Too Much Sun, Not Enough Wire

Walking the renewables chain, from the polysilicon glut to the grid super-cycle.

Part 1 of a series on China’s electrification.

Good morning,

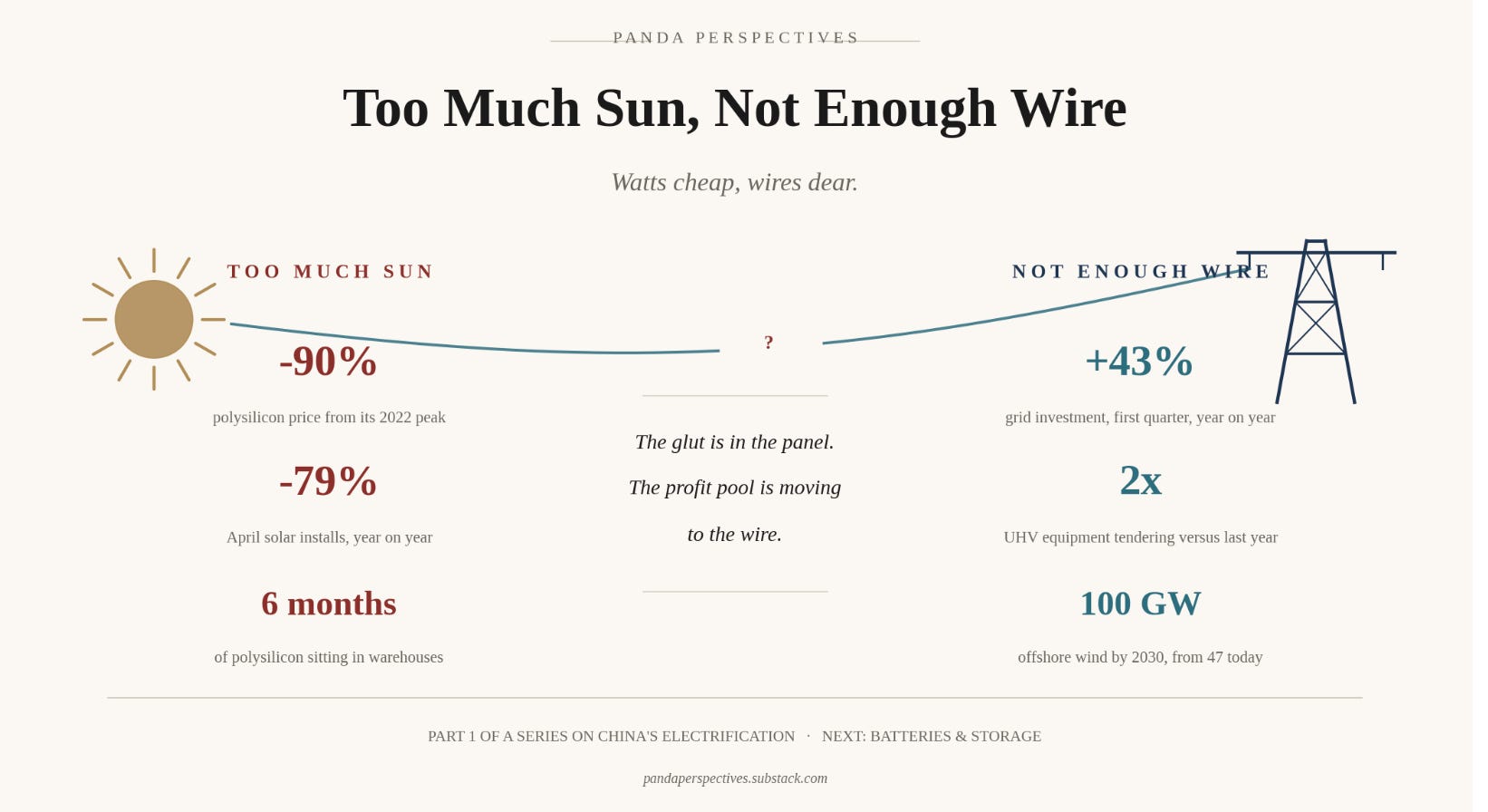

There is a number that frames everything that follows. China installed roughly nine-and-a-half gigawatts of solar in April, down seventy-nine percent on the same month a year earlier. In the same country, in the same quarter, power grid investment grew forty-three percent. One half of the renewables complex is living through the deepest demand air-pocket in a decade. The other half is in the early innings of the largest build-out it has ever seen. They are wired to each other, literally, and they are in completely opposite places.

That tension is the subject of this piece, and it is the reason we are starting a series rather than writing one note. China’s energy transition has become the single largest industrial story in the country, and it is too big to cover in one sitting. So here is the plan. This piece, Part 1, walks the build-out: the manufacturing chain that makes the panels, the inverters and the turbines, and the grid that has to carry what they produce. Part 2 will take on batteries and storage, the buffer that turns intermittent sunshine and wind into power you can actually dispatch when the data centre needs it at two in the morning. We expect a later instalment on the demand side and the power market itself, where the AI build-out, electric vehicles and the operators all meet. We will flag the seams between the parts as we reach them, and we will hold storage almost entirely back for Part 2, because it deserves its own canvas.

The through-line of the series is electrification. The best single piece of strategy work we read this month framed it as the unifying current beneath three otherwise separate forces: a more fractured geopolitics, an AI capital-expenditure supercycle, and the energy transition itself. Each of those drives power demand, and power demand is the thing that ties the panel to the wire to the battery to the chip. We wrote in Nominal Returns and Stirring the Pot about anti-involution, the slow, policy-backed clearing of industrial overcapacity that began in steel and is now working through solar, and that thread runs straight through this piece. Solar is the textbook case of the glut. The grid is the textbook case of the build. We will walk from one to the other, and at each stop we will ask the three questions we always ask: what does the business do, how profitable is it, and what is the valuation, all of it read against the only thing that finally decides the answer, which is how much runway sits in front of it.

IMPORTANT NOTE: We are presently in the process of getting a license with a major regulator, and while that process is ongoing we are not able to publish the portfolio update and company notes. We’ll do a big reveal of the new plans as soon as we’re in a position to do thusly. We apologise for it taking time, but this is unfortunately a fact of life. With that we’re also putting the opinion part of this behind the wall.

NOTE: Panda+ is now closed to new joiners. We thank everyone for their interest and custom.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

Part 1. The current underneath everything

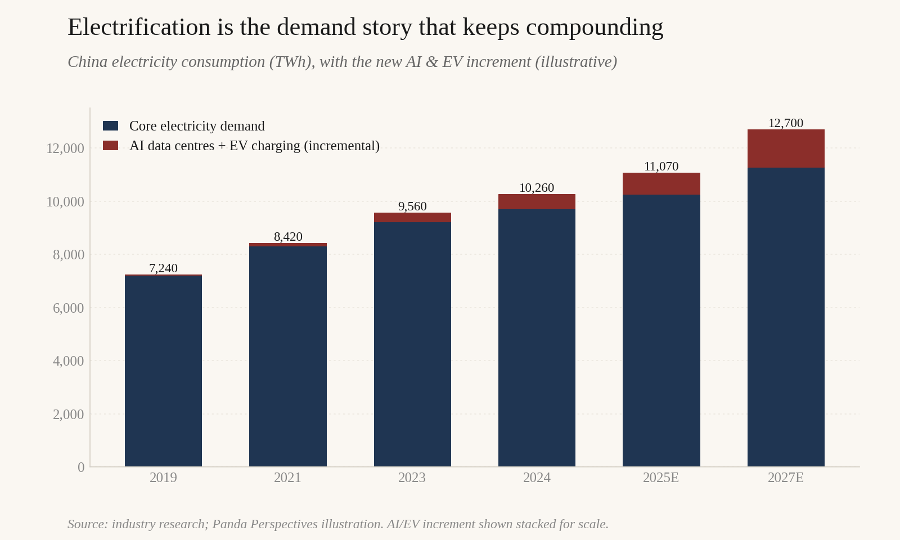

Start with demand, because demand is what makes the whole chain worth building. China’s electricity consumption has roughly doubled since the mid-2010s and is still compounding at mid-single digits a year, in a developed-scale economy where most Western grids are flat. The base is industry, buildings and transport. The increment, the part that is new, is the part that matters: electric vehicles drawing from the wall, and the AI data centre, which has quietly become a grid-planning variable in its own right.