The Strait Has Spoken

Picking Winners in APAC Energy After the Hormuz Shock

Good Morning,

Oil! Fertilisers! Gas! It’s all happening, and it’s all very exciting. We’ve been covering the Chinese views and reactions to the US-Israel and Iran standoff and the resulting bombardment, but we’ve been somewhat reluctant to address the energy impact directly - maybe it’s just a scare, maybe trade routes get rerouted for the next decade, maybe the worst is already priced. Now that the most benign options are off the table, but so seemingly (at least for now) are the worst ones, it feels like the right moment to try to put a finger on what’s what in the resulting energy balance.

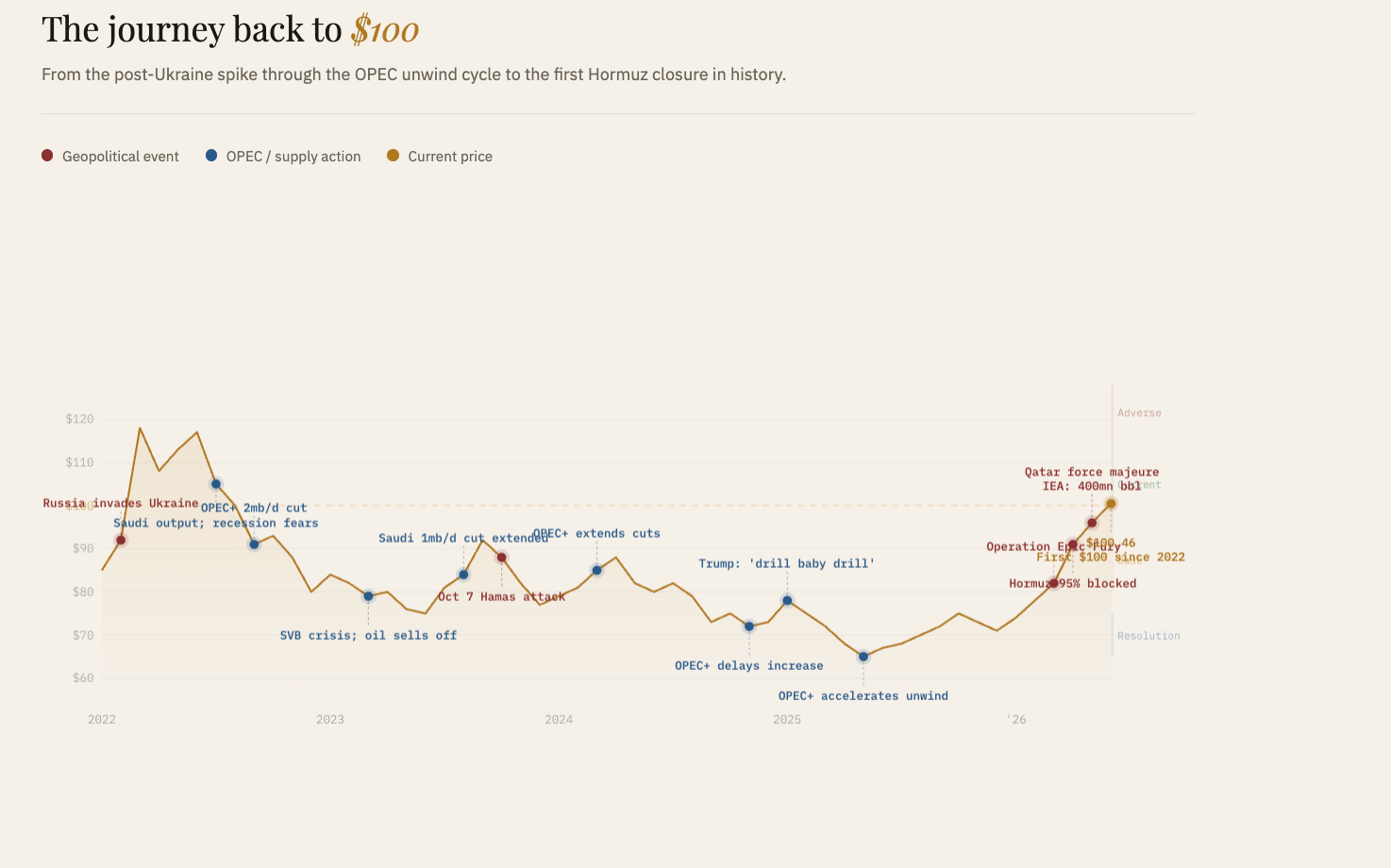

The Strait of Hormuz is closed. Operation Epic Fury - the joint US-Israel strike campaign that killed Supreme Leader Khamenei and shredded Iran’s nuclear and military infrastructure - did something the energy market had modelled as a theoretical tail risk for forty years. Not partially. Not temporarily as a negotiating posture. The IRGC mined the strait, attacked transiting vessels, and Iran’s newly appointed Supreme Leader Mojtaba Khamenei has since declared in his first public statement that the closure must continue as a “tool to pressure the enemy.” Tanker traffic fell 95–100% within 72 hours. Brent closed above $100 on Thursday for the first time since August 2022. This sees us go baclk to our commodity roots, so do please join in if you’re interested!

IMPORTANT NOTE: We are presently in the process of getting a license with a major regulator, and while that process is ongoing we are not able to publish the portfolio update and company notes. We’ll do a big reveal of the new plans as soon as we’re in a position to do thusly. We apologise for it taking time, but this is unfortunately a fact of life. With that we’re also putting the opinion part of this behind the wall.

NOTE: Panda+ is now closed to new joiners. We thank everyone for their interest and custom.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

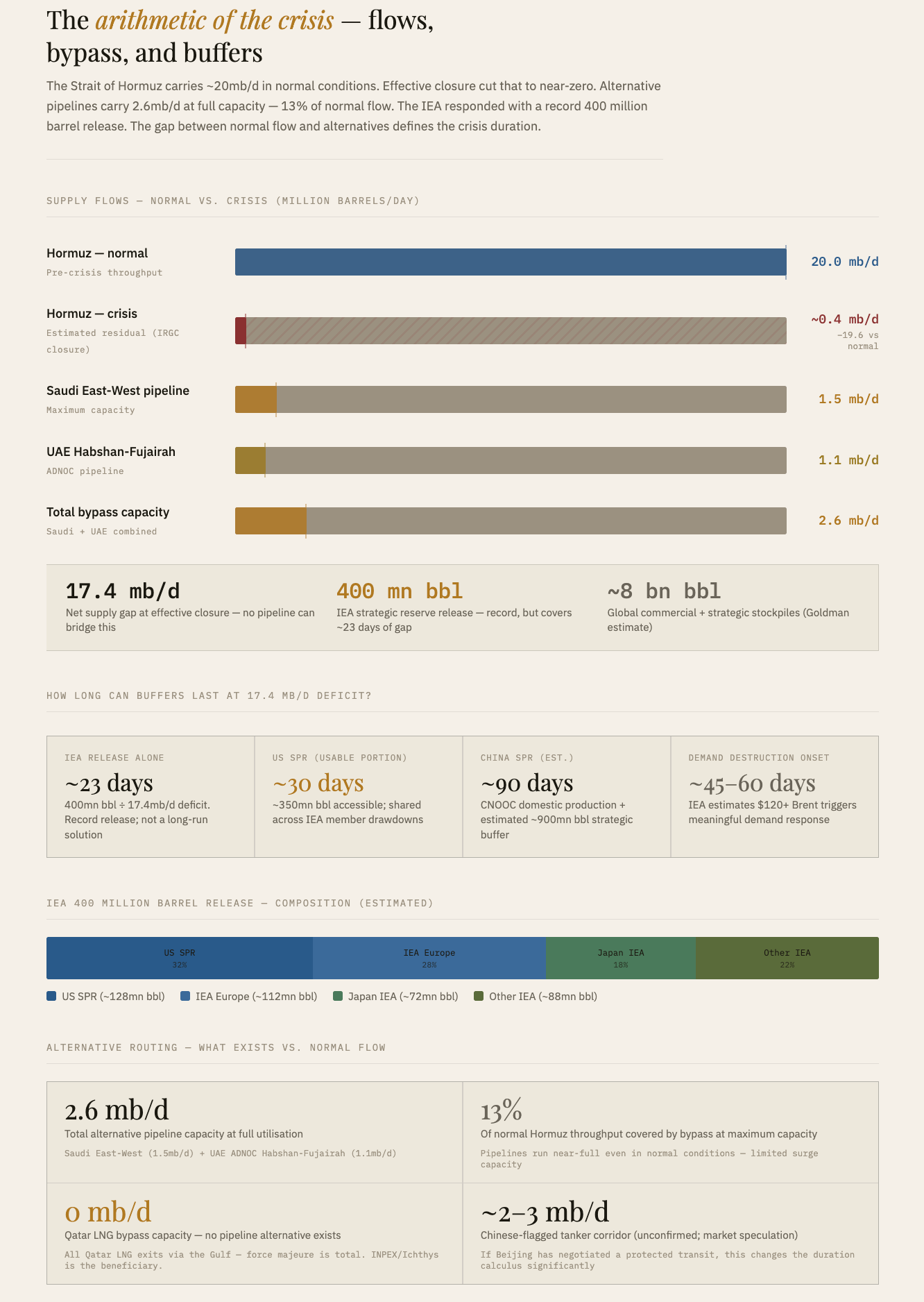

Let re-establish come of the basics of why this is important, just in case you’ve missed the numbers being blared from every corner of FinTwit and Business TV: twenty million barrels per day, which is roughly one-fifth of global petroleum consumption - flowed through that 21-mile-wide passage daily. It also carried about 20% of global LNG trade, primarily from Qatar’s North Field. QatarEnergy has already declared force majeure after Iranian drone strikes on Ras Laffan. The IEA just announced the largest emergency reserve release in its history: 400 million barrels. Analysts at Rapidan Energy note that even this extraordinary measure can “at best only offset a fraction” of the roughly 15 million bpd net supply loss. Goldman models a 2 million bpd structural shortfall even in a base case.

The question we want to sit with in this piece is not “will oil go higher?” - it might, it might not, the IEA release and potential US naval escorts create genuine uncertainty around the near-term price path. The question is: where in the APAC energy complex does the Hormuz closure create durable, defensible earnings power that the market hasn’t yet fully priced? And where does it create a value trap dressed up as an oil play?

The Geography of Pain

APAC is where this crisis hurts most. The US EIA estimated that 84% of crude flowing through Hormuz was destined for Asian markets. China, India, Japan, and South Korea together accounted for 69% of all Hormuz crude flows. The asymmetry of vulnerability is stark and creates a first analytical cut: import-dependent economies with limited bypass optionality are structurally disadvantaged, while domestic producers and non-Gulf exposed upstream assets become enormously more valuable.