The Strait Falls Quiet

A peace deal reopens Hormuz, oil hands back the war premium, and the bearish case we flagged in April arrives

Good morning,

Seven weeks ago we closed a long note on the Hormuz shock with a single forward call. If the Strait stayed shut long enough for the Gulf to build around it, the next move that mattered would be the reopening rather than another closure, and it would be bearish, because the workaround capacity built during the blockade does not get mothballed the day the tankers return. That reopening is now here. We thought it worthwhile to articulate our view going forward, especially in the context of the electrification work we’ve been doing lately.

As usual with our work on important current affairs we try and make it freely available, s please enjoy this post. But do please consider subscribing to support our work and get access to all our China content.

IMPORTANT NOTE: We are presently in the process of getting a license with a major regulator, and while that process is ongoing we are not able to publish the portfolio update and company notes. We’ll do a big reveal of the new plans as soon as we’re in a position to do thusly. We apologise for it taking time, but this is unfortunately a fact of life. With that we’re also putting the opinion part of this behind the wall.

NOTE: Panda+ is now closed to new joiners. We thank everyone for their interest and custom.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

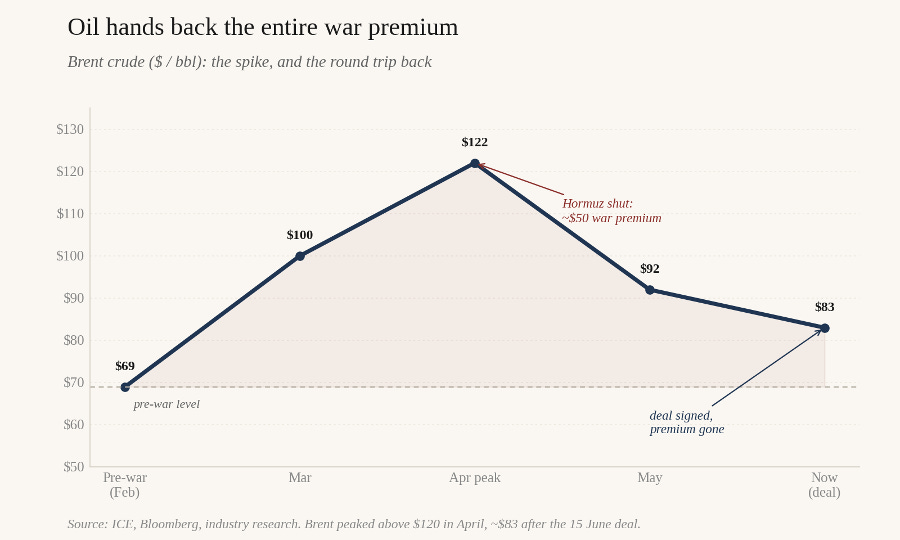

On 15 June the United States and Iran signed a framework deal at the G7, and the headline term is the one the oil market had been waiting four months for: Hormuz reopens. Commercial traffic restarts at once, Iran clears its mines within 30 days, and free passage is guaranteed for an initial 60 days. The price reaction was immediate and one-directional. Brent fell about 4% to roughly $83 a barrel and WTI to around $80, the lowest since early March, and that is on top of the 20% the market had already shed through May as a ceasefire moved from rumour to term sheet. Brent peaked above $120 in April, against roughly $69 before the conflict. At $83 it has handed back most of the war premium, with only a thin residual still in the price.

This is the resolution the April curve was built to price, and the speed of the move is the proof. We argued at the time that the bad news was already in the price: at $112 Brent, with the dated spread blown out and Hormuz shut, the asymmetry from there was that resolution compressed prices and only a fresh, un-priced disruption pushed them higher. Resolution won. The question worth thinking through now is not the first $40 of give-back, which has happened, but where the floor sits, because the supply side that reassembles on the far side of this deal is heavier than the one that existed before the war.

The overhang on the other side of the deal

Three things now lean on the price at once, and they compound.

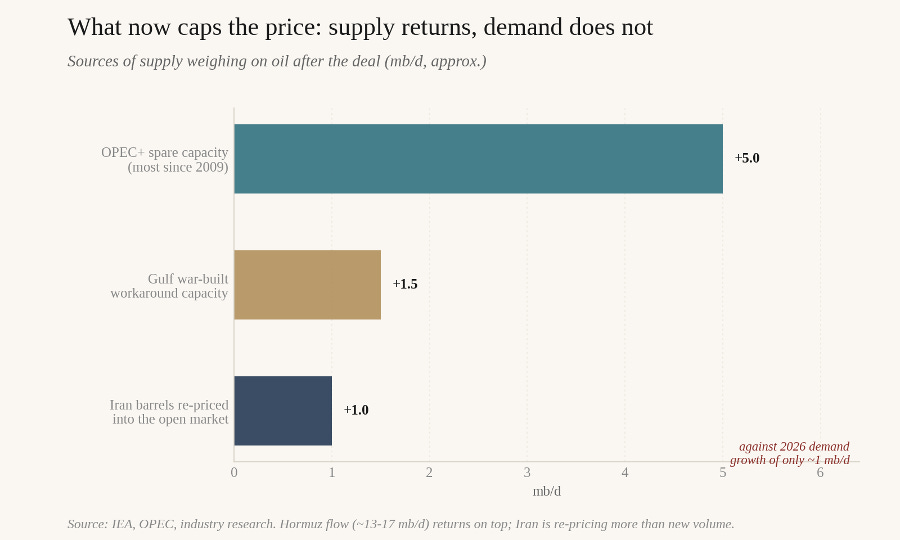

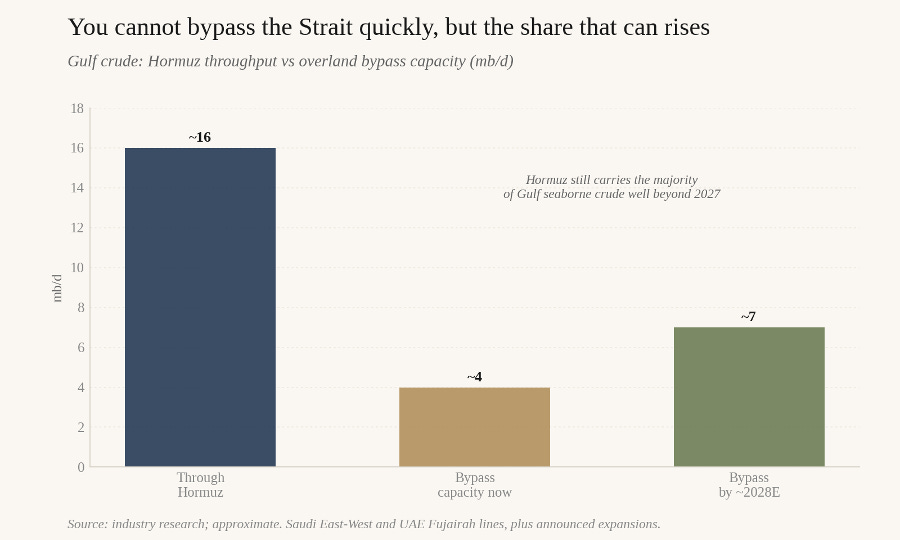

The first is the barrels that simply switch back on. Hormuz carries roughly a fifth of the world’s seaborne crude, on the order of 13 to 17 mb/d at normal throughput, and most of that returns over the demining and re-routing period.

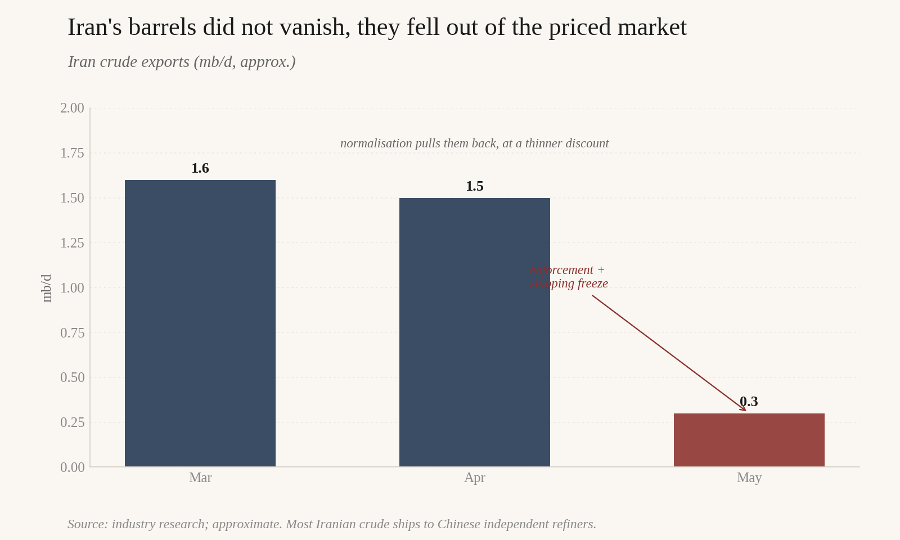

On top of it, more subtly, comes Iran’s own export channel, and it is worth being precise here, because it is easy to double-count. Those barrels never truly left world supply, since the buyer of almost all of them sits in China and kept taking what could still move, but they left the priced, dollar market when loadings collapsed to under 0.3 mb/d in May from 1.5 mb/d in April. A sanctions relaxation therefore does less by adding fresh volume, since much of that crude transits Hormuz and is already inside the throughput above, than by killing the distressed discount that made it move at all. That pulls the barrels back into the openly priced market and compresses the Iranian discount, which is bearish through price and re-routing rather than through a clean extra million barrels a day. The natural buyer for most of it still sits in China, which we come to below.

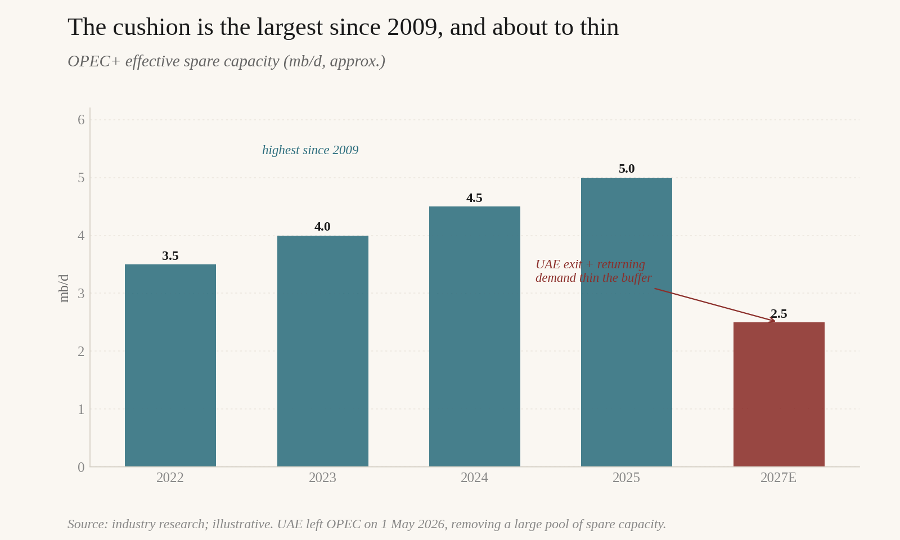

The second is the spare capacity that was always behind the curtain. OPEC+ idle capacity reached its highest level since 2009 during the war, on the order of 5 mb/d, and it is the reason Brent could not hold a rally above $85 even at the height of the closure. That cushion now has nowhere to hide. It also coordinates worse than it used to. The UAE left OPEC on 1 May, taking the second-largest pool of spare capacity out of the group, which leaves the cartel’s ability to manage the price on the way back down weaker than at any point in decades. A buffer that is large and uncoordinated is exactly the configuration in which prices overshoot to the downside.

The third is the engineering. During the closure the Gulf did begin to build around the Strait, and partial Yanbu uplift, Iraqi southern reactivation and the early Latin American and Canadian additions do not reverse because a treaty was signed. They stay on the water and add to the returning Hormuz flow rather than replacing it. Layer sluggish global demand growth on top, and the picture is a market that has gone from rationing barrels to absorbing them inside a single quarter.

None of this argues for a collapse into the $50s. There is a real floor not far below here. OPEC+ has every incentive to slow the descent, US shale stops adding barrels somewhere in the low-to-mid $60s a barrel for WTI, a breakeven that has fallen a long way from the shale-patch numbers of a decade ago, and the same strategic buyers who sat on their hands at $112 will restock into weakness. The honest read is a market that settles into a lower and calmer range, and we would treat the low $70s as a more likely test than a return to three figures. The $85 that capped every wartime rally is worth holding onto only with a caveat, because it was a level set by a closed Strait and an idle cushion, so it is a reasonable peacetime ceiling but not one the market has yet validated. The band is a judgment rather than a line the tape has drawn. The bulk of the war premium is gone, and what remains is an oversupplied market with a fragmented cartel, a slower and more durable kind of bearish.

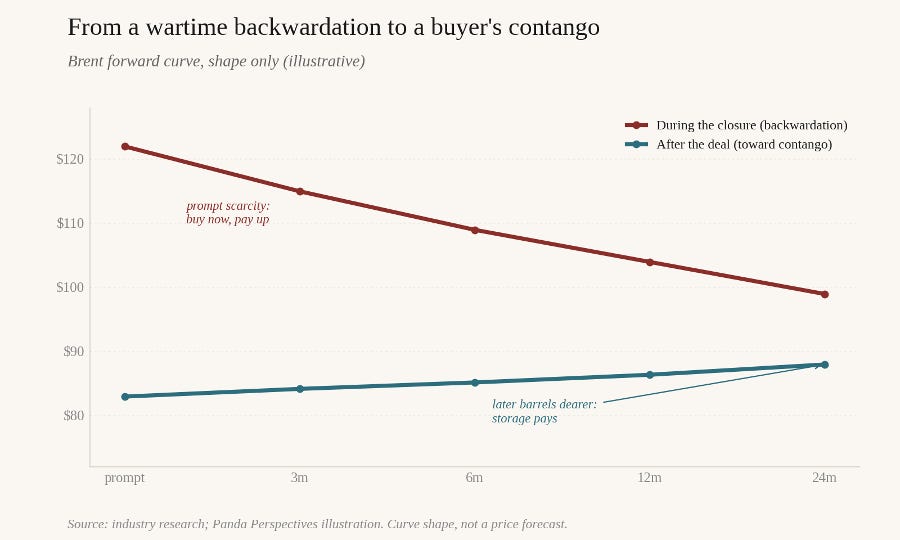

The cleanest confirmation of all this sits in the shape of the curve rather than the flat price. Through the closure the front of the curve was in steep backwardation, with prompt barrels commanding a fat premium over later-dated ones because the scarcity was immediate and the dated market was screaming. A reopening into a 5 mb/d cushion does the opposite. As prompt scarcity unwinds, that backwardation flattens and can tip into contango, where the later barrels trade above the prompt, and that flip matters for two reasons. It is the market’s own admission that the overhang is real, written in structure rather than in a forecast, and it pays a holder to store, which is exactly what turns China’s strategic restock from a patriotic gesture into an economic one. Watch the front spreads, because they tend to tell the story before the flat price has finished telling it.

Getting through the worst is not the same as a smooth path back, and the resumption itself will be uneven. Restarting a waterway that has been shut and mined for months is a lumpy, sequenced process, and the bullwhip can still pinch a specific product such as jet fuel or diesel, or a specific territory at the long end of the supply chain, for weeks while cargoes, refiners and freight re-sequence around the reopening. Those squeezes are real, and they will make headlines, but they are one-offs with a clear resolution path, and that distinction is the whole game. There are two kinds of disruption. In the first, the resolution is in sight and both the buyer and the seller still want to transact, so the market routes around the friction and clears, which is where we now are. In the second, the willingness to deal has itself broken, where a seller would rather hold the barrel back or a buyer would rather not be seen taking it, and that is the disruption with no self-correcting mechanism. This reopening is firmly the first kind. What is left to work through is timing and logistics, and timing and logistics always clear when both sides want the trade.

The cheque now runs the other way, and most of it clears in Asia

In April we wrote that the bill for the shock was being paid in places that do not make the financial news, by the import-dependent economies whose currencies and current accounts could not absorb $100 oil. Pakistan hiked its policy rate 100 basis points to 11.5% into the teeth of it, its first hike in 22 months. That cheque now runs the other way. Every dollar off the oil price is a transfer back to exactly those importers, and the relief lands hardest where the pain did, across South Asia and the import-dependent corners of the emerging world.

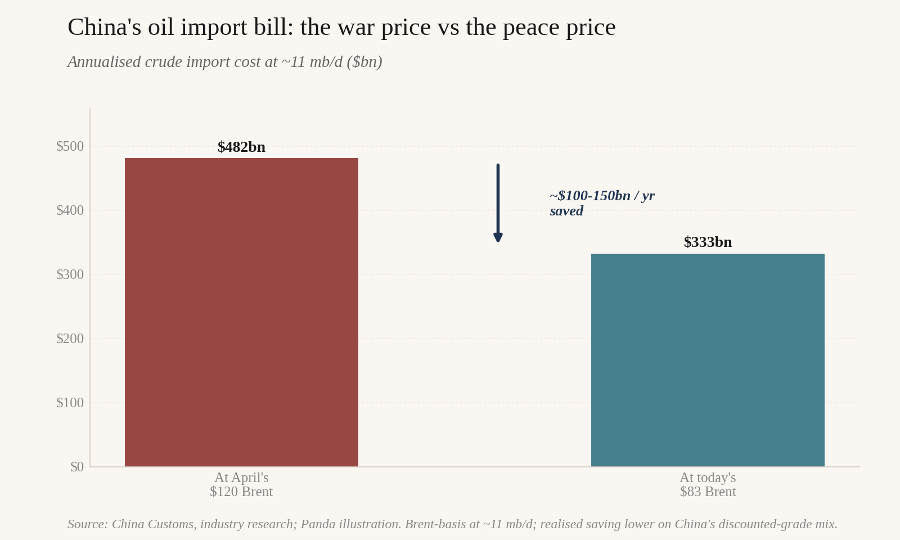

The largest single beneficiary, though, is China, and this is where the deal matters most for the readers of this note. China imports roughly 11 mb/d of crude, more than any country on earth, so the slide from April’s war peak is worth real money, on the order of $100bn to $150bn a year off the national import bill at a full-year run-rate. The precise figure is smaller than a naive peak-to-trough Brent sum implies, because a good slice of China’s barrels are discounted Iranian, Russian and other sanctioned grades that already traded below the headline, so the realised saving runs off a lower average price than $120. It is a large terms-of-trade gain regardless, flowing straight into lower input costs for refiners, airlines, shippers, chemicals and the household fuel bill. For a domestic-demand recovery that has been described all year as fragile, a large and unlegislated tax cut delivered by the oil market is a genuine tailwind.

It runs deeper than the flat-price saving. China’s small independent refiners, the teapots, take close to 90% of Iran’s exports and were importing a record 1.8 mb/d of Iranian crude in March, and they live on discounted, sanctioned feedstock. The peace deal cuts both ways for them. A normalised Iran sells fewer barrels at a distressed discount, which thins the specific edge the teapots enjoyed, while the lower outright price helps the refining complex as a whole. And China holds something like 120 to 130 days of strategic cover, which means it can do over the next few months what it does best in every oil down-cycle, which is buy the dip into the tanks and lock in cheap molecules while the war premium drains away.

There is a larger point inside that strategic cover than a cheap restocking opportunity, and it reframes China’s role in the whole episode. Through the worst of the closure, China did not chase scarce cargoes into a panicked market. It leaned on the 120 to 130 days of inventory it had spent a decade accumulating, and in doing so it quietly took the world’s largest marginal buyer out of a market that was already short. The motive was self-interested, but the effect was stabilising for everyone, because the single thing a stressed oil market needs least is the biggest importer on the planet bidding for the last available barrel. That restraint is the whole reason the inventories exist. A strategic reserve that is never drawn in a crisis is just expensive storage, and this was the crisis it was built for.

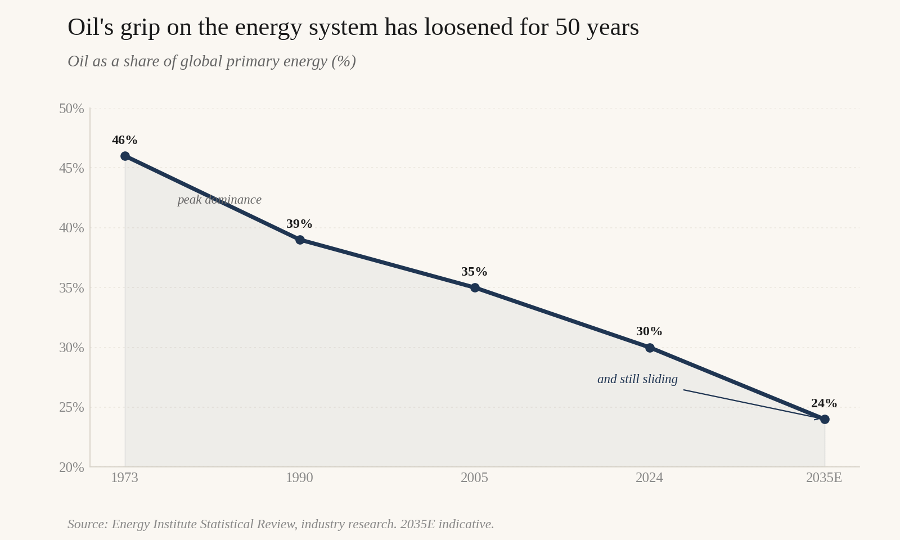

The most important point for this readership is the one the shock just proved. China sat through a four-month closure of the artery that carries a fifth of the world’s oil, and its energy supply held. Renewables now run above 60% of installed generating capacity, heavy-truck electrification has gone from 13% to 29% in a year, and grid storage is being deployed at a pace nobody else is near. The electrification build we have spent this whole series describing is what let China treat a historic oil shock as a manageable input-cost problem rather than a macro emergency. Cheaper oil is a bonus on top of that, and it does not slow the structural shift, because the Chinese transition is driven by the falling cost of making the hardware rather than by the price of the diesel it displaces. And even though the barrels got cheaper now, the reasons to keep electrifying did not change.

What would break this

The bearish case has one obvious failure mode, and it is the same fragility that has haunted this conflict from the start. The deal is a 60-day framework rather than a treaty. The ceasefire that preceded it broke more than once, strikes continued even as the terms were being agreed, and demining a contested waterway is a process that can stall or be reversed by a single incident. A re-closure would re-spike the price as fast as the reopening deflated it, and anyone treating the move down as a straight line is underwriting a peace that is days old. The structural overhang is real and durable. The path to it is not guaranteed to be smooth.

The second caveat is for the China bull. Cheaper energy at the margin makes the diesel truck and the gas boiler a little less painful to keep, and a naive reading would have it slow the electrification story. We think that reads the causation backwards, because the Chinese transition has been a manufacturing project rather than a price-of-oil project for several years now, but it is a tension worth watching rather than dismissing, and the place it would surface first is in the marginal heavy-truck and industrial-heat decisions over the next few quarters.

The last verse?

The deal does not stop the building. The Saudi, Emirati and Iraqi bypass projects that were accelerated during the closure keep going, because no Gulf producer wants to be held hostage to a single waterway twice. The existing overland routes, the Saudi East-West line to the Red Sea and the Emirati line to Fujairah, already move a few million barrels a day around the Strait, and the war has pushed both toward expansion. The pipeline math does not let anyone bypass a 13 to 17 mb/d artery in eighteen months, so Hormuz still carries the majority of Gulf seaborne crude well beyond 2027. What changes is the share that can go around it, which climbs year by year, and with it the premium the world is willing to pay for the chokehold comes down. The Strait stays important. It stops being the single point of failure it has been since 1980.

That invites a question larger than the trade, and it is the one we would leave readers with. Oil’s share of global primary energy has been sliding for two decades, and the electrification we have spent this series describing is accelerating the descent. A chokehold only has power over a commodity the world cannot do without, and both halves of that sentence are weakening at once. The Strait is being engineered around, and the thing it guards matters a little less every year. So it is worth asking whether a Gulf closure can ever again move the world the way this one did, or whether we have just watched something closer to the final verse of the oil age, the last time a single waterway could hold the global economy to ransom. We would not put a date on it. The direction is not in much doubt

.

The Strait has fallen quiet. We are still listening, because the last time it went quiet it did not stay that way for long, and the cheapest barrel of the year is usually the one the market is most certain about.

The verdict

Three lines, as ever.

The war premium is largely gone, and the overhang is heavier than the pre-war baseline. Returning Hormuz throughput, the re-pricing of Iranian barrels back into the open market, record OPEC+ spare capacity and a cartel fragmented by the UAE exit together describe an oversupplied market settling into a lower range, with $85 a plausible ceiling and the low $70s a more likely test than a return to three figures.

China is the largest single winner, on two clocks. The cyclical clock is the terms-of-trade gain, a saving on the order of $100bn to $150bn a year. The structural clock is the one the shock already proved, that the electrification build let China ride out the closure, and cheaper oil neither caused that nor undoes it.

The risk is that the peace is young. A 60-day framework over a contested Strait is not a settled one, and a single incident re-prices the whole move. The base case is a calmer, cheaper, oversupplied oil market. The hedge against it is that this conflict has surprised on the violent side more than once.

A follow-up to The Strait Has Spoken, Again (30 April 2026), and a companion to our China electrification series. pandaperspectives.substack.com

Data sources: IEA, EIA, OPEC, NEA, China Customs, Bloomberg, LSEG, industry research and company disclosures. Prices and figures current to 19 June 2026.

Nothing in this Substack is investment advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any companies or countries named are discussed as subjects of analysis, not as recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions.