The Score at Half-Time

The first half went to the mainland, exactly as the plan intended. What worked and what didn’t in China and Hong Kong in 1H26, and why we still believe in HK

Good morning.

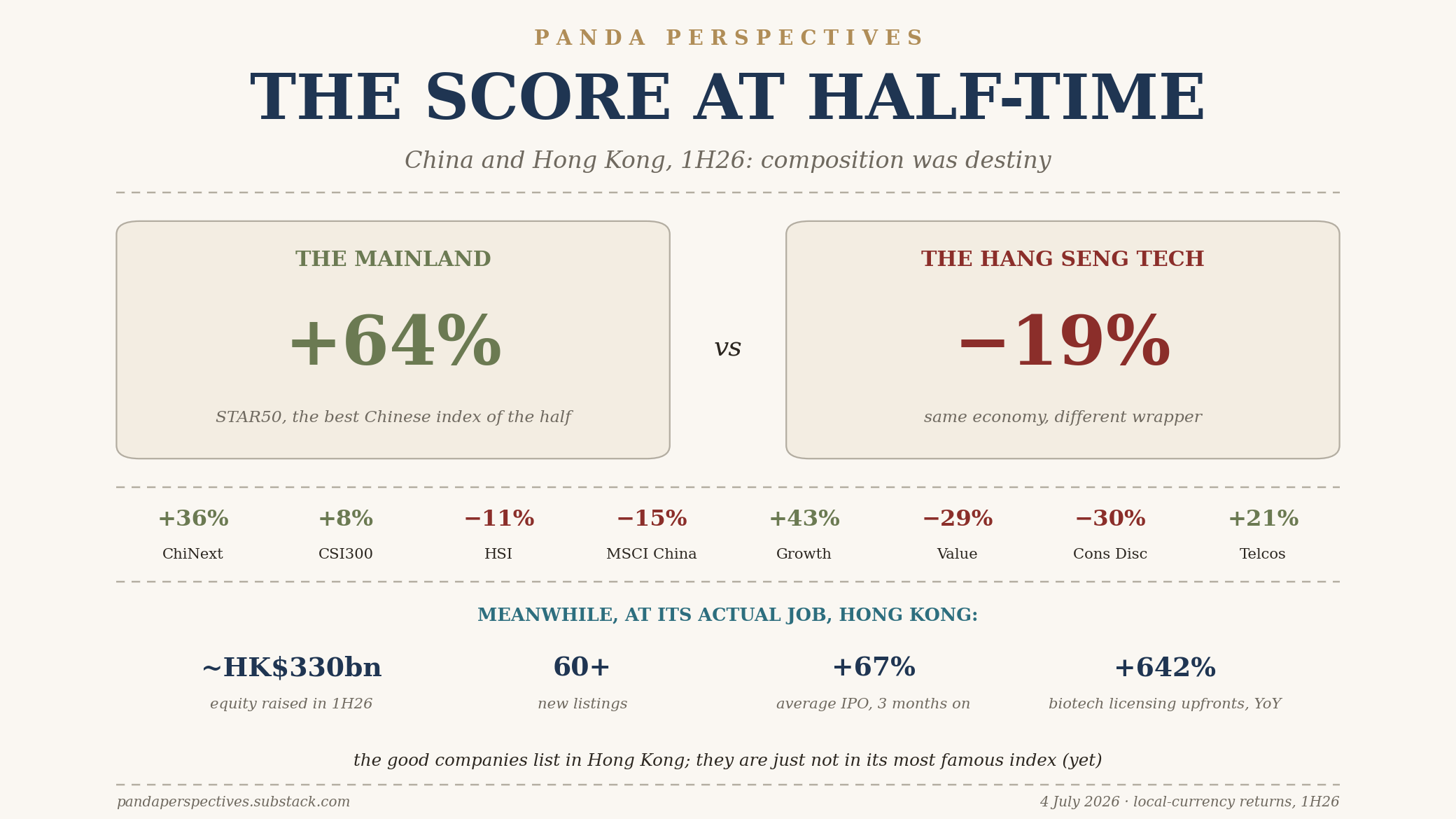

Every review of the first half of 2026 will open with Korea’s 151% moonshot or the AI names that carried the Nasdaq. Ours opens one market to the west, where the more instructive story played out: a single Chinese market that produced both a 64% winner and a 19% loser at the index level, depending entirely on which wrapper you bought. The half was a referendum on composition, and the second half will be a referendum on delivery.

Today, in brief: the 1H26 scoreboard and the one variable that explained most of it; why the mainland’s outperformance is the plan from Leonid Mironov’s June guest essay, Somewhere to Go, arriving on schedule; what the second half asks of the market; and why we believe Hong Kong still has a place in a landscape that has moved onshore. The verdict in three lines, as ever, and the case against at the end.

Th review section is free, the forward looking part is for subscribers. Please enjoy!

IMPORTANT NOTE: We are presently in the process of getting a license with a major regulator, and while that process is ongoing we are not able to publish the portfolio update and company notes. We’ll do a big reveal of the new plans as soon as we’re in a position to do thusly. We apologise for it taking time, but this is unfortunately a fact of life. With that we’re also putting the opinion part of this behind the wall.

NOTE: Panda+ is now closed to new joiners. We thank everyone for their interest and custom.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

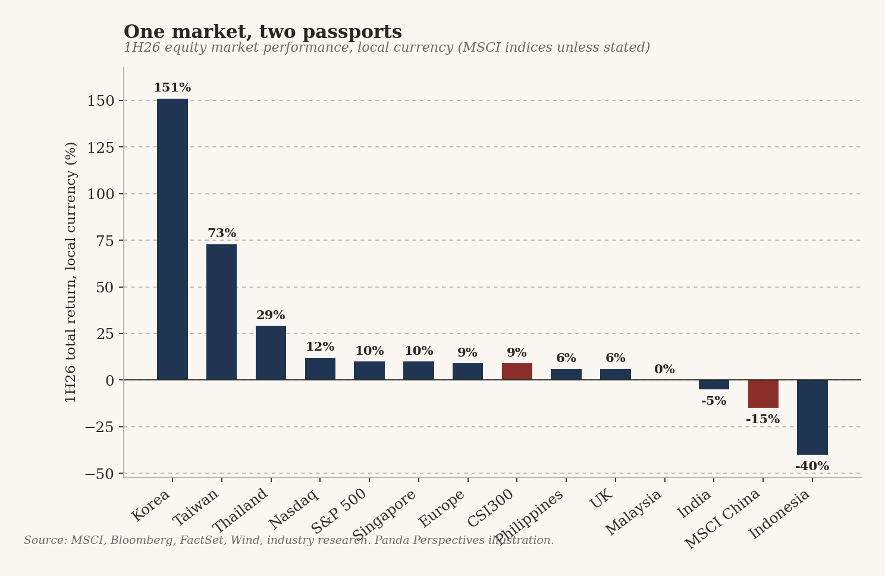

Start wide. In local-currency terms, 1H26 was a strong half for Asian equities and a brutal one for the China benchmarks most foreigners own. Korea returned 151%, Taiwan 73%, Thailand 29%. The Nasdaq and S&P 500 added 12% and 10%. MSCI China lost 15%, one of the worst results of any major market, with only Indonesia (down 40%) below it.

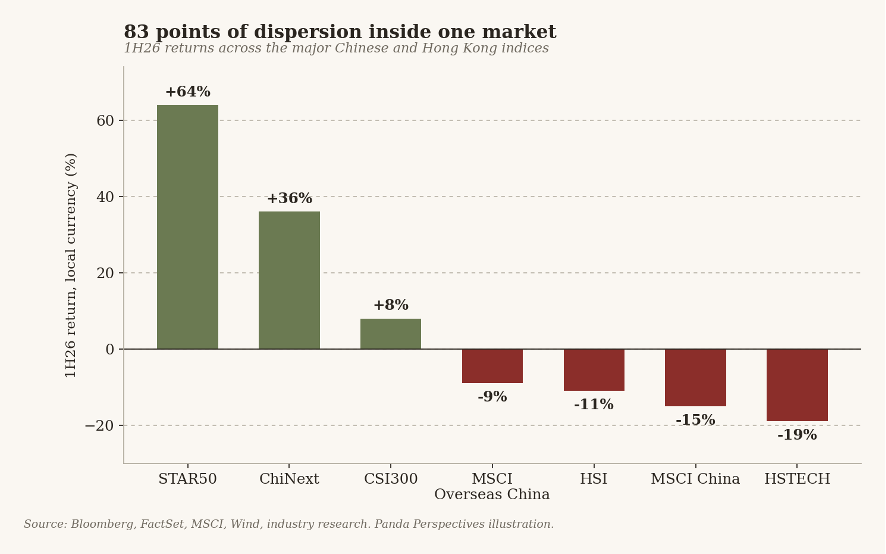

Now look inside China, because the aggregate hides everything. The STAR50 returned 64% in the half. The ChiNext returned 36%. The CSI300 managed 8%. Meanwhile the Hang Seng lost 11%, MSCI China lost 15%, and the Hang Seng Tech index, the instrument most institutional money uses to express a China tech view, lost 19%. That is 83 percentage points of dispersion between indices tracking the same economy, in the same six months.

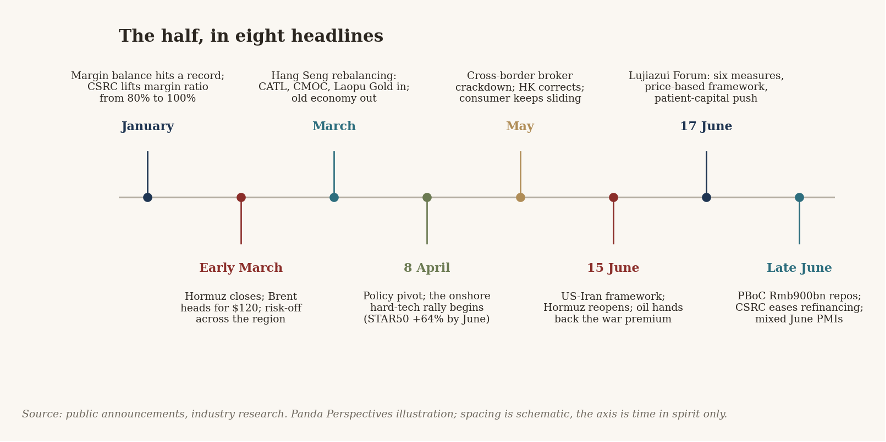

The half also had a plot twist worth recording, because it caught a lot of investors leaning the wrong way. In April we published Chinese Indices Decoded, and at that point the composition trade favoured Hong Kong: HSTECH was up roughly 12% year-to-date on its platform weight while the STAR50 sat flat, weighed down by semiconductor valuations. The 8 April policy pivot inverted the whole board. From that date the onshore hard-tech complex went vertical, and the offshore platform complex sold off as the AI capex bill landed on its income statements. The composition lens kept working perfectly. What changed was which composition the market wanted.

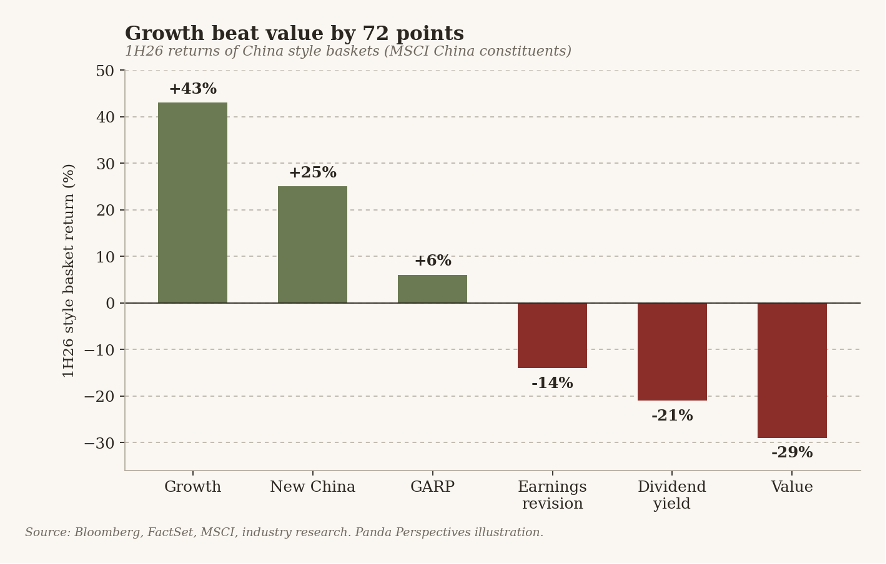

The style cut makes the regime explicit. Growth returned 43% in the half and value lost 29%, a 72-point spread. Dividend yield, the defensive trade that worked through 2024 and 2025, lost 21%. The market has stopped paying for stability and started paying for delivery.

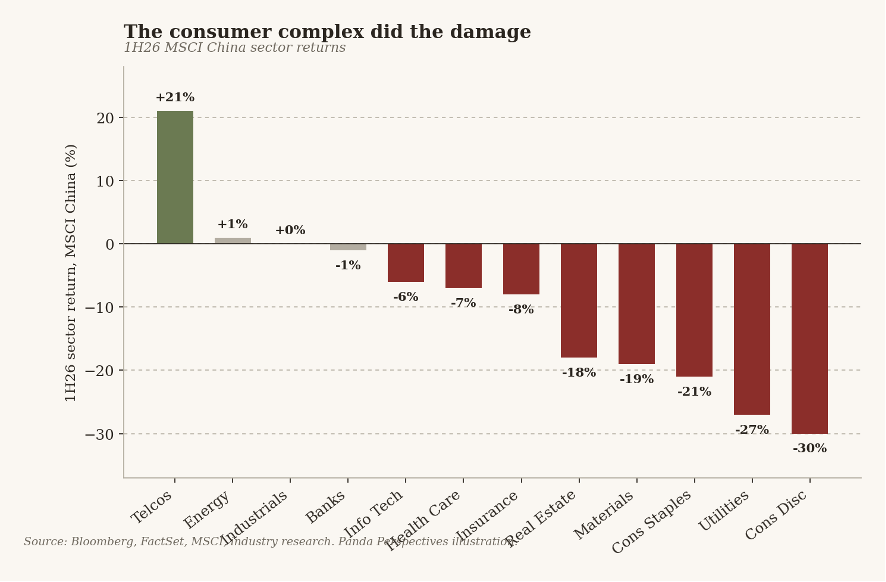

The sector cut tells you where the damage was. Telecoms returned 21% on the data-centre build-out. Energy, industrials and banks were roughly flat. And then the floor gives way: real estate down 18%, materials down 19%, consumer staples down 21%, utilities down 27%, and consumer discretionary down 30%, the worst sector in the index.

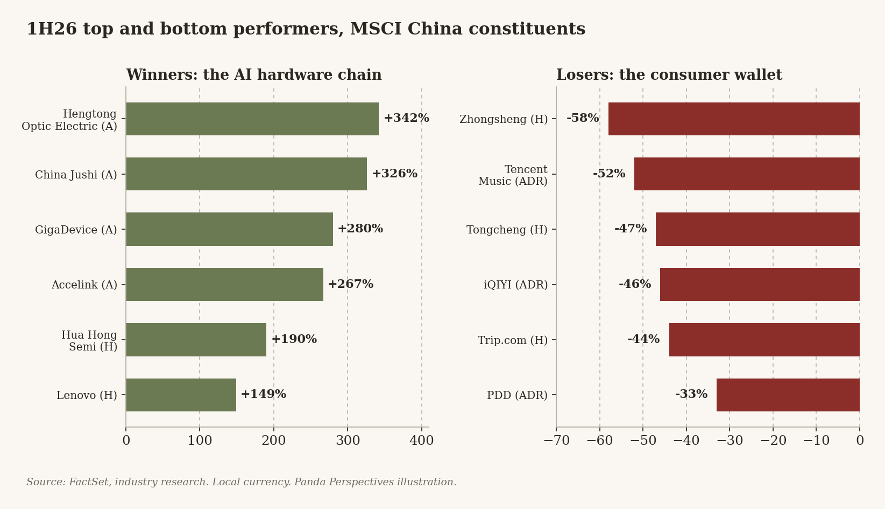

Single names complete the picture. The best performers in the A-share market were an optical cable maker (Hengtong, up 342%), a fibreglass producer whose electronic-grade cloth goes into AI server boards (China Jushi, up 326%), a memory designer (GigaDevice, up 280%) and an optical module house (Accelink, up 267%). In Hong Kong the leaders were Hua Hong Semiconductor (up 190%) and Lenovo (up 149%). The worst performers were a car dealership chain (Zhongsheng, down 58%), a music streamer (Tencent Music, down 52%), two travel platforms (Tongcheng down 47%, Trip.com down 44%), a video streamer (iQIYI, down 46%) and an e-commerce discounter (PDD, down 33%). One list sells picks and shovels to the compute build-out. The other list sells things to the Chinese household.

Three of those winners repay a closer look, because they show the machine working and our three questions earning their keep.

Lenovo tells you what kind of rally this was. What it does: assemble PCs, a business the market had long and fairly filed under commoditised also-rans, with a server sideline attached. The sideline is the story. The pivot into AI servers, made at the right moment, is what the half repriced: hyperscaler and enterprise capex filled the order book, domestic AI infrastructure procurement supplied a leg its Western rivals do not have, and the AI PC refresh added a kicker to the legacy business. How profitable: the re-rating tracked delivered revenue acceleration and mix-driven margin expansion, confirmed print by print through the spring. Keep the description honest, though: this is a thin-margin assembler that positioned itself well and collected 149% in six months for it. Which makes the valuation the uncomfortable question. The stock has compressed several quarters of conviction into weeks, and the runway question, how long the server cycle runs and at what margin for the integrator as opposed to the chipmaker, now matters far more than the next print. When the also-rans re-rate like champions, the cycle is being believed. It is also, increasingly, being priced. Hua Hong is the quieter version of the same story: a mature-node foundry, the unglamorous workhorse end of self-sufficiency, where management now describes utilisation running above 100% with pricing improving and the next tranche of capacity already funded, and where June’s semi-annual index review pushed roughly $3.1bn of passive money towards tech hardware with Hua Hong among the headline additions. And Hengtong, the half’s best A-share, is the purest case of all: it makes the optical cable and interconnect without which no data centre gets built, demand is being revised up faster than capacity can answer, and the market learned from the 800G optical-module cycle what that combination does to margins.

The losers were just as instructive, so take the anti-case too. Zhongsheng, down 58%, is China’s flagship car dealership group. What it does is sell and service premium foreign cars, a franchise the EV transition attacks from three directions at once: the brands it represents are losing share, the direct-sales model cuts the dealer out entirely, and the price war erodes the servicing annuity that made the model work. It looked cheap in January and got cheaper every month, and the index committee removed it from the Hang Seng in March. A car dealer at half price is still a car dealer. The same runway discipline separates the travel platforms (decent businesses priced for a consumer that stopped showing up, and plausible recovery stories) from the streamers (weak franchises meeting a weak consumer, with nothing on the other side of the valley). Runway decides which drawdowns are opportunities and which are verdicts.

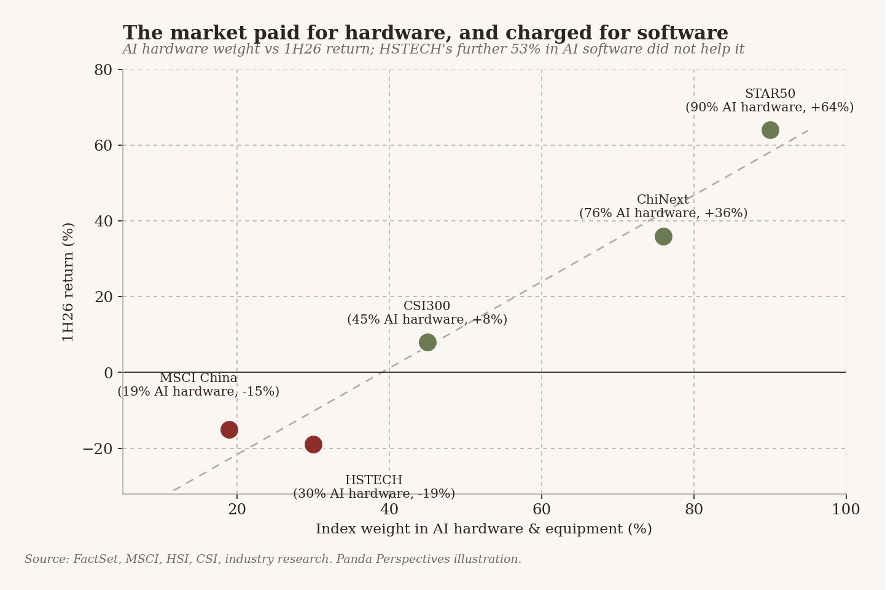

You can compress the whole half into a single scatter. Rank the indices by their weight in AI hardware and equipment, and the returns follow almost mechanically: the STAR50 at 90% hardware weight returned 64%; the ChiNext at 76% returned 36%; the CSI300 at 45% returned 8%; MSCI China at 19% lost 15%. The instructive outlier is HSTECH, which actually has 83% total AI exposure, and still lost 19%, because 53 of those points are AI software: the platforms that are paying for the build-out rather than being paid by it. The market spent the half paying for hardware and charging for software.

The mechanism deserves spelling out, because it is the layer beneath the scoreboard. The hardware names sit on the receiving end of the capex cycle: orders arrive first, earnings follow, and the 1Q26 season confirmed it, with aggregate A-share earnings up 9% YoY, tech hardware up roughly 50%, materials up 70% on the anti-involution repricing, and April industrial profits up 26%. May customs data ran the same direction, IC exports up 111% and IC imports up 68%. The platforms sit on the paying end of the identical cycle: Tencent and Alibaba are funding hundreds of billions of renminbi of AI capex out of consumer cash flows, and their managements said the quiet part aloud through conference season, that long-term AI investment takes priority over near-term profitability. Meituan spent the half burning margin in a local-services war, and the reported Rmb2tn state-backed data-centre programme was read, plausibly, as tomorrow’s competition for the private clouds. June then added a geopolitical tax, with Washington’s expanded military-linked entities list sweeping in Alibaba, Baidu, BYD and CATL among 65 additions, and a newly hawkish Fed repricing the discount rate on every offshore growth multiple. None of that touches an optical-cable plant in Suzhou. Nearly all of it lands on an ADR.

The exception inside software proves the rule. Zhipu, the model lab that listed in Hong Kong in January, rose more than 15-fold from its debut to rank as the best performer in the tech gauge, because a lab sells the models the capex produces, and the market believes its enterprise customers will stay. Its twin January debutant MiniMax roughly halved from March as the same market doubted exactly that about its consumer-facing revenue. Even within the software layer, the half paid proven demand and charged promises.

So, what worked: optics, semiconductors, AI hardware, telecoms, anything with a purchase order from a data centre. What didn’t: the consumer wallet in all its listed forms, property, utilities, and every index whose weights point at those things.

Part 2: The Why.

Somewhere to Go, the guest essay Leonid Mironov wrote for us in June, argued that China’s supply of capital, the demand to deploy it, and the returns to reward it were aligning for the first time in roughly 20 years. The first half delivered that alignment almost to the letter, and it delivered it where the essay’s logic says it must arrive first: onshore. The wall of capital is renminbi household savings. The patient buyers being conscripted are mainland insurers and pension funds. The assets both can most easily buy are A-shares, and the sectors policy is steering them towards are the hard-technology ones. When the reallocation started to move, the STAR50’s 64% and the growth basket’s 43% are simply what it looked like on a screen. The mainland’s outperformance was the plan, working. It is worth scoring the three legs separately.

The supply of capital held up, with a policy hand on the tap. The half opened with a record Rmb2.88tn of A-share margin balance and a regulator confident enough to lean against it, lifting the margin ratio from 80% to 100% in January. The Lujiazui Forum in June then formalised the architecture we described in the essay: a price-based monetary framework anchored on a repo corridor, direct financing running at 47% of incremental social financing, ahead of bank loans for the first time, and an explicit push to make insurers and pension funds the marginal buyer. Late June brought Rmb900bn of PBoC reverse repos across two operations and a CSRC draft easing refinancing rules for listed companies. The plumbing is being tightened where money is fast (margin) and loosened where money is patient (insurance, refinancing, IPOs). That asymmetry is the whole policy story of the half, and it is deliberate.

The demand for capital showed up in the earnings. High-tech manufacturing output grew 15.1% YoY in May, chip exports rose 111%, and overall exports grew 19.4%. The telecom, optics and semiconductor results that drove the scoreboard above are the Six Networks capex programme turning into revenue. This is the “somewhere to go” leg working as described.

The demand behind the demand split in two, and the market priced the split without mercy. New China demand is real: the compute orders, the grid orders, the storage orders. Old China demand is still shrinking. May retail sales fell 0.6% YoY, the first negative print of the cycle. Property investment is down 16.2% year-to-date, fixed asset investment down 4.1%. CPI at 1.2% tells you the household is still not bidding. Consumer discretionary down 30% in six months is that macro, marked to market. The June essay noted that the macro softness was concentrated in the Old China the thesis rotates away from. The half agreed, with a violence few anticipated.

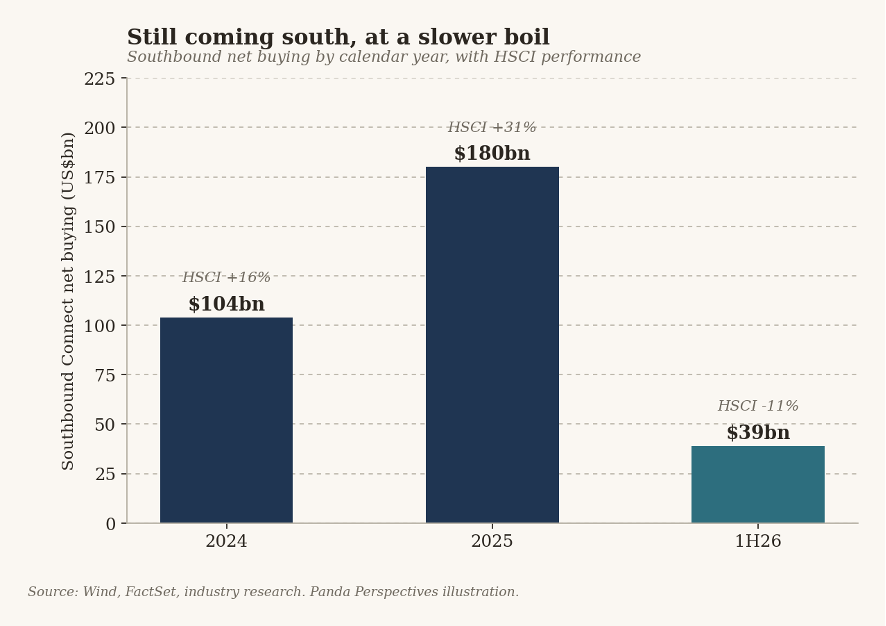

And the flows followed the logic, at a slower boil. Southbound bought US$39bn of Hong Kong stock in the half. That is well below 2025’s record US$180bn run rate, and May even saw the first monthly outflow since 2024 as mainland insurers rotated home. It is still US$39bn of net demand into a falling market, which is what a structural bid looks like: it slows when the tape fights it, and it does not reverse.

One puzzle inside the flow data is worth resolving, because it explains the style scoreboard. If policy wants insurers buying dividend stocks, why did the dividend basket lose 21%? Because the marginal insurer allocation went home. Mainland bond yields backed out of their long downtrend during the half, giving liability books a domestic alternative for the first time in two years, and the mandate steering a share of new premiums into A-shares pulls the same money onshore. The offshore dividend complex lost its incremental buyer at precisely the moment the growth complex found its earnings. Style rotations follow the marginal buyer, and in 1H26 the marginal buyer moved twice: out of offshore yield, into onshore growth.

One more first-half event deserves its own line, because it will echo through the second half. The Hormuz closure came and went. Oil spiked above $120, a four-month war compressed into the front of the curve, and the June peace handed most of the premium back, with Brent now near $83. China imports roughly 11 mb/d of crude; the round trip is worth on the order of $100bn to $150bn a year off the national import bill at current prices versus the April peak. That is a large, unlegislated tax cut for the same household whose weakness sits at the bottom of the sector chart, and it arrives just as the second half begins.

Part 3: The second half