China Weekly Wrap: Markets, Macro & Tech – Key Developments This Week

a week that was 30 June - 5 July 2025

Good Morning, And if you're reading from the U.S., Happy Fourth‑of‑July weekend—feel free to dip into this wrap between the brisket and the fireworks.

We stayed firmly in healthcare‑land this week, adding two more pieces to the series we kicked off a fortnight ago:

Medical Devices — Value‑Based Pricing Meets Global Ambition (published Tuesday): how VBP pressure is forging cost‑efficient innovators like Mindray, United Imaging and SNIBE, and why their export push is still under‑owned.

Biotech & Pharma — Pipelines, Policies, Valuations (published Thursday): a bottoms‑up scan of CSPC, Hansoh, Hengrui, Innovent, BeiGene and Sino Biopharm, plus our updated screen of “growth at a rational price” names.

Coming up next week: Platforms, Hospitals & CDMOs. We’ll dissect JD Health vs. Ali Health, urban private‑hospital roll‑ups, and whether WuXi’s valuation gap to global CRO peers is justified.

Join up if you’re interested as all the pieces are paywalled.

This Sunday will see the release of the Panda Portfolio Update. The portfolio has some activity planned, but none executed yet. This remains a premium feature that full subscribers have access to.

Level‑up your Asia Edge

Our Substack is just your starter. For the full course that includes actionable calls, custom decks and live Q&A consider a Bespoke Panda Service.

What we’re helping clients with right now • China’s fast‑shifting consumer wallet

• The 2Q25 macro path & policy pivots

• Factory automation & the robotics super‑cycle

Keen to sharpen your edge? Check out our advisory menu or drop us a note to get started.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

📊 Weekly Relative Performance Observations

Week of June 30 – July 4, 2025

Broad Takeaway

Asian markets saw mixed performances this week, with Turkey’s BIST 100 surging +9.2%, far outpacing regional peers, while Chinese equities posted modest gains. Hong Kong equities underperformed slightly, with the Hang Seng Index down -1.52% despite stabilising turnover. Mainland A-shares were more resilient, aided by continued policy support signals and cautious optimism on economic stabilisation.

Volatility remained subdued across the region, reflecting a market tone of cautious positioning ahead of upcoming mid-year data releases and global central bank meetings.

🇨🇳 Performance in Chinese Equities

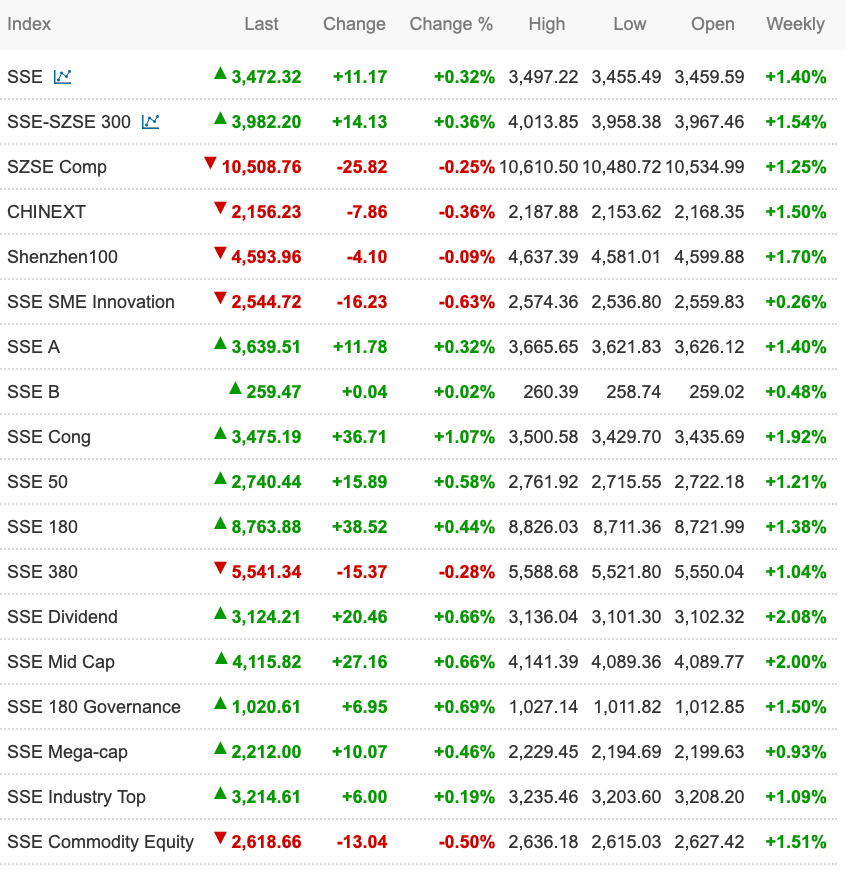

Shanghai Composite (SHCOMP): 3,472.32, +1.40%

The SHCOMP posted a steady gain, supported by SOEs, financials, and defensive cyclicals. While daily turnover was moderate, breadth improved, indicating broad-based buying in value and policy-linked sectors.

CSI 300 (SHSZ300): 3,982.20, +1.54%

Large-cap A-shares outperformed slightly, driven by financials, insurance, and industrials. Investor sentiment improved on expectations of further targeted easing and stabilising FX, with foreign institutional flows remaining net positive.

ChiNext Index (CHINEXT): 2,156.23, +1.50%

ChiNext rose moderately, led by biotech and digital health stocks. Growth names benefitted from improving risk appetite, though gains were more contained compared to the sharp rebound in prior weeks.

🇭🇰 Performance in Hong Kong Equities

Hang Seng Index (HSI): 23,916.06, -1.52%

The HSI declined despite supportive Southbound flows. Losses were led by tech (-2.3% weekly) and industrials, offsetting modest gains in property (+2.0% weekly). Investors remained cautious ahead of global macro data, keeping upside capped.

HS Tech Index: 5,216.26, -2.34%

Tech stocks underperformed, with internet and EV ecosystem names seeing profit-taking after recent rebounds. Sentiment remains fragile, with market participants waiting for clearer sector-specific policy catalysts.

HSCEI (China Enterprises Index): 8,609.27, -1.75%

The HSCEI declined, tracking weakness in large-cap Chinese financials and industrials. Flows were subdued, and valuation support was not sufficient to offset incremental profit-taking pressures.

HS Red Chips: 4,091.81, +0.62%

Red Chips outperformed, led by select infrastructure and SOE-linked names, reflecting rotation into defensive policy beneficiaries.

HSI Property Index: +1.99%

Property stocks were a bright spot in Hong Kong this week, driven by hopes of incremental easing measures and sector stabilisation.

VHSI (Volatility Index): 20.16, -1.08%

Volatility declined marginally as traders unwound hedges amid thin holiday-week volumes and limited macro catalysts.

💡 Takeaways for Chinese Equities in a Regional Context

Mainland A-shares resilient: The CSI 300 and SHCOMP outperformed Hong Kong, driven by SOEs, banks, and industrials, reflecting cautious optimism on policy support.

Hong Kong underperformed regional peers: The HSI lagged, weighed down by tech and industrial weakness, though property stocks bucked the trend with gains.

Growth sentiment stable but not euphoric: ChiNext posted modest gains, signalling continued but measured retail risk appetite.

Flows remain policy-driven: Market movements remain linked to incremental easing expectations and FX stability rather than fundamental earnings upgrades.

🌏 Regional Peers – Weekly Performance

🇹🇷 BIST 100 (Turkey): +9.24%

Turkey surged as easing FX pressures and central bank confidence boosted equities sharply.

🇹🇼 FTSE TWSE Taiwan 50: +0.06%

Taiwan equities were flat on the week. Semiconductor giants, particularly TSMC, saw profit-taking after a strong run in June. AI optimism remains intact, but investor positioning turned cautious amid stretched valuations and ahead of upcoming Q2 earnings results. Broader market volumes moderated, indicating a pause in aggressive inflows.

🇯🇵 TOPIX: -0.44%

Japanese equities slipped slightly this week as yen volatility weighed on exporter sentiment. Auto, machinery, and electronics stocks traded defensively, offsetting modest gains in banks and trading houses. The Bank of Japan’s steady policy stance supported the macro backdrop, but investors remain wary of currency-induced earnings pressures.

🇮🇳 NIFTY 50: -0.69%

India’s benchmark consolidated recent gains, declining modestly as banks, PSUs, and infrastructure stocks faced profit-taking. The market remains structurally strong following post-election stability, but near-term flows turned cautious pending budget announcements and potential fiscal clarity in coming weeks.

🇵🇭 Philippines PSEi: +0.60%

The PSEi advanced modestly, led by gains in financials and select consumer names. Investor focus is turning to potential policy moves in H2 to support growth amid mixed macro data releases, including inflation and remittance trends.

🇮🇩 FTSE Indonesia: +0.30%

Indonesia posted small gains as banking stocks held steady while commodity-linked sectors, particularly coal and palm oil, lagged. Political transition uncertainty and fiscal recalibration remain market watchpoints, tempering investor conviction despite attractive valuations.

🇦🇺 ASX 200: +0.10%

Australia’s market ended broadly unchanged. Weakness in materials (iron ore and base metals) and energy offset gains in banks and consumer staples. Investors await clearer signals from China’s industrial and property sectors to guide commodity demand outlooks, with miners underperforming this week.

💡 Key Observations for Asia

China’s mainland equities outperformed most regional peers this week, with both the CSI 300 and Shanghai Composite posting steady gains, while Hong Kong lagged due to tech and industrial weakness. Improved FX stability, incremental policy signals, and cautious optimism on domestic economic data underpinned sentiment in China.

Turkey stood out with an exceptional +9% rally, driven by FX stabilisation and bank-led gains, far outpacing Asian markets. However, the sustainability of this surge remains contingent on macro and policy credibility.

Asia’s tech leadership remained anchored in Taiwan, though the Taiwan 50 index was broadly flat this week as semiconductor names saw profit-taking. In contrast, China’s growth sectors – especially ChiNext biotech, automation, and digital health – posted moderate gains, suggesting selective reallocation into Chinese growth following recent underperformance.

Japan’s equities slipped slightly, reflecting the market’s continued currency dependency. Exporter sentiment remains sensitive to yen volatility despite a supportive policy backdrop, limiting upside conviction.

India’s market dipped modestly this week, consolidating recent post-election gains. Strong domestic flows and political stability continue to provide a robust structural underpinning, though near-term flows turned cautious ahead of budget announcements.

Southeast Asia delivered muted performances, with the Philippines and Indonesia gaining marginally. Commodity-linked names underperformed, particularly in Indonesia and Australia, reflecting softer global commodity trends and cautious investor positioning.

Overall, Asia posted mixed results this week, with China’s mainland equities regaining relative strength while Hong Kong underperformed. Investors are tactically re-engaging in Chinese A-shares amid stabilising macro conditions, while maintaining core overweight positions in India and Taiwan and a balanced exposure to Japan’s industrial cycle.

📰 In the News This Week

🇨🇳 China-US Trade Signals Improve

Announced by: Ministry of Commerce | Date: July 4

China’s Ministry of Commerce stated that the US has informed China of plans to cancel some restrictive measures. Both sides are working to implement outcomes from the London Framework, and China is reviewing applications for export licenses of controlled items. Beijing urged Washington to “continue to work in the same direction and correct wrong practices.”

Interpretation: Suggests tentative progress in US-China trade discussions, aligning with recent diplomatic efforts to stabilise bilateral economic ties. Potential easing of restrictions could benefit technology, semiconductors, and industrial supply chains, though market scepticism remains pending formal announcements.

🇨🇳 New Child Rearing Subsidy Policy Finalised

Announced by: CPC Central Committee and State Council | Date: June 19, effective January 1, 2025

China formalised the Implementation Plan for Child Rearing Subsidies, granting annual subsidies (RMB 3,600 per child under age 3) to boost fertility rates and reduce household financial burdens. The scheme emphasises streamlined application procedures, local government oversight, and alignment with broader demographic support policies.

Interpretation: Reinforces Beijing’s structural demographic response, aiming to address declining birth rates by reducing early childcare costs. Signals a policy shift toward direct fiscal incentives to support family formation and counter long-term population decline risks.

🇨🇳 State-Owned Enterprises’ Strategic Role Reaffirmed

Comment by: Jiang Xiaojuan (Tsinghua University & State Council) | Date: June 29

Jiang Xiaojuan highlighted that SOEs are expected to “perform supplementation in sectors the private economy is unable or unwilling to engage with,” framing SOE expansion as the “execution of a strategic mission.” She referenced the 20th Third Plenum’s call to direct SOE capital into key industries critical to economic security and livelihood.

Interpretation: Signals continued strategic prioritisation of SOEs in critical and emerging sectors, consolidating state influence where private firms lack scale or willingness. Investors should anticipate ongoing SOE-led initiatives in advanced manufacturing, energy security, and technological infrastructure.

📉 Domestic Smartphone Shipments Decline Sharply

Reported by: CAICT | Date: July 4

China’s domestic smartphone shipments fell -21.8% y/y in May to 23.72 million units. Shipments of foreign branded phones (including Apple) within China also declined -9.7% y/y to 4.54 million units.

Interpretation: Reflects ongoing weakness in discretionary consumer demand, intensified market saturation, and longer replacement cycles. May weigh on smartphone OEMs, component suppliers, and retail channels in the near term.

🇨🇳 Anti-Dumping Ruling on Brandy Imports

Announced by: Ministry of Commerce | Date: July 4

China stated it will not impose anti-dumping duties on imported brandy if products are sold no cheaper than agreed commitment prices.

Interpretation: A pragmatic trade stance designed to balance domestic producer protection with consumer price stability and bilateral trade relations, particularly with major brandy-exporting nations in Europe.

⚙️ SHFE Warehouse Stocks – Weekly Update

Reported by: Shanghai Futures Exchange | Date: July 4

Copper: +3,039 tonnes (+3.73%)

Aluminum: +342 tonnes (+0.36%)

Zinc: +1,731 tonnes (+3.97%)

Lead: +1,374 tonnes (+2.65%)

Nickel: +204 tonnes (+0.83%)

Tin: +243 tonnes (+3.49%)

Rubber: -2,148 tonnes (-1.00%)

Interpretation: Inventory builds across most base metals suggest weaker near-term physical demand or pre-emptive restocking amid price volatility. Rubber stocks declined modestly, indicating stable downstream demand.

📊 Macro Data Review

It was a moderately busy data week in China, dominated by June PMI releases. The macro tone remains cautiously stabilising: manufacturing remains under pressure but shows tentative improvement, while services growth moderated slightly. The overall narrative continues to be one of fragile recovery without decisive new catalysts.

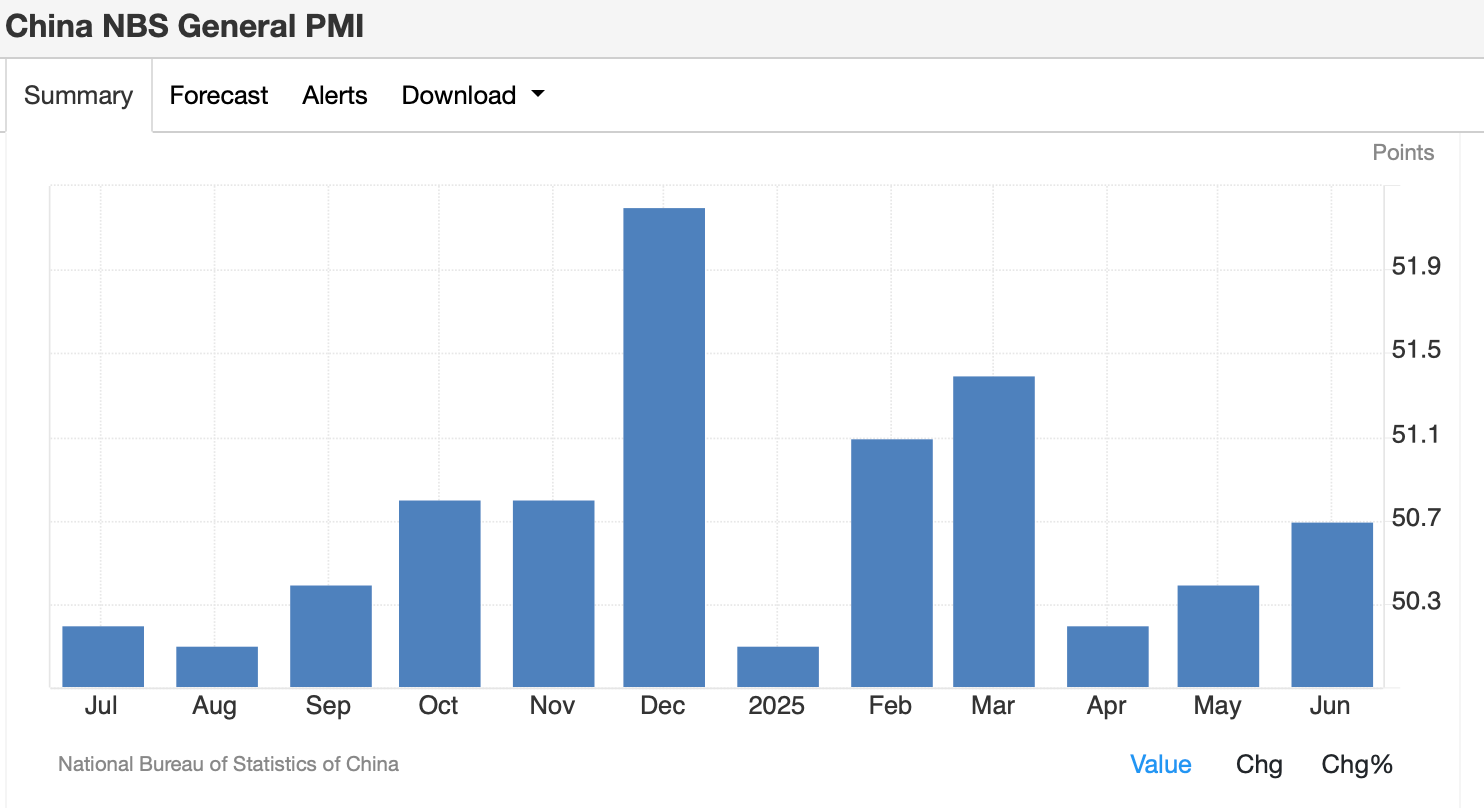

🏭 NBS PMIs (June)

NBS Manufacturing PMI: 49.7

(Consensus: 49.7 | Previous: 49.5 | Forecast: 50)

NBS Non-Manufacturing PMI: 50.5

(Consensus: 50.3 | Previous: 50.3 | Forecast: 50.5)

NBS Composite PMI: 50.7

(Previous: 50.4 | Forecast: 50.7)

This Indicates:

The official manufacturing PMI remained in mild contraction territory for a second month, signalling that industrial production continues to face headwinds from weak domestic orders, limited pricing power, and cautious restocking by firms. However, the small uptick from May’s 49.5 suggests marginal improvement in operating conditions, with output and employment sub-indices stabilising.

The non-manufacturing PMI edged up to 50.5, supported by construction activity and modest expansion in services, albeit below the average pre-pandemic trend. The composite PMI rose to 50.7, reinforcing a picture of gradual economic stabilisation, underpinned by infrastructure spending and targeted easing measures.

Overall, the NBS PMIs highlight:

Continued fragility in manufacturing amid lacklustre demand.

Relative resilience in services, although growth remains sub-trend.

An aggregate stabilisation but with no signs yet of a strong cyclical upswing.

🏭 Caixin PMIs (June)

Caixin Manufacturing PMI: 50.4

(Consensus: 49.0 | Previous: 48.3 | Forecast: 49.2)

Caixin Services PMI: 50.6

(Consensus: 51.0 | Previous: 51.1 | Forecast: 51.3)

Caixin Composite PMI: 51.3

(Previous: 49.6 | Forecast: 50.2)

This Indicates:

The Caixin manufacturing PMI surprised to the upside, rising back into expansion (above 50) for the first time since March. The improvement was driven by new orders, output growth, and an uptick in export demand, particularly benefitting small and export-oriented manufacturers. Input cost pressures remained contained, supporting slight margin improvement.

The Caixin services PMI, however, eased to 50.6 from 51.1, below consensus. The slowdown reflects softening in consumer-facing segments such as catering, travel, and retail services, as households remain cautious amid income and employment uncertainties.

The composite PMI rose to 51.3, indicating overall economic activity is expanding modestly, with manufacturing recovery offsetting deceleration in services.

Key takeaways from Caixin PMIs:

Private sector manufacturing momentum is improving, contrasting with the still-contractionary NBS measure that skews towards larger SOEs.

Services growth is losing steam, suggesting the consumer recovery remains uneven and fragile.

The broader economy is stabilising at low expansion levels, consistent with policy focus on maintaining steady growth rather than seeking aggressive stimulus-driven surges.

Overall Macro Implication

June PMI data portray an economy experiencing gradual stabilisation with divergent sector trends. Manufacturing shows early signs of improvement among private and export firms, while services lose some momentum. These results:

Reinforce expectations of continued targeted easing ahead of the July Politburo meeting.

Suggest policy support remains necessary to sustain growth, with limited spillover yet into household consumption and private capex.

Do not fundamentally alter market sentiment but provide tentative reassurance that downside risks are being contained.

🏢 Company News & Results

XPeng XPEV 0.00%↑ Launches World’s First L3 AI Car

Date: July 3

XPeng announced the launch of the world’s first L3-level AI autonomous driving car, the G7, starting at RMB 195,800.

This Indicates:

XPeng is pushing aggressively into advanced assisted driving, aiming to differentiate in a crowded EV market through AI-led features. The L3 launch strengthens its technological credentials and could trigger competitive responses from peers such as Li Auto, NIO, and Huawei Aito, as the race to deploy higher-level autonomy intensifies. The sub-RMB 200k pricing positions it directly against mid-tier family SUVs, challenging both legacy ICE models and fellow EV brands on value-for-tech metrics.

Alibaba BABA 0.00%↑ Expands Southeast Asia Data Centres to Drive AI Growth

Date: July 2

Alibaba Cloud announced expansion of its data centre footprint in Malaysia (third centre) and the Philippines (second centre by October) to support AI growth. Additionally, it is establishing a global AI competency centre in Singapore to assist over 5,000 businesses and 100,000 developers with advanced AI models. CEO Eddie Wu stated Alibaba plans to invest over $53 billion in AI infrastructure globally over the next three years.

This Indicates:

Alibaba is doubling down on its global cloud and AI strategy to regain leadership against Microsoft Azure, Amazon AWS, and Huawei Cloud. The Southeast Asia expansion leverages strong regional digitalisation demand, while the Singapore AI centre builds developer ecosystem lock-in. The aggressive capex reiterates AI and cloud as core growth pillars despite competitive and regulatory pressures at home.

ByteDance (Douyin) – Sets Up Gaming Division

Date: July 2

Reports indicate ByteDance’s Douyin has established a new game publishing division, aiming to integrate game distribution into its core platform and leverage its short video ecosystem for in-app gaming traffic monetisation.

This Indicates:

ByteDance is re-entering gaming strategically after past regulatory and competitive setbacks, seeking to monetise its vast daily active user base and boost average revenue per user (ARPU). The move intensifies competition with Tencent, NetEase, and Bilibili in mobile gaming distribution and may face close regulatory scrutiny given content controls.

Complete Index Performance List:

🧭 General Trends

Chinese equities delivered a mixed but rotational week. Mainland indices posted modest gains led by large caps, while Hong Kong underperformed slightly, with property and selected SOEs providing support against tech and industrial weakness.

Investor tone remains cautiously constructive. Macro data (PMIs) pointed to fragile stabilisation, while policy headlines (US trade signals, child subsidies, AI industrial strategy) provided incremental optimism. Sector rotation rather than fresh inflows continues to define market price action, with defensive positioning alongside selective growth buying.

📈 Mainland Indices: Resilience Amid Mixed Flows

Shanghai Composite (SSE): +1.40%

CSI 300: +1.54%

ChiNext: +1.50%

Shenzhen 100: +1.70%

SSE SME Innovation: +0.26%

SSE Commodity Equity Index: +1.51%

SSE Conglomerate Index: +1.92%

🔍 Interpretation: Mainland markets extended stabilisation gains, with CSI 300 and ChiNext posting moderate advances. Large-cap financials, SOEs, and innovation names led the rally, supported by policy expectations ahead of mid-year meetings. The broad-based rise reflects cautious re-risking but no decisive momentum shift.

📉 Offshore Indices: Weakness in Tech and Industrials Offset Property Gains

Hang Seng Index (HSI): -1.52%

HS Tech: -2.34%

HSCEI (China Enterprises): -1.75%

HSI Financials: -1.31%

HSI Property: +1.99%

HSI Industrials: -1.96%

VHSI (Volatility): -1.08%

🔍 Interpretation: Hong Kong equities declined, led by tech and industrials, while property stocks posted gains on incremental mortgage easing expectations. The muted volatility suggests cautious positioning rather than aggressive de-risking. Flows remained light, with market participants awaiting stronger macro or earnings catalysts.

🧪Sector & Style Trends

🚗 EVs & Autos: Tactical Divergence Across Names

BYD Co. (1211.HK): +0.13%

Geely Auto (0175.HK): +0.09%

Xiaomi-W (1810.HK): +0.77%

Li Auto-W (2015.HK): +0.46%

Comment: EVs traded flat to slightly higher. Xiaomi shares rose marginally on AI and smart EV strategy optimism, while Li Auto rebounded modestly after recent declines. BYD and Geely posted fractional gains, reflecting muted sentiment despite stable June delivery data.

Strategic Takeaway: Investors remain cautious on the sector’s overcapacity risks, awaiting July’s production and pricing data for clearer directional conviction.

💊 Biotech & Healthcare: Resilient Despite Volatility

Hansoh Pharma (3692.HK): -0.32%

Wuxi Bio (2269.HK): +0.41%

Sino Biopharm (1177.HK): +1.45%

Ali Health (0241.HK): -13.17%

Comment: Biotech names saw mixed performance. Wuxi Bio and Sino Biopharm gained modestly on technical buying, while Hansoh Pharma edged down. Ali Health fell sharply amid profit-taking after strong YTD gains (+27%). Sector flows indicate selective positioning rather than broad conviction.

🏦 Financials & SOEs: Defensive Tone Continues

Ping An (2318.HK): -0.69%

ICBC (1398.HK): +1.31%

China Life (2628.HK): +1.06%

China Mobile (0941.HK): -0.52%

Comment: Banks and insurers posted mixed returns, with ICBC and China Life gaining modestly amid stable yields and cautious positioning. Telecoms paused as China Mobile dipped slightly after strong YTD performance.

🏘 Property & REITs: Incremental Recovery

China Overseas (0688.HK): -2.19%

Henderson Land (0012.HK): +4.89%

China Resources Mixc (1209.HK): +3.25%

Link REIT (0823.HK): +0.82%

HSI Property Index: +1.99%

Comment: Property developers outperformed the broader market, with Henderson Land and Mixc leading gains on policy easing optimism. China Overseas declined, giving back prior gains. REITs saw mild gains, reflecting stabilising investor sentiment towards real estate amid weak sales but improving policy support.

🥤Consumer & Staples: Soft to Stable

Nongfu Spring (9633.HK): -0.52%

Haidilao (6862.HK): -2.64%

CR Beer (0291.HK): +0.35%

Tingyi (0322.HK): +0.17%

Comment: Consumer staples were mixed, with Nongfu Spring and Haidilao down on cautious household demand data, while CR Beer and Tingyi edged higher on defensive buying. The sector continues to reflect fragile consumption recovery despite occasional tactical inflows.

⚙️ Industrials & Materials: Under Pressure

Xinyi Glass (0868.HK): +9.46%

Zijin Mining (2899.HK): +2.61%

China Shenhua (1088.HK): -0.64%

CNOOC (0883.HK): -0.57%

Comment: Materials posted mixed returns. Xinyi Glass outperformed strongly, while coal and oil names saw marginal declines, reflecting weaker commodity market sentiment this week.

🔍 Strategic Takeaways

Mainland resilience contrasts with offshore caution.

CSI 300 and Shanghai Composite gains reflect incremental policy optimism, FX stability, and domestic fund re-risking, while Hong Kong underperformed due to persistent tech and industrial weakness. The divergence underscores market preference for onshore policy beneficiaries and SOEs over offshore listings exposed to global macro risks.

Sector rotation remains tactical rather than conviction-driven.

Flows into SOEs, large-cap financials, SME innovation, and select biotech names were offset by outflows from tech, industrials, and consumer staples. This rotation reflects a market still driven by short-term policy tradesrather than structural earnings upgrades, with investors repositioning tactically in anticipation of upcoming macro data and Politburo policy outcomes.

Property stabilisation is emerging as a relative bright spot.

Gains in property indices and developers signal rising investor confidence in incremental mortgage easing and funding support measures, despite weak underlying sales data. Positioning is shifting from outright defensive underweights towards cautious tactical longs in higher-quality developers and property services names.

EV sentiment remains fragile amid competitive pressures.

The muted performance in EVs and autos, despite Xiaomi and Li Auto headlines, suggests investor concerns over pricing pressure, overcapacity risks, and profit sustainability outweigh short-term product launch enthusiasm. A sector re-rating will likely require clearer volume and margin resilience in Q3.

Consumption recovery remains uneven.

Consumer staples and discretionary showed mixed moves, highlighting fragile household sentiment and selective brand leadership. Investors continue to favour F&B giants with pricing power (e.g. Nongfu Spring) while avoiding lower-margin discretionary plays.

Positioning is defensive and policy-driven.

Institutional investors maintain overweight allocations in SOEs, insurers, and banks to capture the “policy safety premium,” while selectively rotating into growth names (ChiNext, SME Innovation) for tactical upside. Overall conviction remains low, with net new inflows subdued pending clearer growth catalysts.

Forward outlook is data and policy dependent.

Markets await mid-July macro data releases (credit, industrial production, retail sales) and potential Politburo announcements for further stimulus clarity. Without decisive policy easing or a shift in growth momentum, equity performance is expected to remain range-bound, rotational, and tactical.

⚖️ Bottom Line

This week saw Chinese equities post a mixed but stabilising performance, with mainland markets edging higher while Hong Kong lagged. The CSI 300 and Shanghai Composite advanced modestly, driven by SOEs, financials, and innovation names, while the Hang Seng Index slipped as tech and industrials remained under pressure. Property stocks bucked the trend with incremental gains, supported by easing expectations.

Policy news was cautiously constructive. Beijing and Washington signalled progress on removing restrictive trade measures, while China formalised its first nationwide child-rearing subsidy program – a clear demographic support pivot. The government also reaffirmed its strategic SOE mission, aiming to deploy state capital in sectors deemed critical to economic security, underlining the enduring centrality of SOEs in industrial policy.

Corporate headlines reinforced this pragmatic tone. XPeng launched the world’s first L3-level AI car, signalling China’s push into autonomous driving leadership, while Alibaba expanded its Southeast Asian data centre footprint, committing over $53 billion to global AI infrastructure. In A-shares, micro-cap innovation stocks surged nearly +40% in H1, far outpacing blue-chip indices and raising speculative froth questions.

Yet despite these catalysts, flows remained tactical rather than conviction-led. Investors rotated selectively into policy beneficiaries and growth segments, but positioning stayed defensive amid fragile consumer data and lingering concerns over manufacturing profitability and EV overcapacity risks.

China’s markets this week were not defined by exuberance, but by quiet recalibration – absorbing incremental policy optimism, corporate execution signals, and geopolitical thawing, while awaiting clearer catalysts from upcoming July macro data and the Politburo’s mid-year policy review.

Regards,

Leonid

XPeng going to L3 while dropping LIDAR is really interesting. Especially after LIDAR has come down in cost and bulkiness. Seems like a huge validation to Tesla's approach and an overlooked story. Do you see signs the broader Chinese EV market is moving in that direction as well?