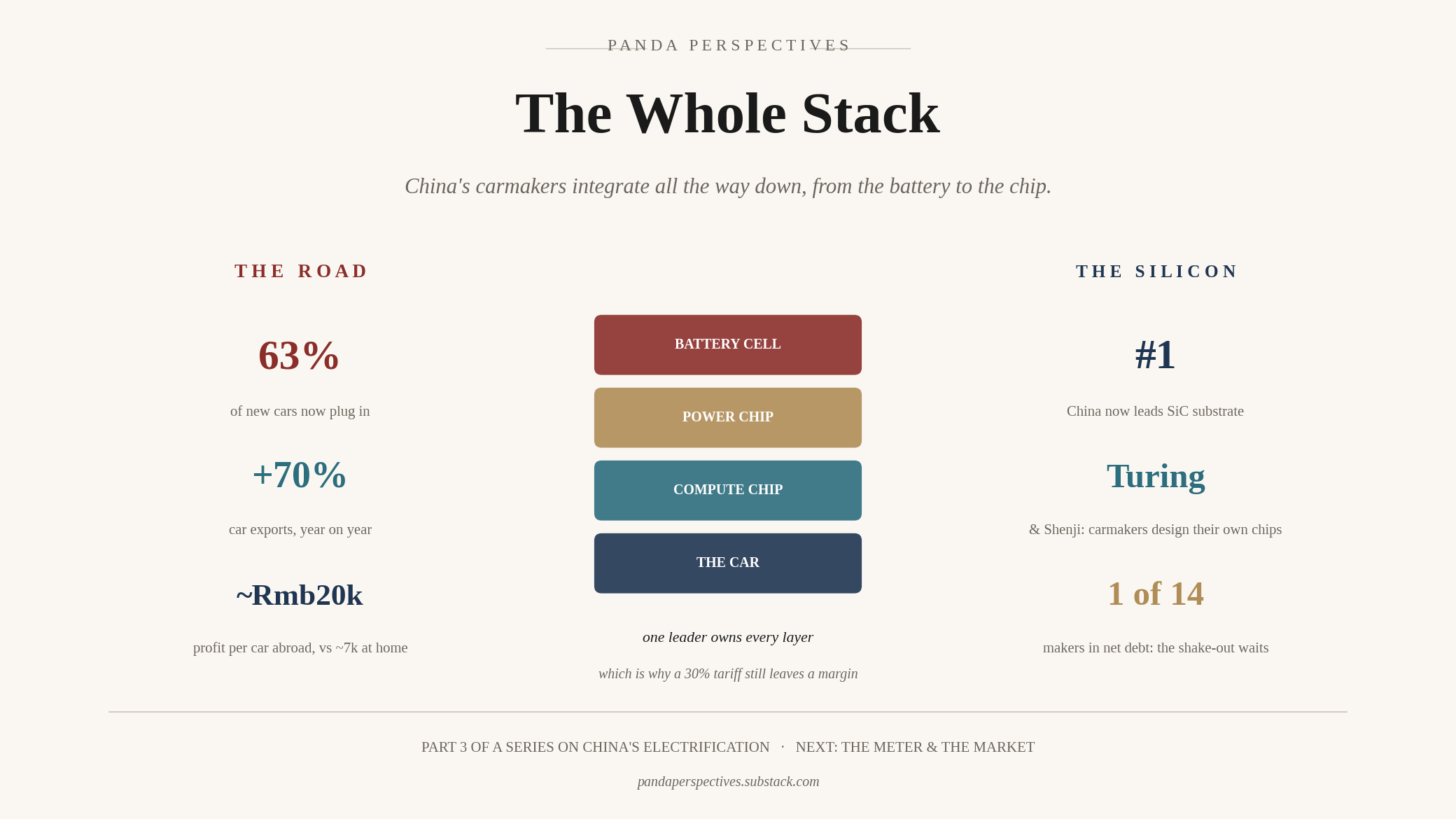

The Whole Stack

China’s carmakers are integrating all the way down, from the battery to the chip. Part 3 of a series on China’s electrification.

Good morning,

In Too Much Sun, Not Enough Wire we walked the generation and the grid, and in Store of Value we walked the battery that turns intermittent power into something dispatchable. This piece is about where all of that electricity gets spent first and most visibly, the car. Part 3 is the road.

We have written about Chinese electric vehicles before, in The New Paradigm last July, in Full Charge in March, and in a field report from the floor of the Beijing Auto Show in April, and the readers who followed those will know the arc. The industry crossed from subsidised hypergrowth into organic, self-funding demand. The wild experimentation phase wound down and the operational-excellence phase began. The weakest players were whistled off, and the survivors got stronger. What we want to do today is advance that story to where it actually sits in the middle of 2026, because two things have changed since March that matter more than the monthly sales noise. The growth at home has stopped, and the centre of the contest has moved underneath the car, into the silicon.

A quick word on the macro, since it connects to the last two notes. When we wrote Full Charge, Brent was above $112 and we argued that expensive oil was an accelerant for electrification. The Strait has since reopened and the oil price has handed back the war premium, which we covered in The Strait Falls Quiet. The tailwind faded. The point worth carrying forward is that it never mattered as much as the headlines implied, because the Chinese transition runs on the falling cost of making the hardware rather than on the price of the diesel it displaces. Cheaper oil does not slow this down. The reasons to keep electrifying did not change.

So we will walk the road the way we walked the wire and the cell. We start with where demand actually is, then the export valve that is keeping the industry whole, then the price war and the discipline being imposed on it, then the question of who survives, then the deepest and least-covered shift of all, which is the move into chips. At every stop we ask the three questions we always ask, what the business does, how profitable it is, and what the market charges for it, all read against the runway in front of it.

IMPORTANT NOTE: We are presently in the process of getting a license with a major regulator, and while that process is ongoing we are not able to publish the portfolio update and company notes. We’ll do a big reveal of the new plans as soon as we’re in a position to do thusly. We apologise for it taking time, but this is unfortunately a fact of life. With that we’re also putting the opinion part of this behind the wall.

NOTE: Panda+ is now closed to new joiners. We thank everyone for their interest and custom.

Nothing in this Substack is Investment Advice. This information is provided for informational purposes only and does not constitute financial, investment, or other advice. Any examples used are for illustrative purposes only and do not reflect actual recommendations. Please consult a licensed financial advisor or conduct your own research before making any investment decisions. The authors, publishers, and affiliates of this content do not guarantee the accuracy, completeness, or suitability of the information and are not responsible for any losses, damages, or actions taken based on this information. Past performance is not indicative of future results.

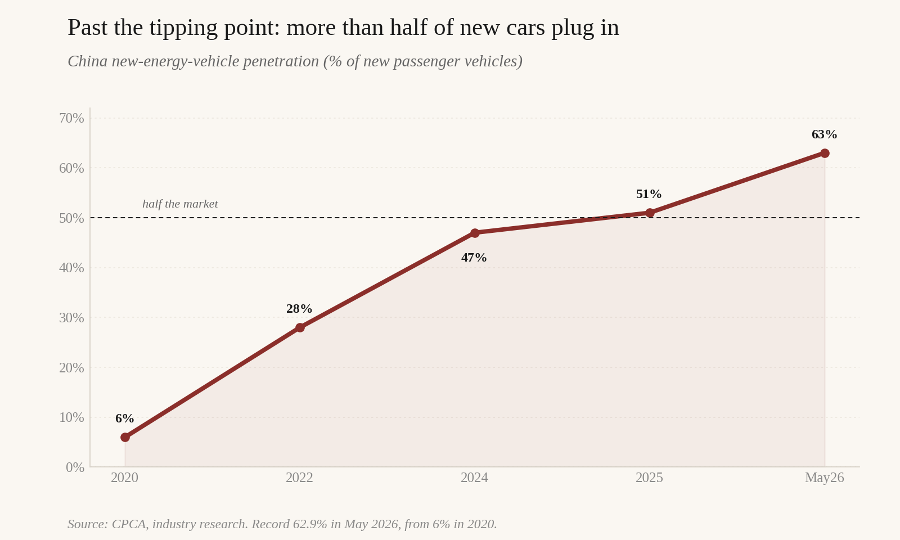

Past the tipping point

For a decade the China electric-vehicle story was a penetration story. The single number everyone watched was the share of new cars sold that plugged in, and it went vertical. From six percent in 2020 to twenty-eight percent in 2022 to fifty-one percent in 2025, and to a record sixty-three percent in May 2026. More than half of the new cars sold in the largest car market on earth are now electrified, and on the best months it is closer to two in three.

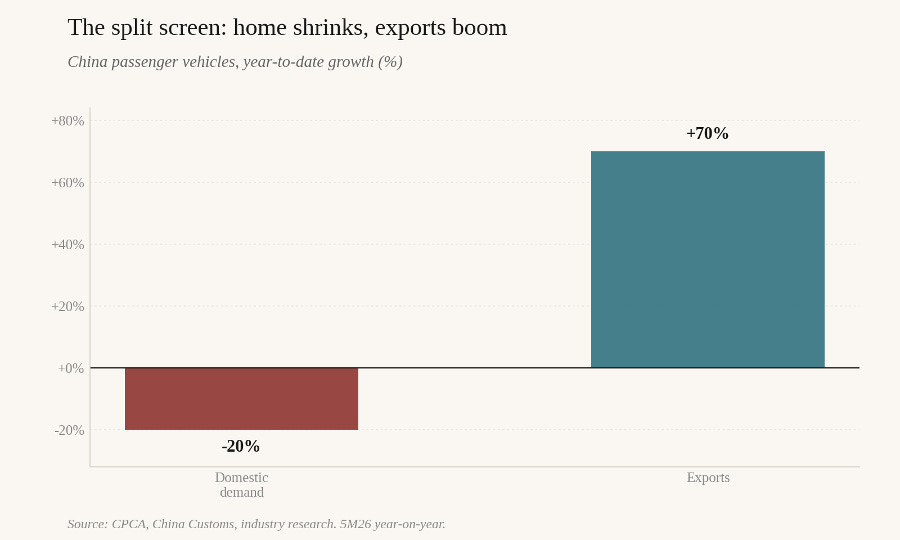

That is the achievement, and it is also the problem, because a penetration curve that has passed halfway cannot keep being the growth story. The home market has stopped growing. Total passenger-vehicle demand is running in the low twenty-millions, down roughly a fifth so far this year on last year’s pulled-forward base, though it remains comfortably the largest car market on earth. New-energy volume specifically, the part that matters for this piece, is running near thirteen million and is no longer growing, with the most recent monthly prints modestly lower year on year. Strip out the policy distortions we come to in a moment, and the underlying picture is an adoption curve that has flattened just as the cycle has turned down, which are two different things that are easy to confuse. Thirteen million new-energy cars a year is still enormous, close to the size of the entire United States car market across every powertrain, and it is now organic rather than subsidised. But it is no longer growing at twenty percent. The era of effortless volume is over.

The policy backdrop: discipline that bites slowly, stimulus that mostly moves demand around