Wired for Conflict

A Panda's Guide to Copper and Aluminium in the Age of Tariffs, Tankers, and Terawatts

Good Morning,

Sometimes things keep us up at night. Sometimes they go on to do thusly for a prolonged period of time. The pandas were grappling with the notion of what metals are in this day and age for some time. What is Dr. Copper in a world with no recessions? does it’s Econ PhD get taken away, and if so how do we trade it? what about Ali as a consumer proxy, when its industrial use if going through the roof? All these have been in the background for us for some time, and we were looking to do a comprehensive metal update, but then the US and Israel struck Iran and we now have the pressure cooked of geopolitical uncertainly applied ot all those trends. We could hold back no longer. Here’s the long-awaited magnum opus on Aluminium and Copper in this day and age.

A quick reminder that this isnt the first piece, as we have covered Aluminium and copper producers before. Do please check out out earlier works:

Aluminium enters the fray

Zijin Feature: The Chinese Copper Leader

MMG and CMOC: the rest of the group

What follows is a long and detailed review and update of the original thesis, how it changes in the present. Well worth your time, even if we do say so ourselves.

IMPORTANT NOTE: We are presently in the process of getting a license with a major regulator, and while that process is ongoing we are not able to publish the portfolio update and company notes. We’ll do a big reveal of the new plans as soon as we’re in a position to do thusly. We apologise for it taking time, but this is unfortunately a fact of life. With that we’re also putting the opinion part of this behind the wall.

NOTE: Panda+ is now closed to new joiners. We thank everyone for their interest and custom.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

Where We Are and How We Got Here

Regular Panda Perspectives readers will recall our Copper Chronicles series from late 2024, where we laid out the structural bull case for copper and profiled the leading Chinese producers. This piece is the comprehensive update we have been meaning to write: the thesis has not only survived contact with reality, it has strengthened. But the path has been anything but smooth.

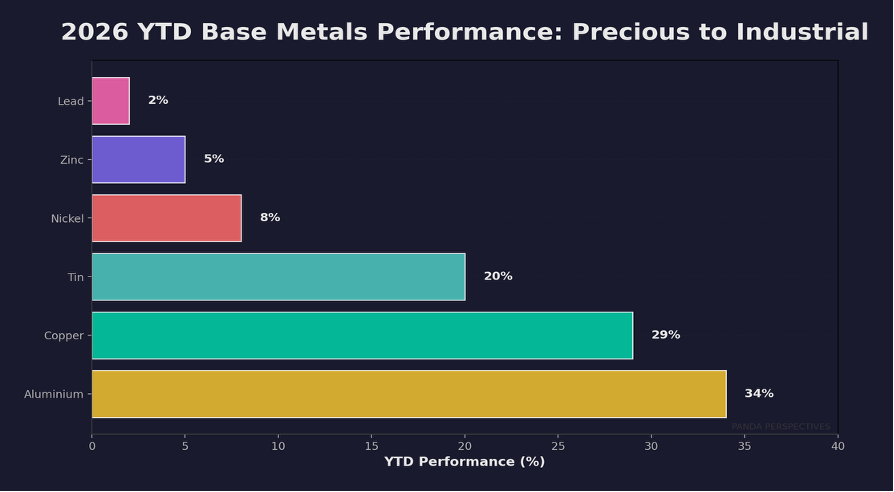

It has been a turbulent start to 2026 for industrial metals. Copper, the commodity most closely tied to the global electrification story, traded as high as $14,527 per tonne intraday on January 29th before pulling back to around $12,250 as of mid-March. Aluminium has had a more steadily bullish run, surging past $3,300 per tonne to trade at $3,342 as of March 18th, its highest level since the post-Covid commodity surge, and outperforming copper on a year-to-date basis with a roughly 34% gain versus copper’s 29%.

The key story is the collision of forces acting on these markets. On the one hand, the structural demand thesis for both metals has never been stronger. On the other, the immediate environment is clouded by a volatile mix of tariff uncertainty, Middle Eastern conflict, and the continued drag from China’s property sector.

Consider how far both metals have come. Copper began 2025 in the low $9,000s per tonne, weighed down by China property concerns and a strong dollar. The rally that followed was driven by a convergence of factors: better-than-expected Chinese manufacturing data, growing recognition of the scale of electrification demand, and a series of supply disruptions that progressively tightened the physical market. By October 2025, copper had crossed $11,000. By January 2026, it was flirting with all-time highs above $14,000 before profit-taking and tariff uncertainty pulled it back.

Aluminium’s journey has been less dramatic in its peaks and troughs but arguably more impressive in its consistency. From around $2,500 per tonne in early 2025, the metal ground steadily higher through the year, supported by rising energy costs in Europe, China’s smelting capacity cap, and growing demand from automotive lightweighting and power transmission. The acceleration in early 2026, which took aluminium through $3,000 and beyond, was catalysed by the Middle Eastern crisis and the resulting supply disruption at Alba.

Looking across the broader base metals complex, the performance dispersion in 2026 tells its own story. Aluminium and copper lead the pack, reflecting their direct exposure to both the electrification theme and supply-side constraints. Tin has performed well on electronics demand. Nickel, zinc, and lead have lagged, lacking the same structural demand catalysts.

Exhibit 1: 2026 YTD performance across the base metals complex. Aluminium and copper lead, reflecting their dual exposure to electrification demand and supply constraints. The performance gap between the top and bottom of the complex highlights the selective nature of the current rally. Source: LME, Trading Economics.

The Middle East: Aluminium’s Black Swan

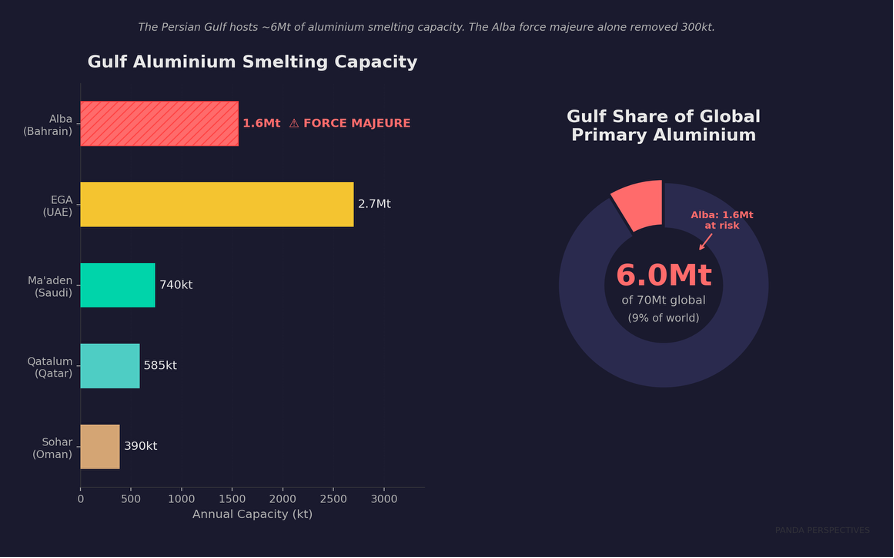

The most acute short-term disruption came from the Middle East. Escalating tensions in the Persian Gulf region reached a critical point in early March when Aluminium Bahrain (Alba), one of the world’s largest smelters with annual capacity of approximately 1.56 million tonnes, declared force majeure on aluminium deliveries and began a controlled shutdown of approximately 300,000 tonnes per year of capacity. The trigger was the effective blockade of the Strait of Hormuz, which disrupted both outbound metal shipments and inbound alumina supply. For a smelter that operates on a continuous basis and cannot simply be switched on and off, this represented a serious operational crisis.

Exhibit 2: Gulf aluminium smelting capacity at risk. The Persian Gulf hosts nearly 6Mt of primary aluminium capacity, roughly 8-9% of global production. The Alba force majeure in March removed 300kt directly, but the broader risk is that further escalation could threaten the entire regional complex. EGA alone produces 2.7Mt, making it the largest single-site smelter outside China. Source: company reports, CRU Group, author estimates.