Store of Value

Sun by day, banked by night. Part 2 of a series on China’s electrification.

Good morning,

While the market pours its attention into NVDA 0.00%↑ chips, TSLA 0.00%↑ Megapacks and Elon Musk’s next SPCX 0.00%↑ launch (actual or finacial), the part of the electric build-out that actually decides whether any of it works after dark is being poured much more quietly, in the storage batteries coming out of China. Headlines reward the spectacle at the front of the system, the rocket and the robotaxi and the trillion-dollar accelerator. The backbone sits one layer down, in the cells that bank the power, and the names that own it are far less famous and, for now, a good deal cheaper: CATL, BYD, EVE Energy, Sungrow and the handful of materials makers that have just walked out of a brutal three-year downturn. The same AI boom that made Nvidia the most valuable company on earth has handed those firms a brand-new customer, and almost nobody outside China is looking at it. This is where the power gets banked.

In Too Much Sun, Not Enough Wire we left a thread hanging on purpose. Part 1 walked the build-out, the panels selling below cost and the grid in a once-in-a-cycle boom, and it kept saying that the seam between the two, the thing that turns a glut of intermittent sunshine into power you can use at two in the morning, is the battery. That is this piece. Part 1 was the generation and the wire, Part 2 is the buffer between them that makes the whole system dispatchable, and a later instalment will take the road and the meter, the car, the power market and the operators who sell the electrons. We hold the car back deliberately, because the most important fact in the battery industry right now is that its centre of gravity has just moved off the car and onto the grid, and that is the story worth telling first.

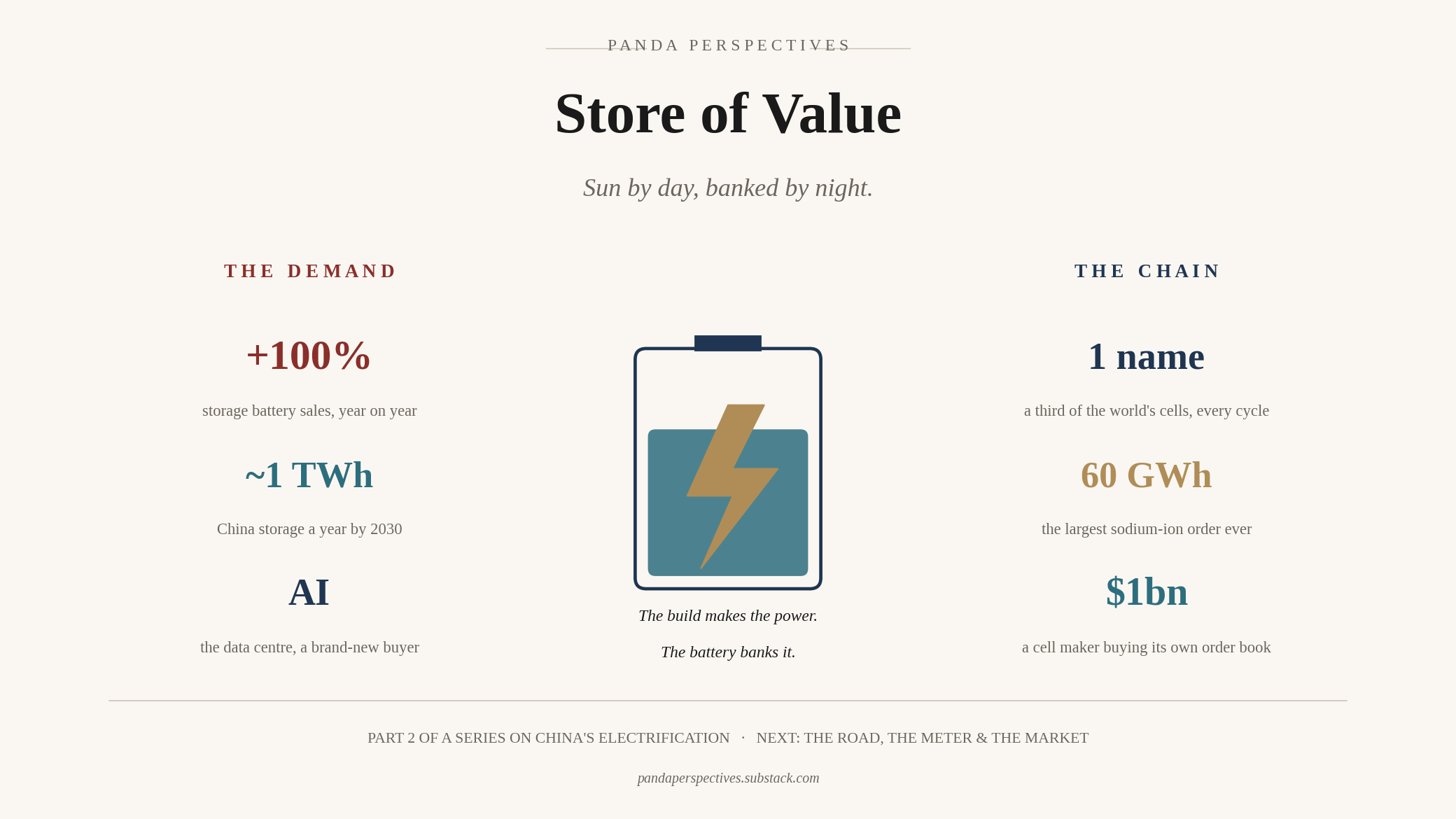

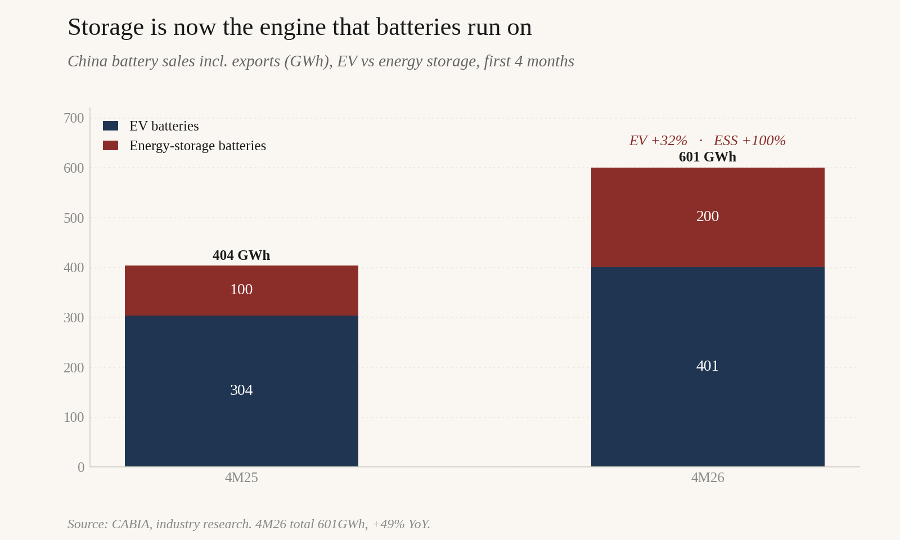

Here is the fact, in one line. China made six hundred gigawatt hours of batteries in the first four months of the year, up forty-nine percent, and inside that number the part going into cars grew thirty-two percent while the part going into storage grew a hundred. Storage has quietly become the engine that the battery industry now runs on. And standing behind it, brand new, is a buyer that did not exist at scale three years ago: the AI data centre, which needs power so clean and so constant that a battery has stopped being a back-up and started being part of the power supply itself.

So we will walk this chain the way we walked the last one. We start with the demand pivot, then go down through the cells, where one company is a through-cycle compounder and the rest are a field of cyclicals, and then into the materials, where a brutal three-year downturn is finally turning from price recovery into profit. Sodium-ion and the cost wall the West is building are the kicker at the end. At every stop we ask the three questions we always ask, what the business does, how profitable it is, and what the market charges for it, all read against the only thing that finally decides the answer, which is how much runway sits in front of it. And the anti-involution thread from the first two pieces runs straight through this one, because the battery industry has lived the supply-side downcycle the solar chain is only now entering, and it has come out the other side more disciplined than it went in.

IMPORTANT NOTE: We are presently in the process of getting a license with a major regulator, and while that process is ongoing we are not able to publish the portfolio update and company notes. We’ll do a big reveal of the new plans as soon as we’re in a position to do thusly. We apologise for it taking time, but this is unfortunately a fact of life. With that we’re also putting the opinion part of this behind the wall.

NOTE: Panda+ is now closed to new joiners. We thank everyone for their interest and custom.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

Part 1. The pivot: storage is the second engine

For a decade the battery was an automotive component. The story was electric-vehicle penetration, the customers were carmakers, and the cycle followed the car. That story is maturing, and a second one has taken over as the growth engine.

The split is stark, and the chart makes it plain. The vehicle line grew a solid third off a large base while storage doubled off a smaller one. One line is maturing and the other is going vertical.

This is not a one-country quirk. On the global numbers, total battery demand for vehicles and storage together is on a path toward well over three terawatt hours by 2027, and the storage slice of that, which was a rounding error a few years ago, is heading toward a terawatt hour and a half on its own. Demand forecasts for the year have been revised up rather than down, and almost all of the upgrade is storage. The car is the large, slowing base. Storage is the thing growing on top of it.

Inside China specifically, stationary storage is compounding at something like forty percent a year and is on track to reach roughly a terawatt hour of annual deployment by the end of the decade, though that headline figure is one we sharpen later, because cells shipped and cells working are not the same thing. The reason for the compounding is the one we built the whole of Part 1 around. A grid stuffed with solar and wind needs somewhere to put the midday surplus so it can be used after dark, and as renewable penetration climbs, the storage attached to it climbs faster. That surplus shows up as curtailment, the clean power a congested grid cannot absorb and simply spills, and storage is the most direct way to monetise what would otherwise be thrown away, even as transmission and dispatch reform chip at the same problem from the other side. Storage is the natural partner of the build we described last time, and it is the part of that build with the steepest demand curve in front of it.