Stirring the Pot

Inflation in the bowl, operators on the menu, and the asymmetry the market won’t price.

Good morning,

There are fresh photographs from yesterday. Jensen Huang, in Beijing as a last-minute addition to President Trump’s delegation for the state dinner with President Xi at the Great Hall of the People on Thursday 14 May, slipped off the official itinerary the next morning and went hutong-walking in Nanluoguxiang. He stopped at No. 69 Fangzhuanchang, the Beijing noodle institution that has been pulling zhajiangmian by hand for years, and ordered the eight-RMB bowl: hand-pulled noodles, fermented soybean sauce, julienned cucumber, fresh garlic. “It’s so good,” he told the crowd that had pressed around him filming on phones. Then he tried a douzhi’er, the gray-green fermented mung-bean drink that is also a Beijing classic and is liked by approximately half the people who try it. He winced. Videos of the wince trended on Weibo by Friday afternoon. To recover, he stopped at the Mixue Bingcheng stand and bought a sweet drink for a few RMB. The most quoted CEO in semiconductors, in a small Beijing shop, queuing with locals, eating one of the most popular dishes in the city, then taste-testing his way through the Beijing beverage cycle. We saw the photographs and laughed. We also thought about them for the rest of the day.

The quality is unbeatable. The affordability is unbeatable. Try walking the same block in Tokyo, Seoul, Singapore or London and finding the equivalent: a same-day-made, just-from-the-stove, locally-sourced bowl for the price of a coffee. You cannot. China’s restaurant and convenience-food sector is producing consumer surplus at a rate that no other developed or near-developed market is able to match. The Jensen photograph is amusing because it confirms what every visitor already knows. It is also worth dwelling on, because consumer surplus is the operator’s foregone revenue, and the question for the next twelve months is whether any of it gets converted into pricing.

There are three parts to that question. First, what the inflation cycle is actually doing under the headline CPI print, particularly to food. Second, why the F&B sector is sitting on better demand than the equity market gives it credit for, but cost pressure that consensus believes cannot be passed on. Third, what happens to a set of names already trading at a 20 to 30 percent year-to-date discount if the consensus is wrong and a meaningful slice of the cost-up cycle can be passed through to the consumer. Eight RMB is what the consumer pays for Jensen’s bowl today. The question is whether that price holds in twelve months, and whether the operator can hold its margin if it does not.

This is the follow-on to Nominal Returns a week ago, where we wrote about PPI turning positive in March and the operating-leverage cycle it triggers. That piece looked at the macro print and the sector earnings response. This one zooms in on the part of the economy that touches the consumer most directly, where the cost cycle and the pricing cycle collide, and where the equity market’s verdict has been the most decisive. We think the verdict is wrong on the names that have a credible pricing playbook. The rest of this piece is the case.

IMPORTANT NOTE: We are presently in the process of getting a license with a major regulator, and while that process is ongoing we are not able to publish the portfolio update and company notes. We’ll do a big reveal of the new plans as soon as we’re in a position to do thusly. We apologise for it taking time, but this is unfortunately a fact of life. With that we’re also putting the opinion part of this behind the wall.

NOTE: Panda+ is now closed to new joiners. We thank everyone for their interest and custom.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

Two speeds in the same basket

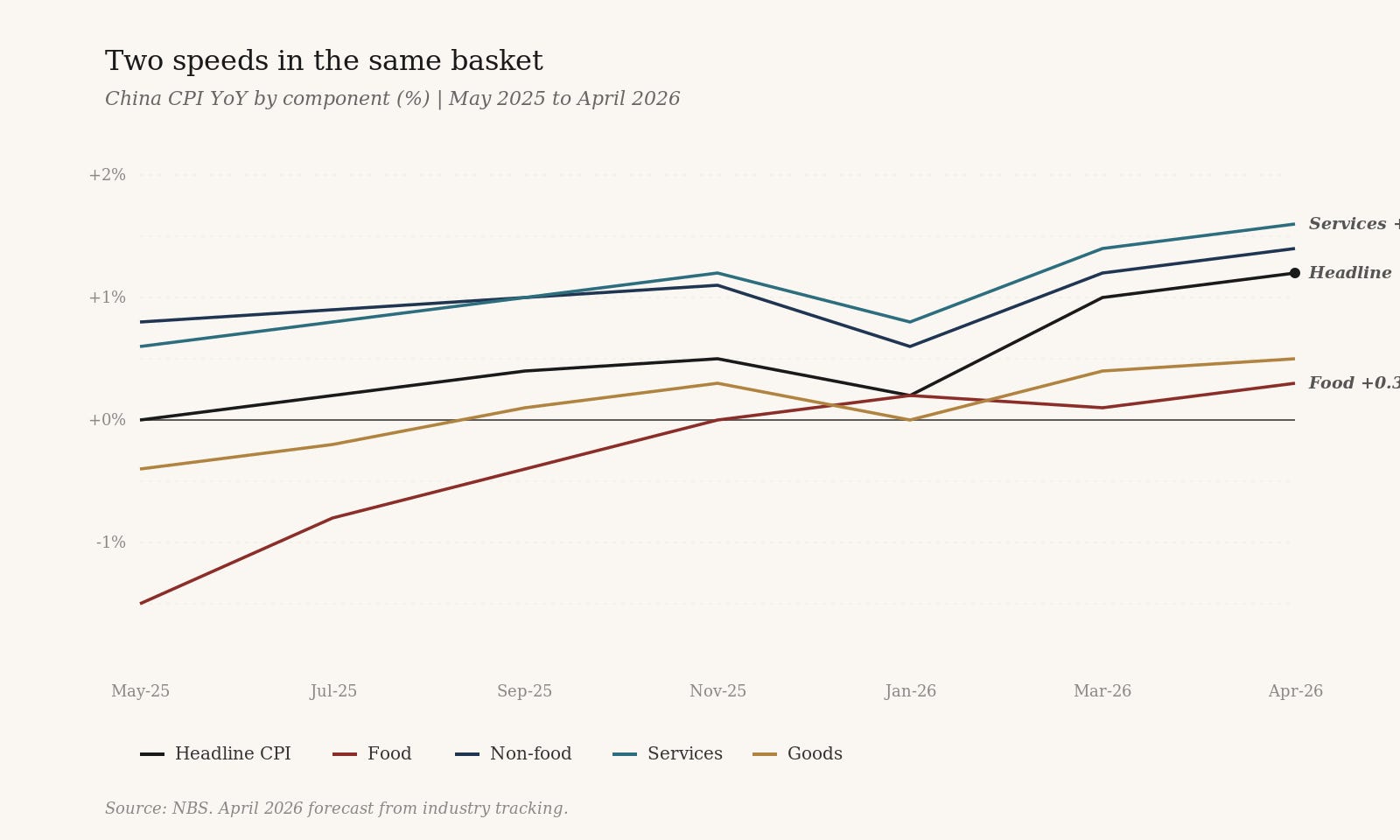

Headline numbers first. China CPI ran +1.0% year-on-year in March and is forecast at +1.2% for April, according to the most recent industry tracking. PPI ran +0.5% in March, the print we wrote about in Nominal Returns, and is forecast at +1.4% for April. Both are accelerating off a deflationary trough. Both have crossed the line from negative to positive. Both are headlines that, on their face, sound healthy.

The composition tells a more complicated story. CPI is being held down by food, which continues to fall outright. CPI is being lifted by services, energy passthrough, and tourism. PPI is being lifted by oil-linked inputs and packaging materials, partially offset by ongoing deflation in agricultural commodities and certain ferrous and chemical sub-segments. The headline indices are converging toward a benign-looking +1 to +1.5%. Underneath, the basket is moving at two very different speeds, and the speeds matter for who can pass through cost and who cannot.