$80,000), reflecting extraordinary demand from the EV sector and fears of supply shortages. However, by late 2023 and into 2024, the market shifted again as new production capacity from major projects in Australia, Chile, and Argentina came online. This, coupled with slowing demand growth in China—a market with already high EV penetration—and seasonal slowdowns in EV production, led to a sharp price correction.

By Q3 2024, lithium carbonate prices had dropped to ¥70,000 per metric ton (~$10,000), marking a dramatic 22% decline from earlier in the year. As of November 2024, prices in China had fallen 19.7% year-to-date to ¥77,500 per ton (~$11,000), reaching their lowest levels in 35 months. This decline reflects the current oversupply in the market, with inventory levels standing at 110,000 metric tons, about 60% higher than early 2024, further pressuring prices.

The historical price trends underscore the lithium market’s sensitivity to supply-demand imbalances and the critical role of technological, geopolitical, and economic factors in shaping its trajectory. Looking forward, analysts expect prices to stabilize around ¥70,000-¥80,000 per metric ton (~$10,000-$11,000) in the near term, with a potential recovery by 2028 as demand growth reasserts itself amid supply adjustments.